|

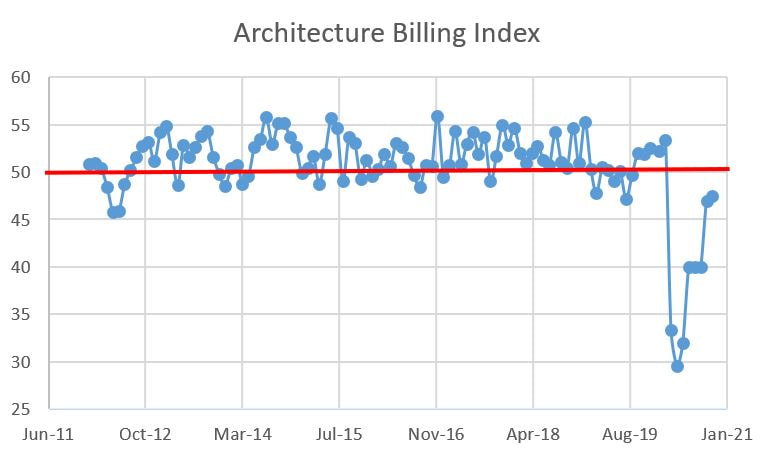

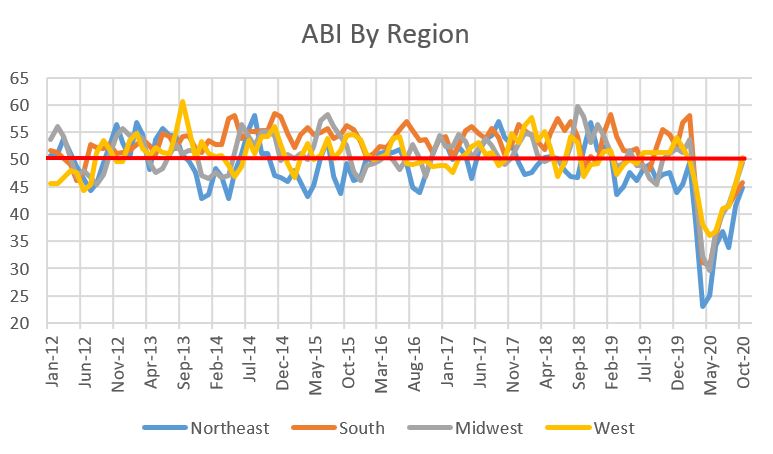

Let's get the bad news out of the way: the American Institute of Architect's Architectural Billings Index (ABI) clocked in at 47.5 for October. That is an increase over the previous month's reading of 47, yet a value less than 50 signifies that billings are decreasing (conversely, and this will be important if you continue reading, values greater than 50 mean billings are increasing). The ABI is a leading indicator of commercial building construction by approximately nine to 12 months, so it is an important leading economic indicator for the commercial building construction industry. Project inquiries increase their streak of being above 50 to three months with October registering a measuring in at 59.1. Inquiries represent interest in projects but not the actual start of design.  Now let's pivot towards some good(-ish) news: In terms of ABI measures with respect to geographic regions, all regions increased from the previous month and the West pierced the 50 level, being the first region to do so since February:

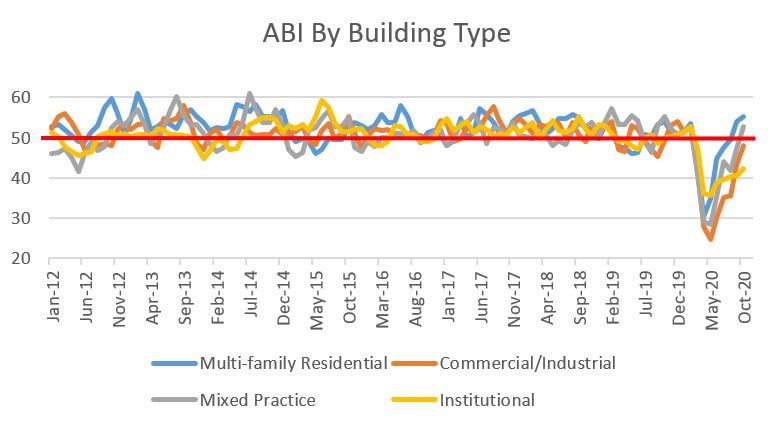

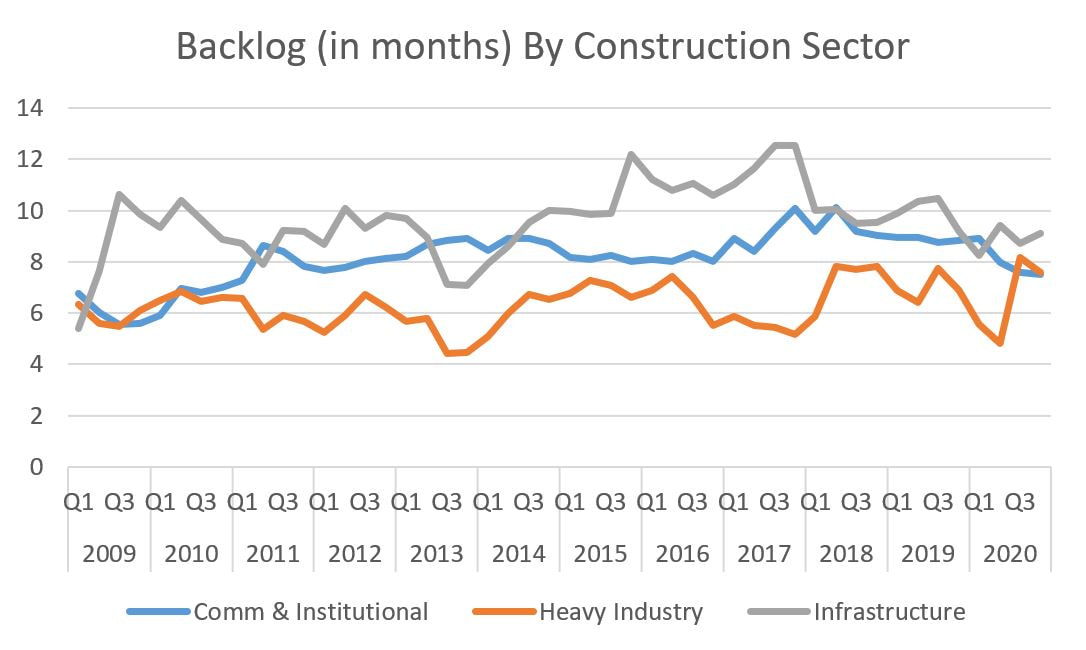

Now that I have your attention with some moderately good news, here's some even more moderately good news: all four industry sectors saw increases and TWO broke 50:

Given COVID, these gains are heartening and the industry is certainly moving in the right direction. That said, as I type this, we're staring at a giant third wave of COVID infections, the never ending post-election hangover and Congress heading for vacation without seriously considering a relief package. Hopefully this compendium of issues does not derail the planning and design of commercial buildings.

0 Comments

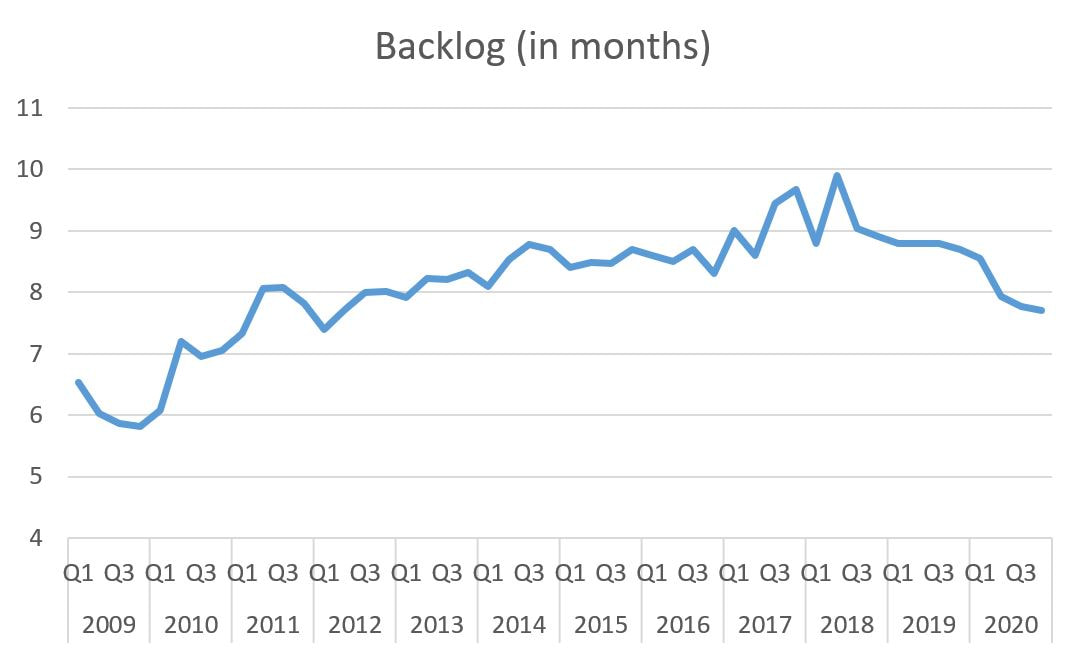

While COVID-19 is still dominating the headlines around the world, the construction industry still shows pent-up demand in the United States. This morning, the Associated Builders and Contractors (ABC) reported that its Construction Backlog Indicator for October increased 0.2 months from the previous month. While October 2020’s overall backlog of 7.7 months is 1.2 months lower than the October 2019 measure, it remains remarkably stable given the economic uncertainty surrounding the nation. The graphs below display quarterly data. October is the first month for the last quarter of the year, so Q4 is incomplete.  Let’s dig into the detailed backlogs, starting with the industry sector breakdown for October:

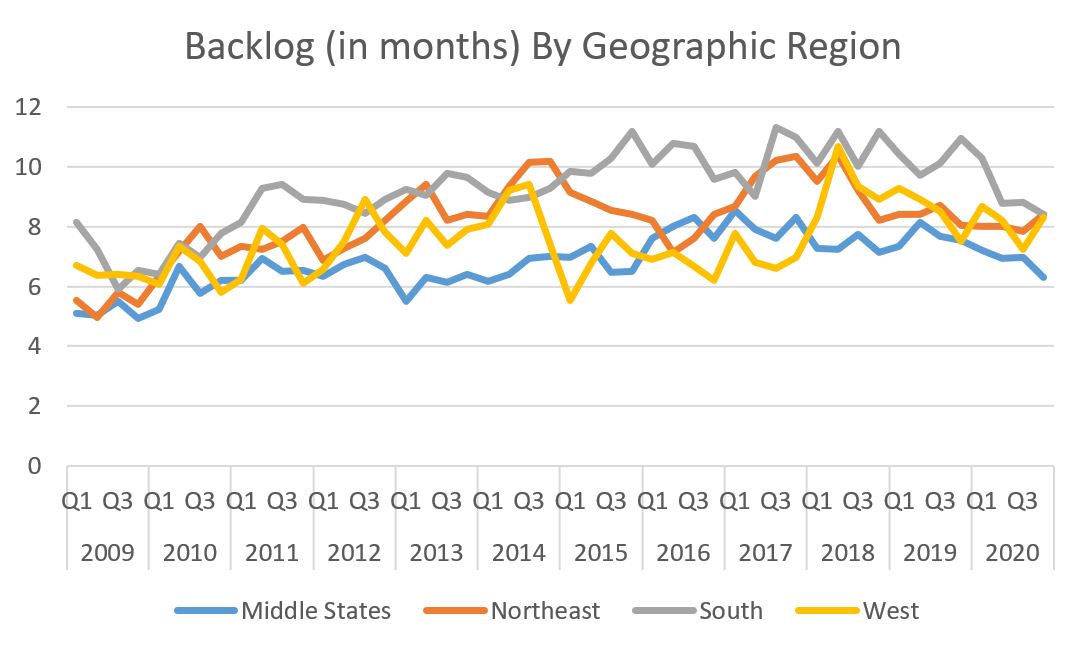

Turning to geographic area, there seems to be a bit of give-and-take with two regions up and one down sharply and one holding fairly steady:

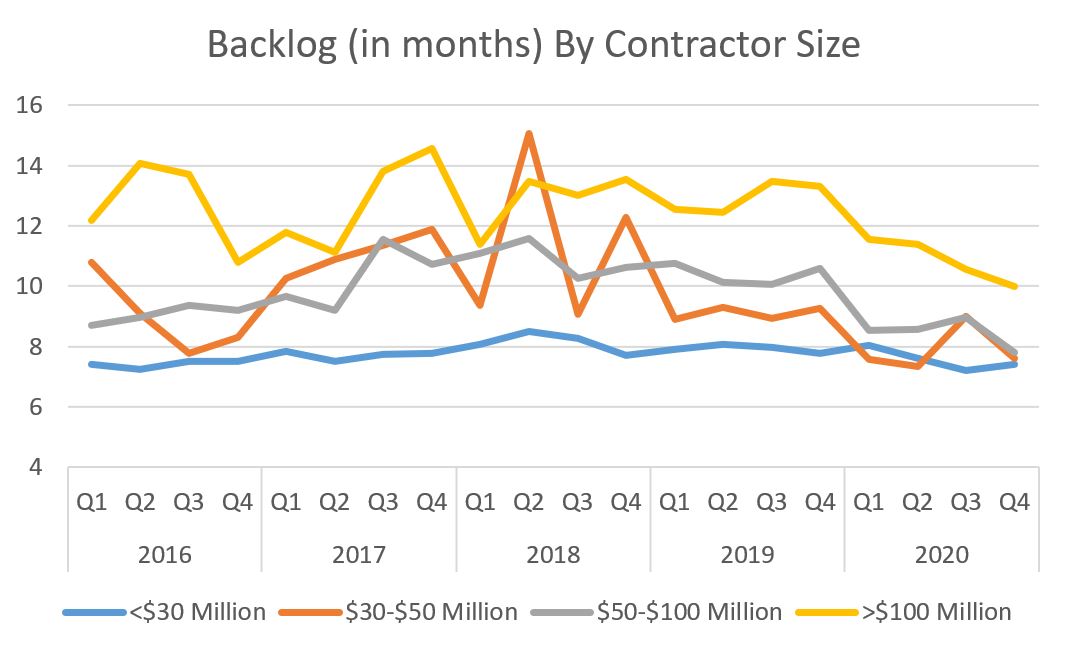

Last are backlog data by contractor size:

Also in the news today is Dodge Data & Analytics reporting that its 2021 Construction Outlook is pointing to $771 billion in construction starts, a 4% increase from last year. Dodge is expecting a drop in multi-family construction of 1%. This is more likely a sign of that superheated segment coming to the end of its cycle than the negative affects of COVID-19. The other sectors expected to see declines are predictable: retail and hotels. Institutional and public sector construction are predicted to be basically flat or see modest gains, which is also expected given that government aid is uncertain, a trend likely to continue with COVID-19 and the possibility of future gridlock between the Executive Branch and Congress. Manufacturing is also expected to be flat. Private construction is expected to increase with the usual suspects leading the way. Warehouses and data centers are expected to increase 5% as the FAANG companies (Facebook, Amazon, Apple, Netflix and Google) and their smaller peers continue to dominate while utilities are expected to increase a whopping 35% due to expected starts liquid natural gas exporting facilities and wind farms.

The WELL Expansion is going vertical. The first structural steel column was set last week while the footings are being placed on the Student Health Center side of the building. The team is working furiously to get out of the ground before the weather turns wet. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed