|

In the past two days, two leading economic indicators have showing continued improvement of the health of the construction industry (on top of the 48,000 new construction jobs reported earlier this month). First is the American Institute of Architects (AIA) Architectural Billings Index (ABI). The ABI has been steadily improving since the market bottomed out in early 2009. February's ABI came in at 54.9, increasing from 54.2 in January (50 is the baseline; greater than 50 means that architectural billings are increasing). The multi-family residential market was the healthiest and posted a strong gain over last month. The Northeast was the biggest winner in terms of geographical regions. All sectors and regions improved: Sectors:

Regions:

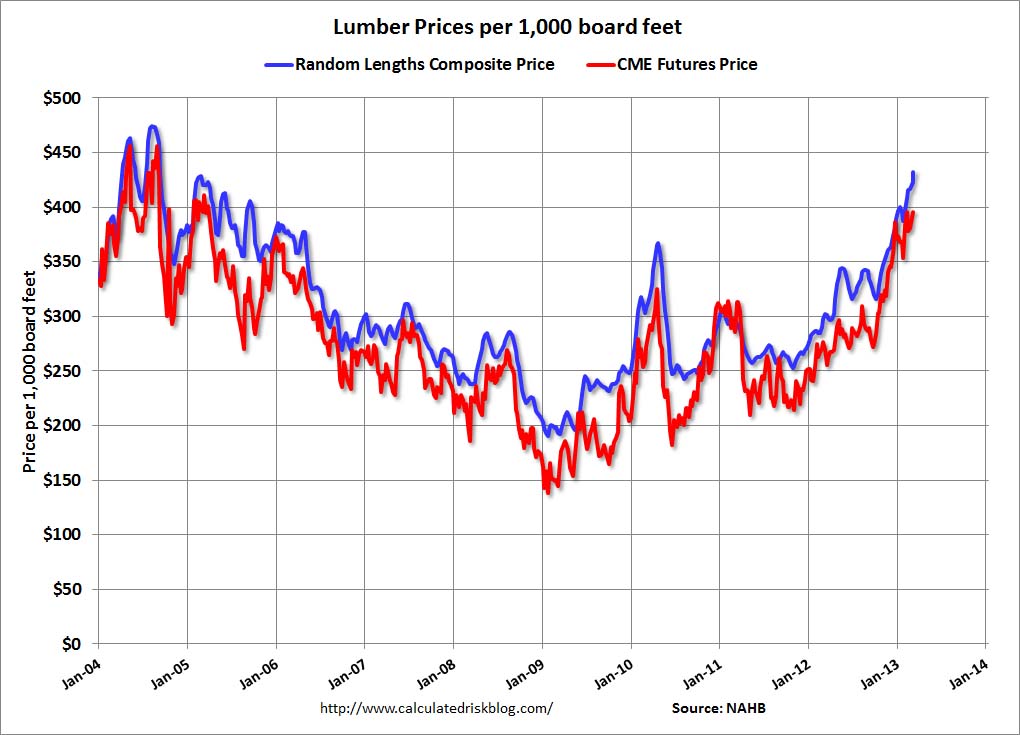

The New Project Inquiry Index (I'm not sure what that is, but it's name strongly suggests new projects) is at 64.8, it's highest level since January 2007. You can read the entire press release here and I'll post the cool graphic AIA typically produces when they post it. Second, it was reported today by the Wall Street Journal that plywood prices are skyrocketing (read article here). In the past year, prices have increased 45% and suppliers are having trouble keeping up with the increased demand. Increasing demand for plywood = more jobs using plywood = more construction activities. This is more good news for CM students. I have included the chart below that is maintained by Bill McBride at the Calculated Risk blog. Is shows the price of lumber per 1,000 board-feet, in case you're interested:

0 Comments

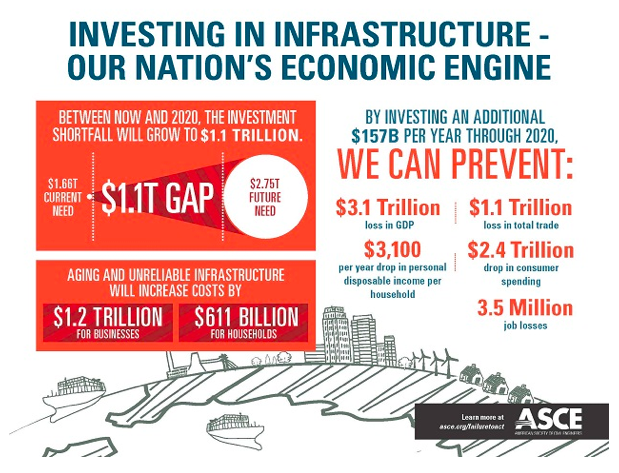

To answer the question posed in the title of this entry, we are apparently not investing in infrastructure, at least not in the ways we have in the past. Consider this graphic created by the American Society of Civil Engineers (ASCE):

Now, I typically take these graphics from ASCE with a grain of salt. I mean, ASCE, as an organization that supports civil engineers (a group that has a huge stake in infrastructure spending), is at least partially biased towards demanding more infrastructure spending. But the graphic below shows that they're not totally crying wolf:

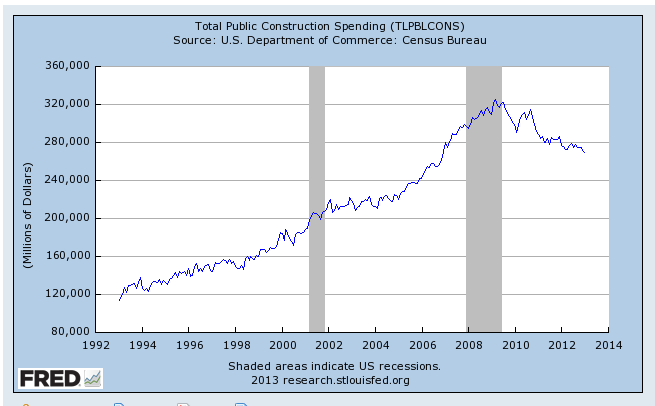

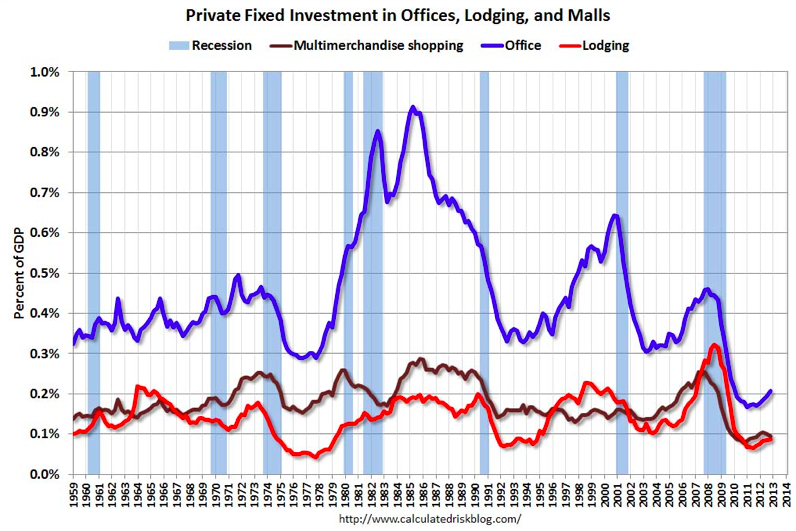

Since peaking in 2009, public spending in infrastructure has declined, save a short-lived uptick that started in late 2009 due to the American Recovery and Reinvestment Act. I'm interested in this phenomenon because at a recent technical job fair at Sac State, the large general contractors that are involved in infrastructure construction where among those with the most open positions. This form of hiring (soon-to-be recent college graduates) leads me to believe that perhaps construction spending in infrastructure is likely to start picking up (or contractors expect it to). I hope this is the case, because if ASCE is not calling for a falling sky, we could be in deepening trouble if we don't improve our crumbling infrastructure. If funding is dramatically cut, as is a likely scenario if the sequestration comes to fruition, it will only get worse. So public investments in infrastructure have decreased since the recession. There is very little private investment in infrastructure (in comparison to public investment). So where is private investment in buildings going? Let's go to some graphs created by Bill McBride of the Calculated Risk blog:

Capital investments in multimerchandise shopping centers (malls), office buildings, and lodging buildings have also declined since the recession. But there has been some positive growth in the past year or so in office and lodging building construction (malls have declined of recently after a slight recovery from 2011-2012; I have discussed the slowing growth in mall and big box retail construction elsewhere in this blog). The bigger story recently has been housing.

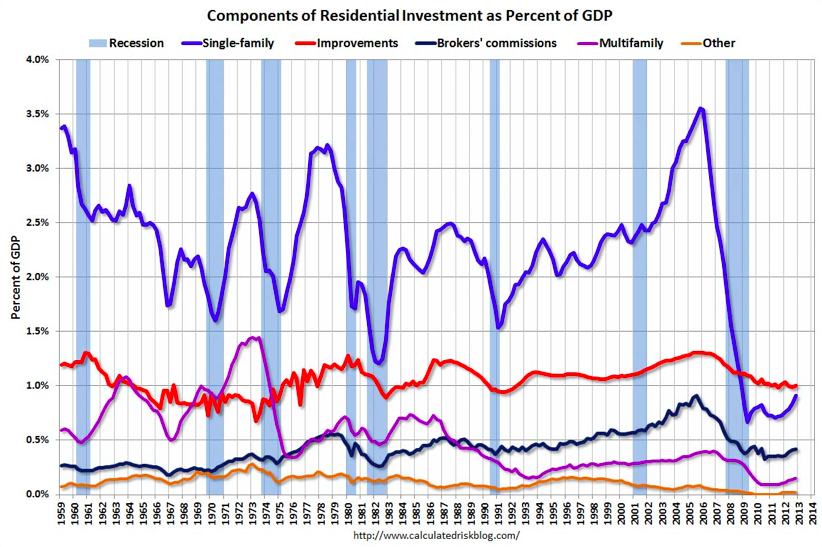

After also falling off a recessionary cliff, housing has increased markedly over the past year or so, particularly in single family housing (multi-family less so, but still moving positively in the last year). That's where the money seems to be going. With little inventory and large amounts of institutional money moving into single family housing, interest in that market should continue to be strong (emphasis on the *should*). A recent down tick in residential construction needs further data to see if it's an actual trend, but it seems on the macro scale that that's where construction investments are positive.

The bottom line: infrastructure spending is declining in the big picture (local areas may be bucking the trend, and hence the hiring of college graduates), but private building construction is increasing, particularly in housing. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed