|

Wow, it's been a full nine months since I last wrote a post. Part of that is due to the fact that I've been super busy. When I'm super busy, that typically means the construction industry is super busy. It doesn't take a genius to recognize that the industry has been white hot in Northern California, particularly the Bay Area, for some time now. How long will the party last? How good is the construction industry in the rest of the country? Let's look at the data, particularly the American Institute of Architects Architecture Billings Index (ABI). Because it's been a while, here's some background: the ABI records architectural billings on commercial building projects. Any value greater than 50 means that architecture billings are increasing; conversely, any value less than 50 means billings are decreasing. The ABI is a leading indicator of commercial building construction by approximately nine to 12 months.

The composite October ABI figure was 53.1, down from 53.7 in September, but still clearly above the 50 threshold. Not too shabby. Similarly, the new project inquiry index clocked in at 58.5 in October, down from 61.0 in September, a slight downturn but still strongly above 50. Drilling down, we can look at how things are looking from a regional perspective based on the October 2015 data:

Everywhere seems to be humming along except the Northeast. I'm a little surprised because New York City is supposed to be booming right now. That is a good reminder that these regional values are just that: regional. Please don't apply them directly to cities within those regions. Sector Averages for October 2015:

0 Comments

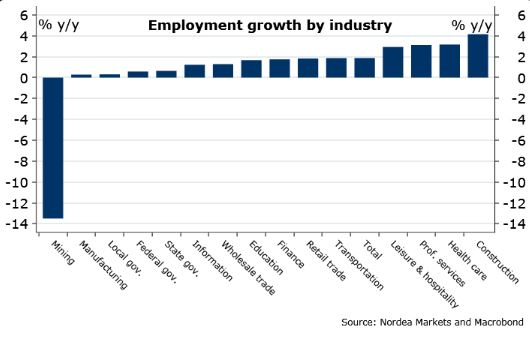

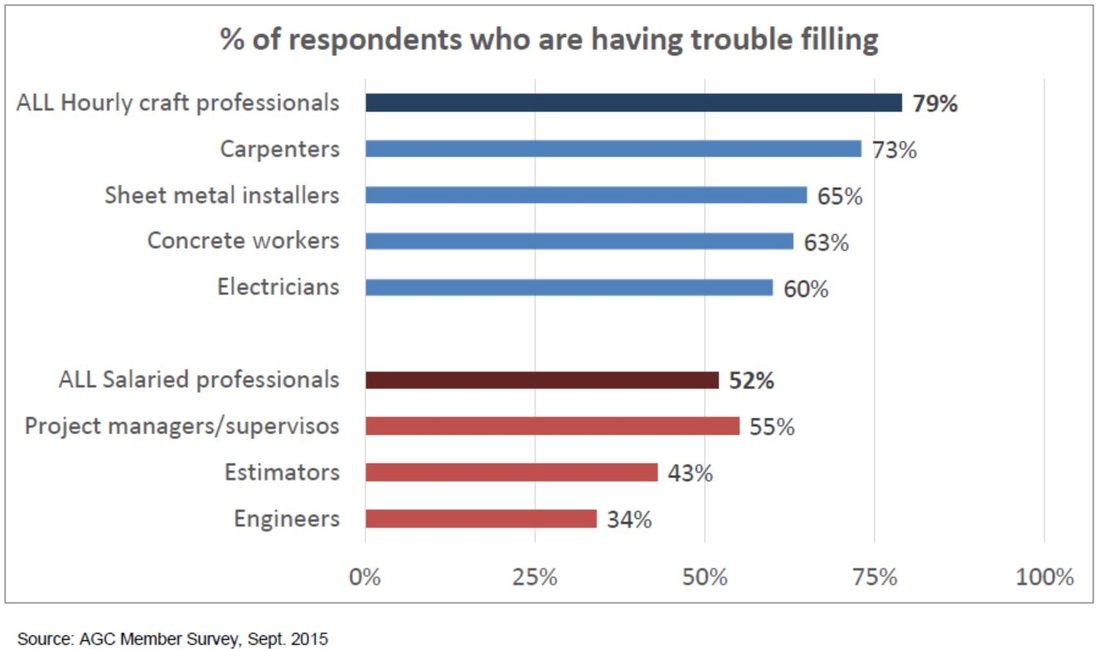

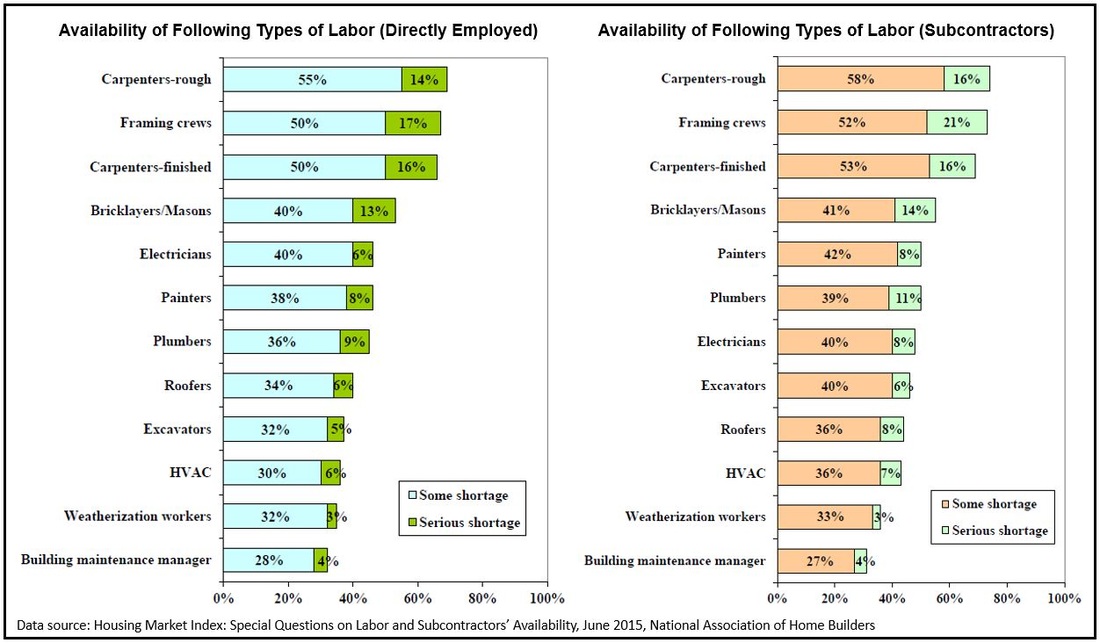

First World Problems: Too Many Open Positions, Not Enough Qualified People Willing to Fill Them1/18/2016 Every day, we are told about how poor the environment for job seekers is. Politicians from both ends of the political spectrum talk about it in differing terms (poor work force participation, jobs being outsourced overseas, lack of opportunities for college graduates, and so on). While I won't deny that the anxiety being felt by some people isn't warranted, I would like to point out that there is a huge opportunity for meaningful and well-payed employment in the construction industry. In fact, the currently white hot construction industry is in real danger of cooling off because there is a lack of people available to perform the necessary work. Consider first that the most robust employment growth is in the construction industry.  Now, consider that there is an industry-wide need for more people, most acutely in skilled trade positions. A survey of the members of the Associated General Contractors of America (AGC) reveals a deep shortage an skilled trade workers, particularly carpenters (for my students who like to call out my grammatical and spelling mistakes, the misspelling of "supervisors" was their mistake, not mine. But I digress...).  As a faculty member in a university Construction Management program, I am particularly interested in the salaried professional positions since that is our finished product (or at least we are preparing people to become salaried professionals). While the AGC tend to represent larger general and specialty contractors, the data is very similar to those in the home building industry.  After the 2008-2009 recession, people left the construction industry en masse. It is hard work and the volatility associated with busts and booms is too much for many to take. No one wants to work hard and be exposed to periods of under- or non-employment. But those issues now seem to plague every industry. I know I have, and will freely admit to, a bias towards the construction industry, but let me state the something very important: the construction industry is one of the few where there is high demand for people and embarking on an career in construction will likely not lead people down a path of chronic under/non employment. There is ample opportunity for both skilled blue collar and college-educated white collar workers. At Sac State, we have had 100% job placement for our graduates and I rarely hear complaints regarding crippling student debt. Construction jobs, at least for the foreseeable future, are not subject to mass offshoring.

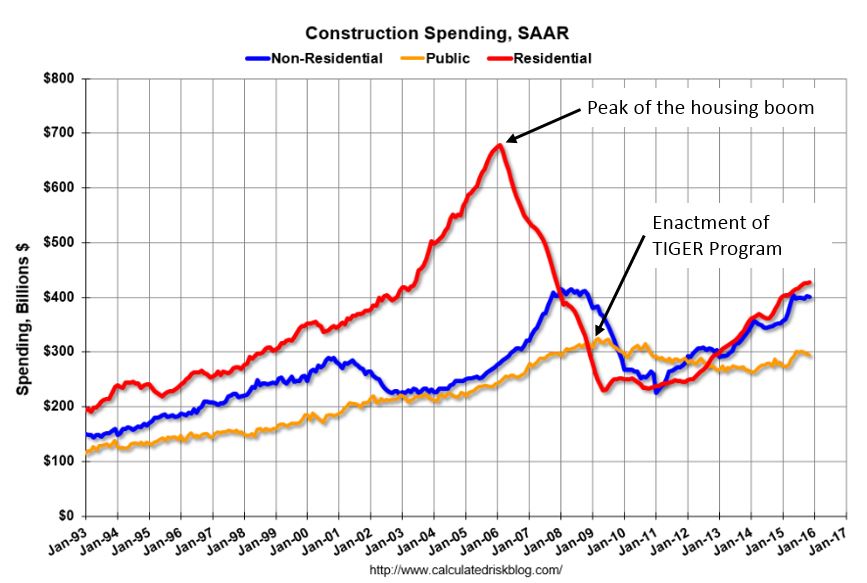

If you're considering a career in construction, then I offer you my biased congratulations. If you are unsure about what you want to do with your future, give strong consideration to an industry that will be key in building and rebuilding the infrastructure that makes the United States the largest and most stable economy in the world. The construction industry needs you. OK, so that is a bit alarmist, but based on recently released data from the Department of Commerce's U.S. Census Bureau, it is true. In November 2015, construction spending was estimated at a seasonally adjusted annual rate of $1,122.5 billion, which is 0.4 percent lower than the revised October estimate of $1,127.0 billion. Spending in the private and public sectors decreased. Private construction spending clocked in at seasonally adjusted annual rate of $828.2 billion (0.2 percent below October 2015's revised figure) and public construction came in at $294.3 billion (1 percent below October's revised number). The figure below, produced by Bill McBride at the Calculated Risk Blog, shows the trends in construction spending dating back to 1993. I added the references to the housing boom and TIGER Program (more on this later) for reference points.  Despite the decline in spending in November, every cloud is a silver lining, and there are a few this month. Let us start with the fact that this month's somewhat sad November 2015 construction spending number is 10.5 percent higher than that of November 2014. The construction market had a very healthy 2015. Secondly, the residential market is way off its bottom and is now almost double (if you allow for some generous rounding) from its lowest point. And it is not just housing: non-residential is way off its 2011 lows and is trending higher.

Public construction trended northward in 2015, although the trend was clipped towards the end of the year. It has steadily decreased since the enactment of the Transportation Investment Generating Economic Recovery (TIGER) funding program that was a part of the American Recovery and Reinvestment Act of 2009. Given those investments and the general consensus that our Nation's infrastructure is in dire need of some TLC, you would expect a stronger trend upward. Hopefully (at least for the sake of the construction industry), Congress will throw some much needed funds in the direction of infrastructure improvements. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed