|

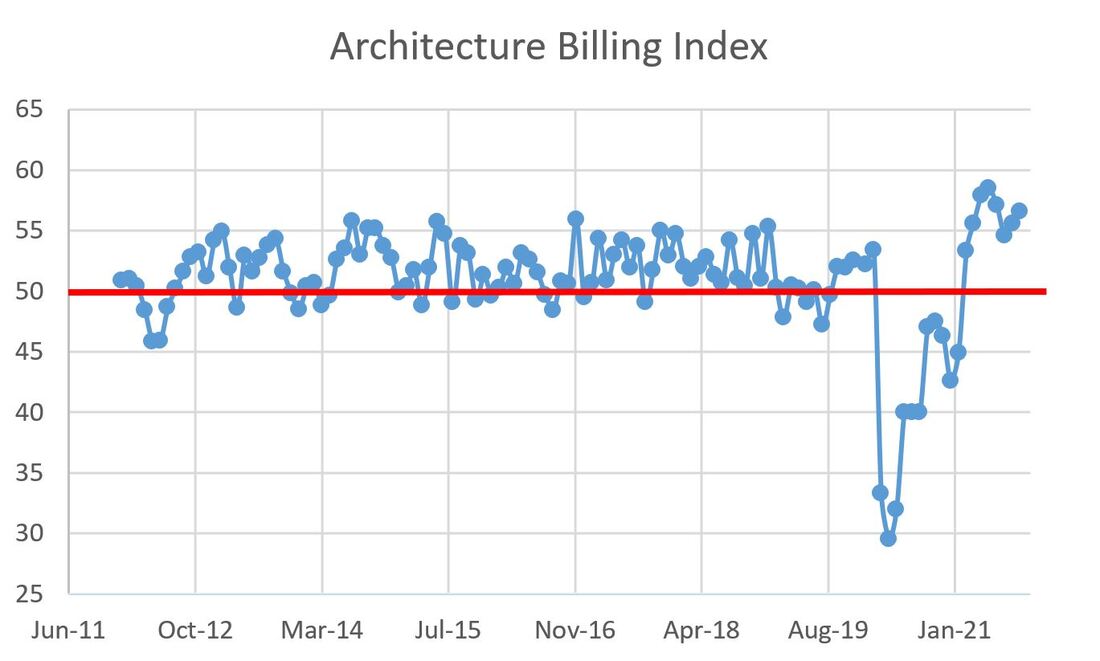

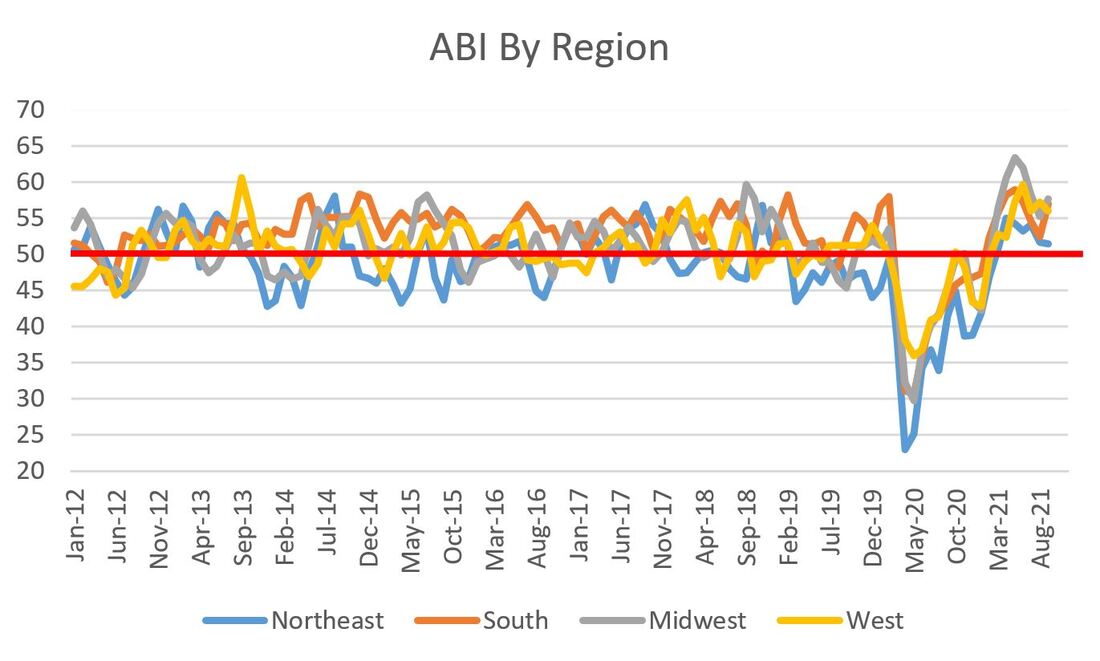

This post is a construction economics two-for-one. The short take is that architectural billings are still very robust and have increased for the second month in a row, while contractor backlogs have dropped over the same period of time. Let's dig into the good news first. The American Institute of Architects (AIA) released the September Architecture Billings Index (ABI) this past week and the value came in at 56.6, above August's 55.6 and July's 54.6. While the ABI is down since peaking at 58.5 in May, all of the data from 2021 are way above the average ABI, which is 50.8 since 2012. As a reminder, the ABI is a nine-to-12 month leading indicator of construction activity. A value greater than 50 means that architecture billings are increasing; conversely, any value less than 50 means billings are decreasing.  The regional ABI data is a mixed bag with two increases and two decreases:

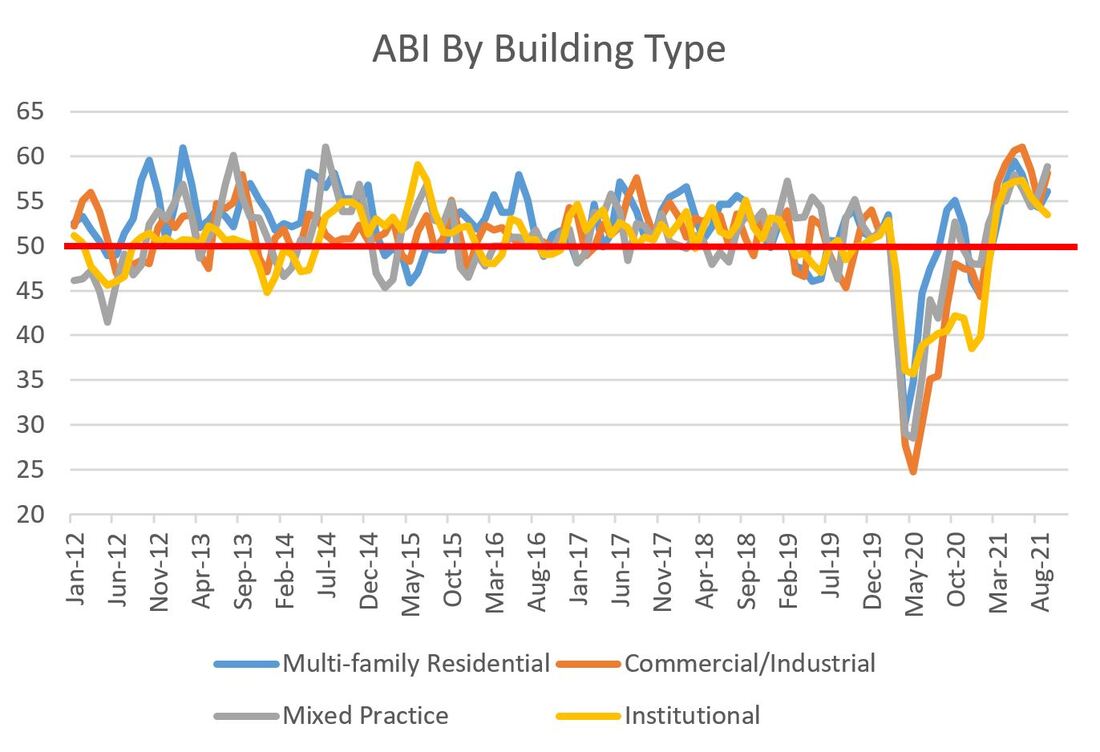

For industry sectors, gainers beat decliners three to one:

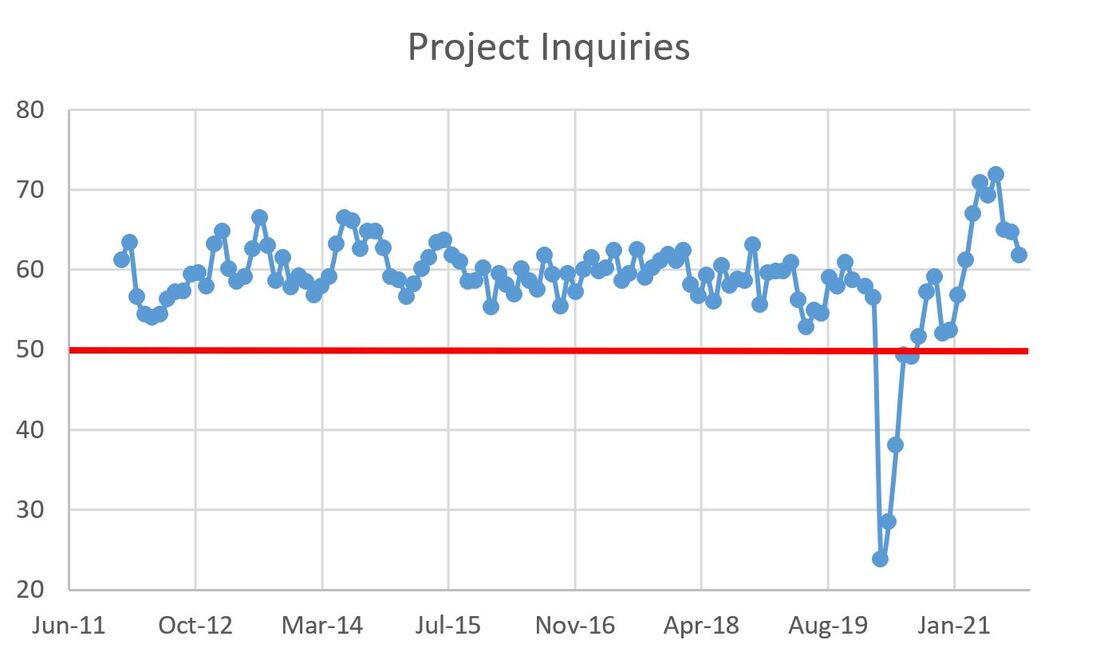

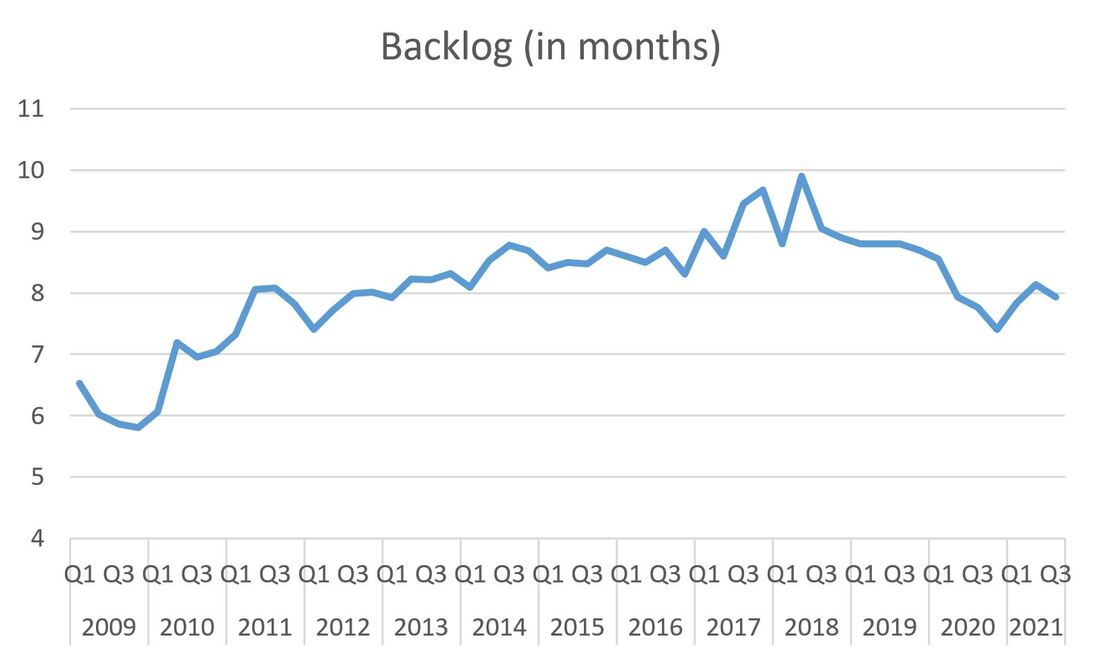

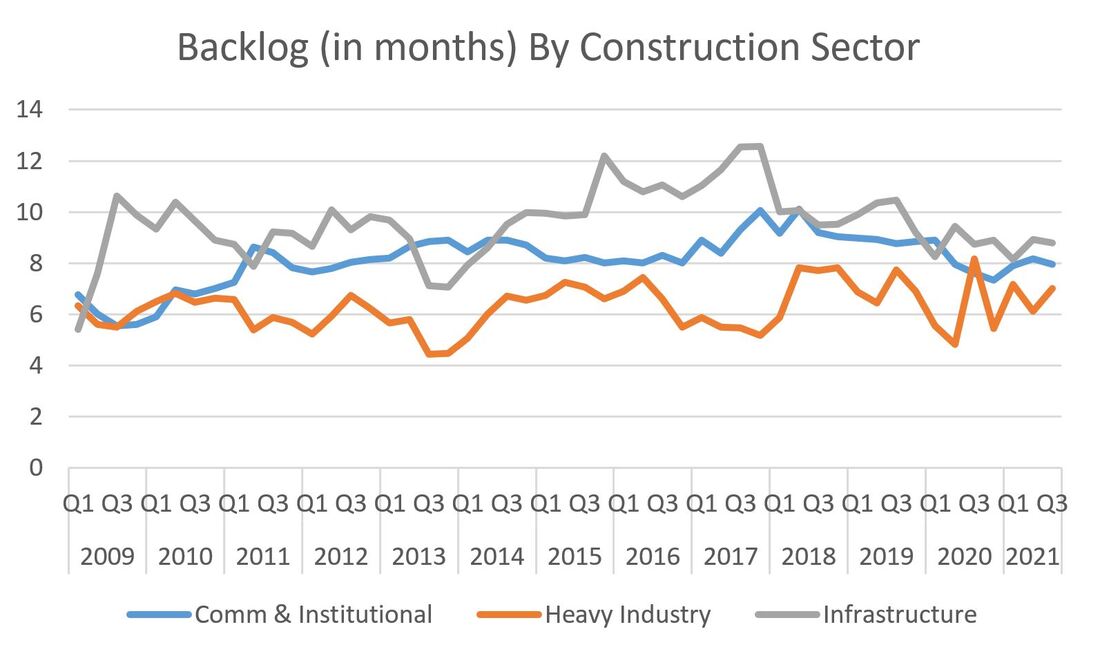

While the news is positive on the balance, one thing to keep an eye on are the four straight months of declines in project inquiries, with September clocking in at 61.8.  monLet's pivot to contractor backlogs, which are reported by Associated Builders and Contractors (ABC) as the Construction Backlog Indicator (CBI). Speaking very generally, when backlogs increase, it is a indicator that contractors are getting busy and, hence, the construction industry is healthier. As the spoiler alert title of this post indicates, the overall CBI has declined the past two month, coming in at 7.6 months for September, declining from 7.7 months in August and 8.5 months in July. Sounds a bit ominous, but keep in mind that the ABI also declined from May to June and June to July before rebounding. CBI may be going through the same gyrations. The figure below shows quarterly CBI data, which mutes the affects of monthly increases and declines, yet the recent downward trend is evident.  Just because the overall CBI is down doesn't mean there are not some rays of sunshine in the data. The industry sector breakdown for September :

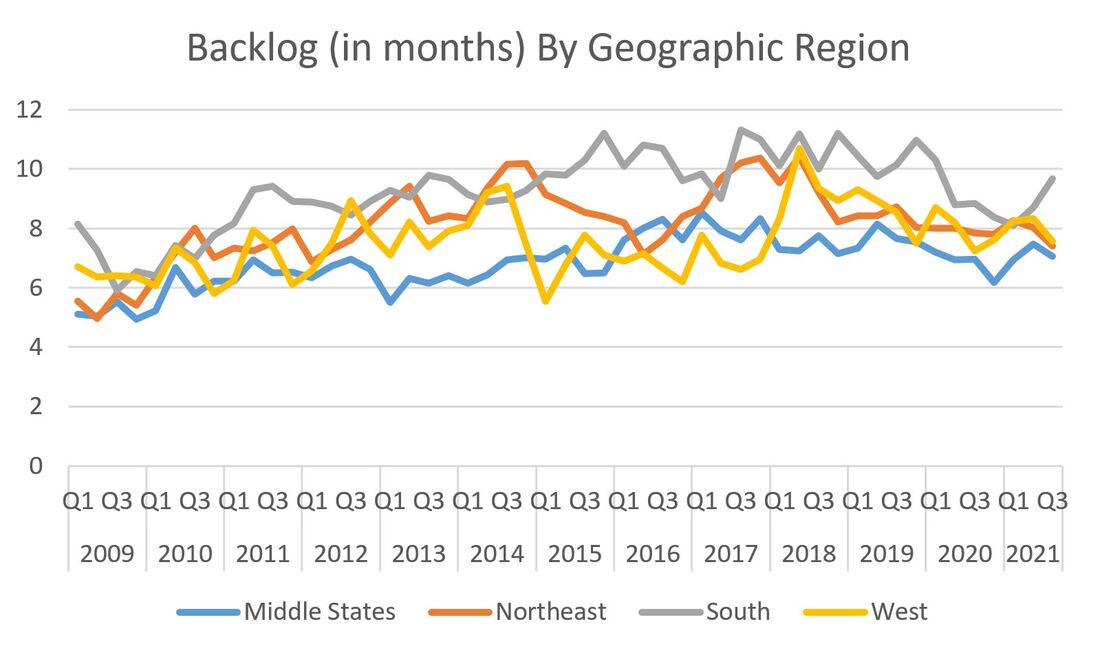

Moving on to geographic area, the results are more mixed:

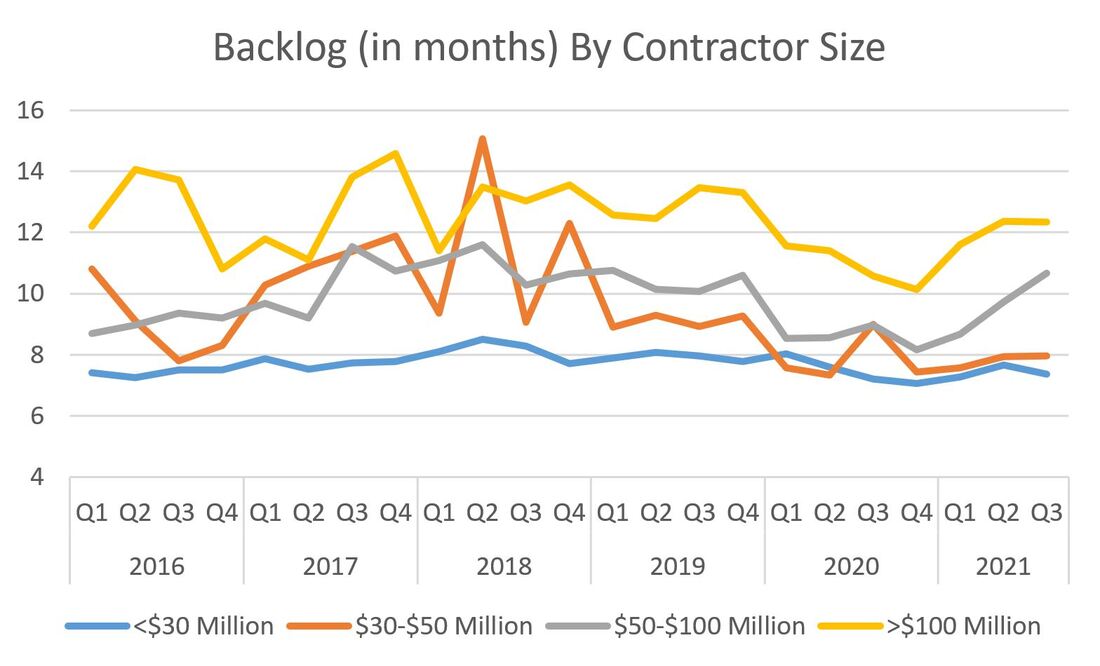

The last CBI breakdown data is by contractor size, which as three increases to one decrease:

The data presents a mixed bag with ABI up and CBI down and that permeates into the specific indices. This is likely to continue while the overall economy stays strong but commodity prices staying high and labor supplies remaining low. For every tailwind comes a headwind. 2021 continues to be interesting.

0 Comments

|

Archives

January 2024

Categories |

RSS Feed

RSS Feed