|

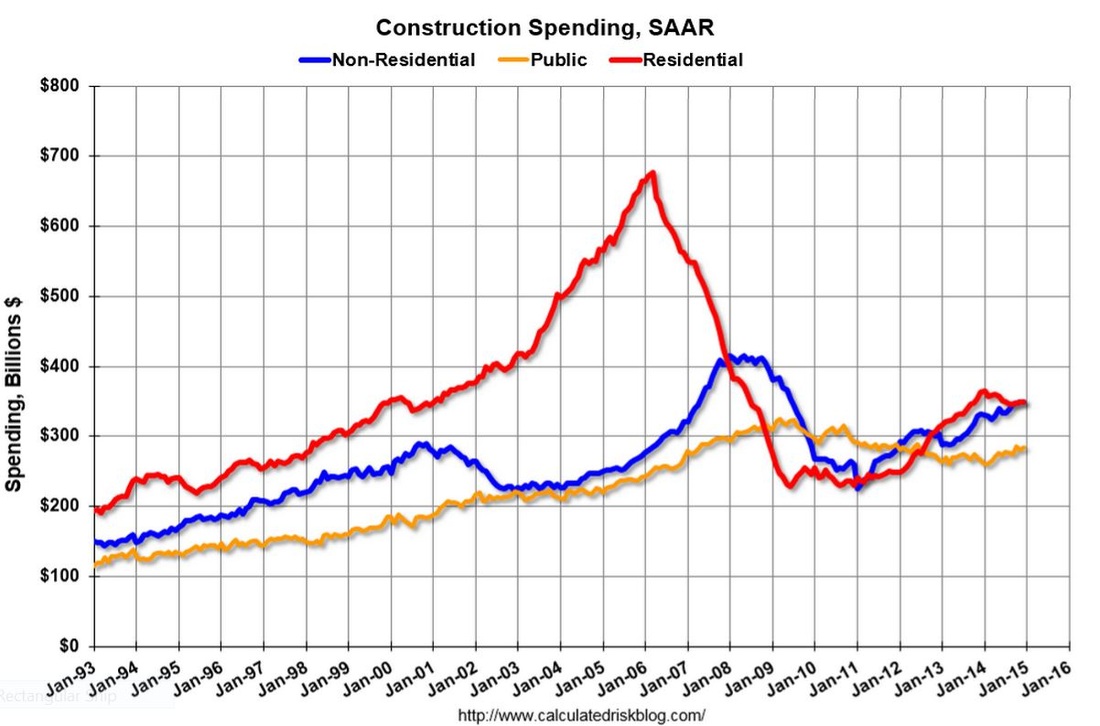

My previous post was about the relatively strong ABI figures from December 2014. ABI is considered a leading indicator. In this post, let's look at what actually happened. Drum roll...construction spending ended 2014 at its highest level since December of 2008. December 2014's seasonally-adjusted annual rate (SAAR) was $982.1 billion (up 0.4% over the November 2014 estimate). Private construction in December 2014 was reported at $698.6 billion (up 0.1% over the November estimate) and public construction came in at $283.5 billion (1.1% over November 2014 estimate). Both figures represent seasonally-adjusted annual rates. This is the first time public construction increased since 2009, which can be seen in the figure below that was created by Bill McBride at the Calculated Risk blog. This data is not too shabby. The construction market will likely not get back to 2008 levels (I tend to discount residential since we don't teach residential construction at Sac State) for some time, but the construction industry is getting healthier.

0 Comments

I've been lagging in 2015 (first post of the new year), but it's worth the wait. Economic data suggests the construction industry continues to get healthier. Let's start with the AIA Architectural Billing Index (ABI) for December 2014. The final figure for the year was 52.2, up from 53.7 in November. The ABI figures have cooled since summer, but December is still above 50. Any value greater than 50 means that architecture billings are increasing; conversely, any value less than 50 means billings are decreasing. The ABI is a leading indicator of commercial building construction by approximately nine to 12 months. Here is the geographic and sector breakdowns:

Regional (three month moving) Averages for December 2014:

The Northeast continues to be a drag. The above 50 scores for the nationwide ABI have been riding on the backs of the South and the West. That sentence is almost redundant from a month ago. Sector Averages for November 2014:

Project inquiries were down to 58.8 (down 62.7 in October and 64.8 in September). The Design Contracts Index (which, according to AIA highlights trends in new design contracts at architectural firms) was measured in at 54.9, down from 56.4 in October and 56.8 in September. The ABI is down overall and every sector, except for the steroid-injecting multi-family market, are down. However, every sector is above 50. The below-50 weakness is housed in the Northeast and Midwest. Hopefully the weakness remains contained there. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed