|

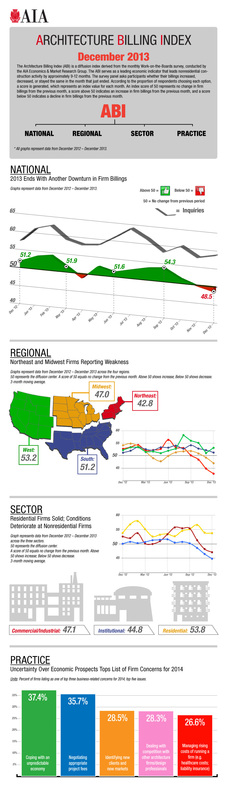

The title shows my west coast bias and how I don't want most (all?) of the people who read this to panic. Things are OK on the west coast (particularly in the Bay Area). The real headline from the American Institute of Architects (AIA) is that the Architectural Billing Index (ABI), a leading indicator for construction activity by nine to 12 months, is down for consecutive months for the first time since May to June 1012. It fell from 49.8 in November to 48.5 in December 2013. Any figure below 50 shows a contraction in architectural billings (and hence, less building construction down the road). The 48.5 figure for December represents the total U.S. building market as a whole. Breaking the number down by region and sector type tells a nuanced story: Regional averages:

Sector averages:

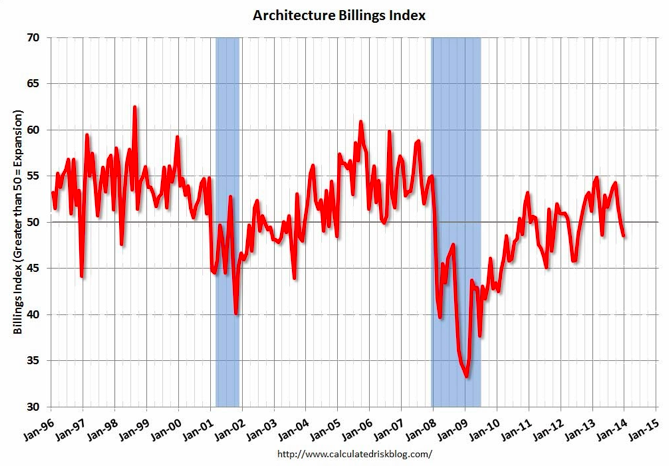

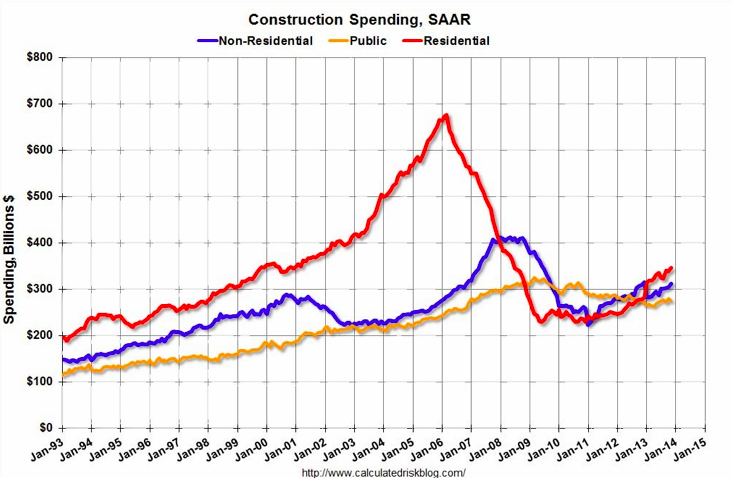

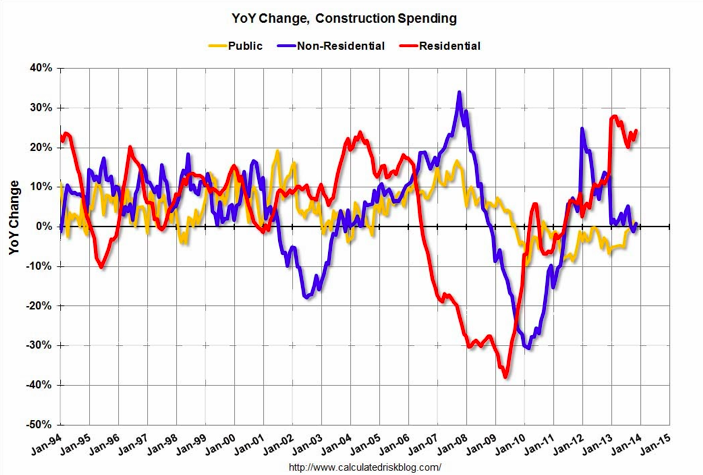

The ABI is essentially being dragged down by the Northeast (and to a lesser extent, the Midwest) and by the Institutional and Commercial/industrial sectors. The AIA's Chief Economist, Kermit Baker, states part of this overall decline in ABI this may be hangover affects from the Federal government shutdown last year. I buy that, particularly for Institutional projects (schools, college campuses, corrections facilities). But it doesn't explain why the West is showing continued strength. My hope is that things are just temporaily slow in the Northeast and Midwest due to the harsh winter and people working less. I guess we'll find out in the spring. Commercial construction continues to face headwinds in retail (malls are dying a slow death) and office (relatively high unemployment means less need for offices). One last thing: building construction is highly dependent on local markets. Some cities are up, others are down. Same goes for sectors. This adds to the volatility of the regional numbers, which snowball into volatility in the national number, as the figure below from Bill McBride at the Calculated Risk Blog so elegantly demonstrates:

The recent slide in ABI is not encouraging, but keep it in perspective. The design/construction is volatile, and it's more important to keep an eye on your respective market.

To read the full AIA press release, click here. Total single-family home sales were down 20% in Sacramento from December 2012 to 2013. Cash buyers for home accounted for 19.5% of all sales, down from 25% a year ago. The inventory of homes increased 44.2% year-over-year in December. Sounds like bad news, right? Supply is up and demand from cash buyers, seemingly the best kind, is down. But trow into the mix that conventional sales (those where your typical buyer takes out a conventional mortgage) were up in December 2013 over the previous December and you have signs of a healthy housing market. Cash buyers are typically investors looking to rent homes. Conventional buyers signal improving consumer sentiment, a precursor to a recovering economy. The increase in inventory leads to slower price increases (with more options of houses to buy, purchasers have some leverage over sellers, keeping prices down). All this equates to an improving market in Sacramento after years of distress.

This is also signaled in home builder sentiment. Nationwide, home builder sentiment declined from 57 to 56 from December 2013 to January 2014. Results greater than 50 indicate the degree that builders feel sales conditions are good. When homebuilders have relatively higher sentiment, they're more apt to build homes, signaling an improving economy. But let's dig deeper: In the west, sentiment increased four points to 63. Not too shabby. Why does this matter to someone interested in in the construction of large structures? Because single-family home building is a leading indicator for the construction of roads and other infrastructure, schools, retail space, and other buildings. Sacramento has been lagging the Bay Area for some time, but perhaps it's about to break out of its doldrums. For more reading, click these links: The winners:

The big loser:

Read ENR's summary of the bill here. As with the beginning of every new year, the prognosticators put on their thinking caps and give their forecasts for the coming year. Iv'e read a couple of good articles (links provided below), but I'll summarize them as to make your life easier. Keep in mind these forecasts are for the United State as a whole. They may not directly represent regions or specific cities (San Francisco, for example, is marching to its own beat). Here's my very basic summary of both articles: 2013: decent year, particularly since we’re still climbing out of the crater of the Great Recession, but most of the growth was in private residential. 2014: expected to be better, with the growth more evenly spread throughout construction sectors, except public infrastructure, which will continue to struggle due to a lack of investment. 2014 Construction Outlook (by EC&M Magazine) (The link above is behind a registration wall and is a long read) The nuts and bolts:

Simonson Says: For Now, 2014 Looks Fortunate for Many (published by AGC)

(Link above is a short read and requires no registration to read) The gist:

What happened in 2013:

What to expect in 2014 in terms of construction by market:

What to expect in 2014 in terms of material prices:

What to expect in 2014 in terms of labor:

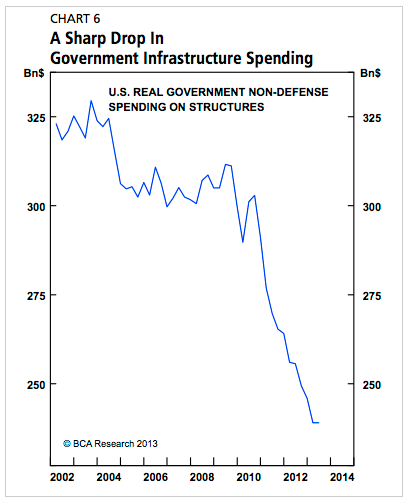

I recently wrote about how architectural billings, a leading indicator for construction, has slowed. It has in specific market regions and sectors, but multi-family housing is holding strong. The most recent data on overall construction shows similar trends. Residential construction spending is going strong. This is typically dominated by single-family housing, which is not the focus on my construction interest, but that is also considered a leading indicator for construction activities. Private non-residential construction spending lags the economy, so there's no surprise that it's been low. Bill McBride from the Calculated Risk blog thinks it will pick up in 2014 based on his analysis of the AIA's ABI. Public construction was down in November after inching up from its April low water mark. It is currently at 2006 levels (or 2001 in real terms). This is not surprising given that many elected officials are pushing austerity measures.

The above figures are courtesy of Bill McBride at the Calculated Risk blog. His full write-up can be read here.

|

Archives

January 2024

Categories |

RSS Feed

RSS Feed