|

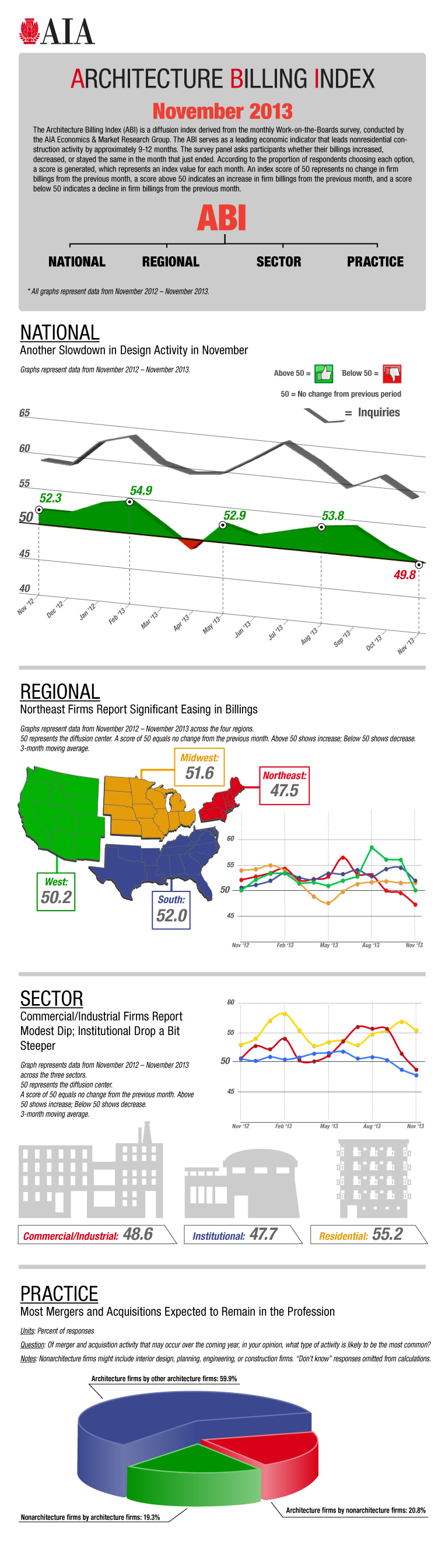

I'm about two weeks late with this (sorry, I was traveling…), but the American Institute of Architects (AIA) released the most recent Architectural Billings Index from November. It's down from last month and November's value of 49.8 is slightly below the Mendoza Line-like threshold of 50 (a value >50 indicates and increase in billings; a value <50 indicates a decrease in billings). The ABI is considered a leading indicator for construction activities. Decreasing architectural billings seems ominous, but like most things in life, the devil is in the details. Most of the pain is being felt in the Northeast. Everywhere else in the country is above 50 (the south has been clearly above 50 all year). Furthermore, in terms of product type, multifamily residential continues to show strength while commercial/industrial and institutional projects have dropped below the 50-point mark. The rundown is below:  The full AIA report can be read here. Anecdotally, this makes sense to me. Many of the 30+ tower cranes in San Francisco are hovering over high-rise residential tower projects, a market that has been strong for some time. It's important to note that the health of macro markets (the West) should not be confused with micro markets (San Francisco). While San Francisco is in beast mode in terms of building, Sacramento (90 mile miles to the east) continues to struggle. While multifamily is picking up slightly in Sacramento (16 Powerhouse, 25th and R), hospital work is the major source of activity in a market that's overall very slow. Like they say about real estate: location, location, location.

1 Comment

There's a lot of whispering going around about how DPR and Skanska landed the whale-sized new Apple headquarters campus. That's a huge win for them on a high profile project. However, flying under the radar is BN Builders, who landed contracts for an auditorium, fitness center, and R&D space on the new campus. Read about it here. Those projects, while not as newsworthy as the main building on campus, are going to be equally cool buildings (and likely more favored by Apple employees!).

I've known BN's VP of Preconstruction, Nick Pera, for years, dating back to when I was an adjunct professor at Santa Clara University. He's a class act and I wish him and BN the best of luck. Many of my recent posts have discussed the improving construction industry (click here and here). These improving trends are over macro-regions (west coast, southeast, etc.). There are many metropolitan areas that are going gangbusters (38 tower cranes over San Francisco!). But others are still hurting, despite promising trends for the industry overall. One such place is Sacramento. Consider these stats from the Associated General Contractors of America reported in this week's Sacramento Business Journal:

Despite this, graduates of Sacramento State's Construction Management Department are still highly sought after. Where are they going? Click here to find out. Spoiler alert: big cities other than Sacramento. Many of the students that graduate from the Sac State Construction Management Department want to stay in the Sacramento area. I don't blame them, I like this area. However, if current trends persist, then for those students that want to pursue a career in commercial building construction, their next stops will increasingly be dense urban areas. Companies are ditching the suburbs for city cores, which will require a lot more construction in those metropolitan areas (office, housing, retail, schools and other services).

This will require students to develop skills to work in environments that are difficult for construction. Cities present their own difficulties, and the dense they get, these constraints will continuously escalate.

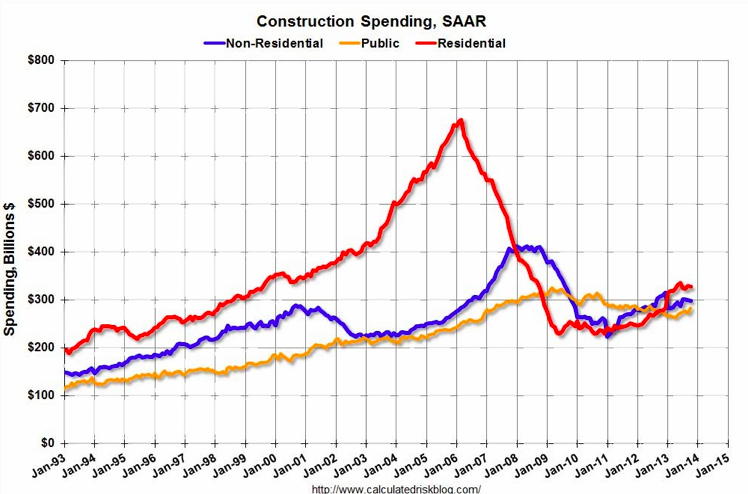

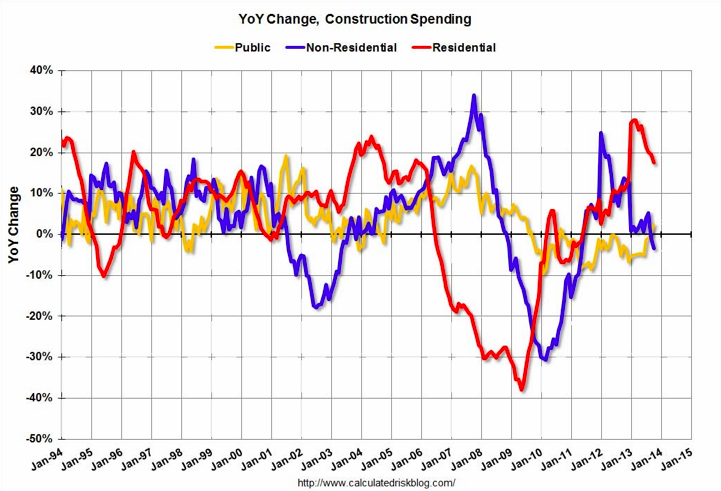

The entire is a very interesting read in terms of the shift underway from suburban corporate campuses to moving into high-rises. Read the entire article here. A couple of graphs from Bill McBride at the Calculated Risk blog:

A few highlights:

For the full article, click here. Also buried in yesterday's Wall Street Journal was an article about lumber prices (p. C3). After peaking at $378.30 per thousand board feet, the highest level since April 4, prices are slipping (now at $364.80). The decrease in price is due to seasonal changes (less domestic construction in winter) and new lumber mill capacity coming on line. The price run-ups were due to sales of U.S. lumber to foriegn countries (China bought 701 million board feet, or 35% of total U.S. output, last year). The additional capacity being added is a good sign because it shows confidence in America lumber producers that the market for lumber (and, by association, construction) is getting warmer, yet the increasing production will keep prices in check.

In a post two weeks ago about the most recent AIA ABI numbers, I wrote about multifamily projects are showing the most strength (the multifamily ABI is at 57; and ABI > 50 means an increase in architectural billings for that project type). Buried on page A8 of yesterday's Wall Street Journal is a graph that also shows how strong the multifamily market is. Basically, the graph shows the percentage of permits going to multifamily projects in select metropolitan areas in the U.S.:

New York City: 91.8% San Francisco: 90.6% Miami: 76.3% San Jose: 73.7% Los Angeles: 71.1% Middlesex County, MA (west of Boston): 70.3% Fort Lauderdale: 68.4% Boston: 65% San Diego: 64.9% Newark: 61.1% There are 38 tower cranes over San Francisco right now, so one can imagine the amount of units currently being constructed. The WSJ article states that in the case of Miami, the investment |

Archives

January 2024

Categories |

RSS Feed

RSS Feed