|

The building has been opened up and the geopiers were quickly installed last weekend (I apologize for missing that...).

0 Comments

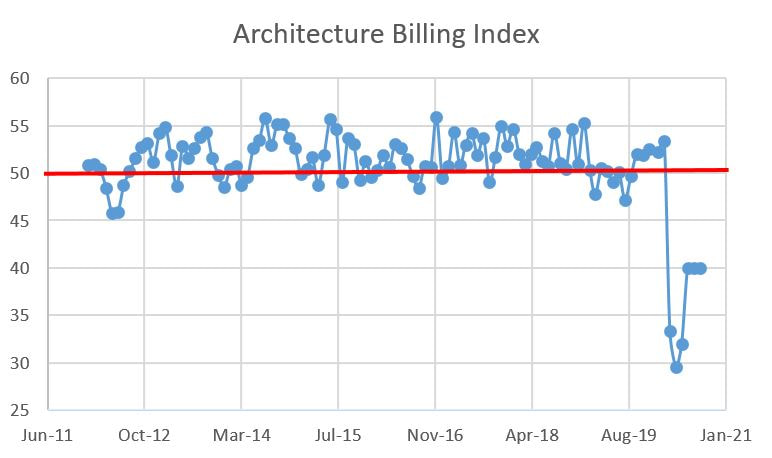

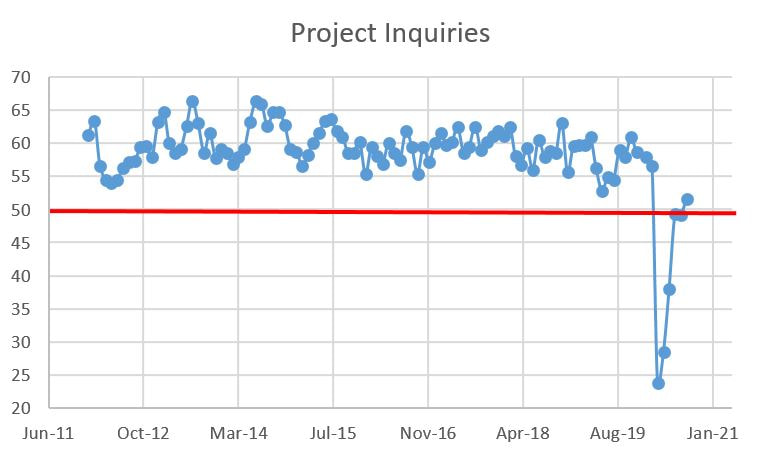

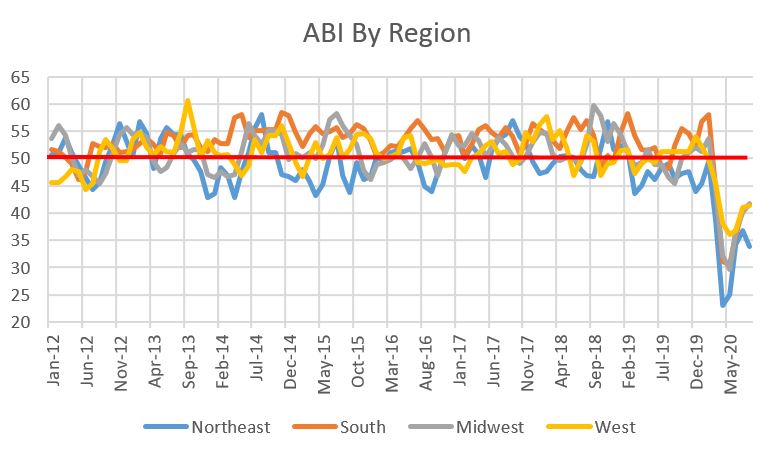

Construction Industry Update: Architecture Billings Flat While Contractor Backlogs Increase9/23/2020 We're three quarters into the month which means it's time to take a look at some economic indicators for the construction industry. Let's start with the leading indicator, the American Institute of Architect's Architectural Billings Index (ABI). As a refresher, the ABI is a leading indicator of commercial building construction by approximately nine to 12 months. A value greater than 50 means that architecture billings are increasing; any value less than 50 means billings are decreasing. For the third month in a row, the ABI checks in at 40. Still decreasing but at least it's holding steady and up from the low of 29.5 in April.  Project inquiries climbed over the 50 hurdle, but recall that inquiries basically represent people interested in projects, not those starting them. Still, we'll take good news however it comes.  The regional data shows modest increases with the exception of the northeast which turned south after four months of increases. The northeast has consistently lagged its peers. The breakdown for each region is as follows:

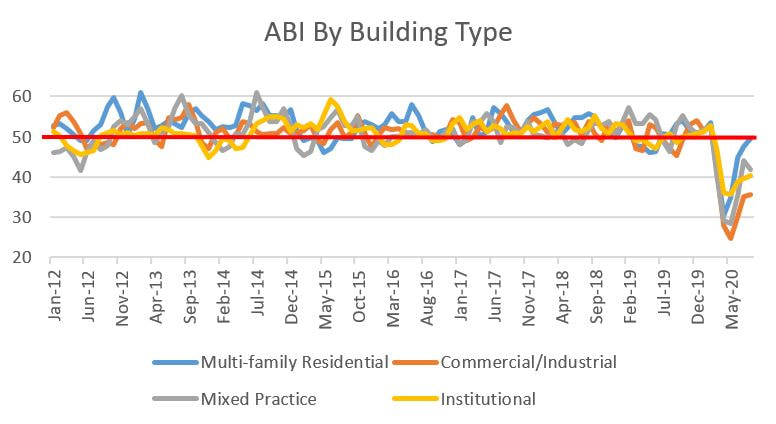

By building type, multi-family continues to be the best performing sector, albeit while still having declining billings. Mixed-practice was the only decliner. The August stats for all are:

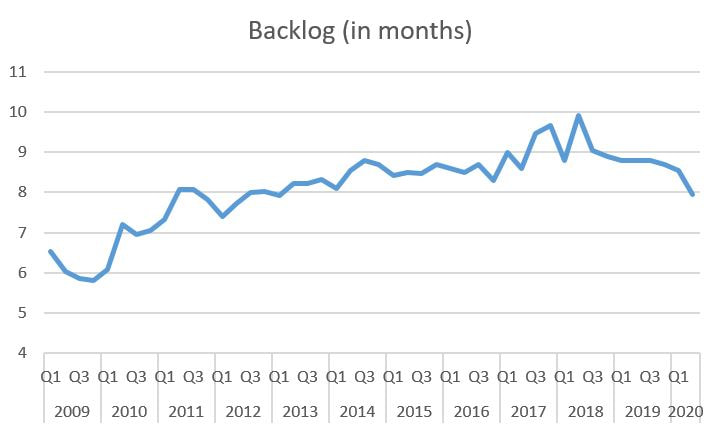

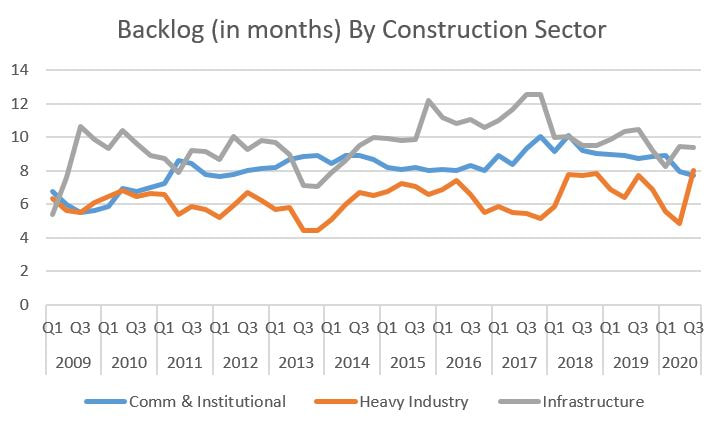

Switching gears from designers to contractors, a bright spot, albeit small, is that contractor backlogs, as reported by the Associated Builders and Contractors, increased last month. The data below is quarterly so the trends still look negative, but we also have one month remaining in Q3 so we may see these curves invert in the right direction next month. Contractors now have an overall backlog of eight months in August, up from 7.8 months in July.  The details are a bit choppy. Let's start with the details by industry sector for August:

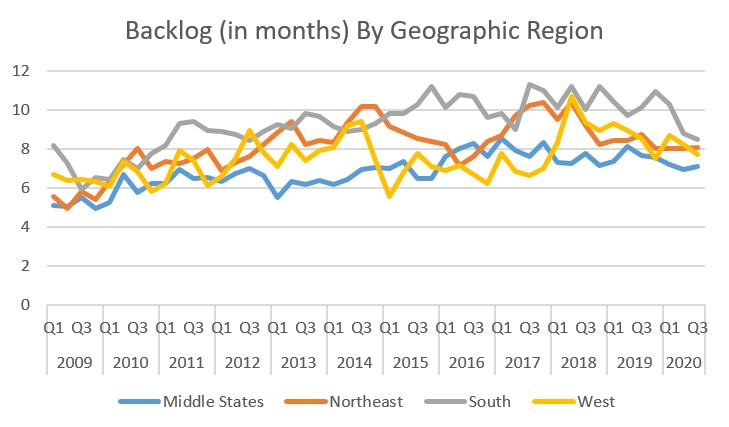

For geographic region, the data is also choppy with bright spots even though the quarterly curves below trend downward. The details are as such:

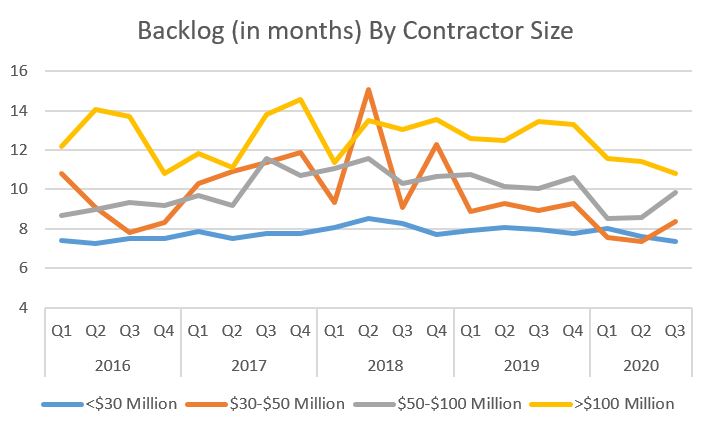

Lastly, the backlog by contractor size is below. The month-to-month data includes some relatively large extremes:

It's not bold to predict that there could be some more turbulence ahead with election posturing, a possible resurgence of COVID-19 as students return to work and the western states on fire, but in these anxious days, the ABI not decreasing and contractor backlogs increasing, even slightly, isn't too shabby.

|

Archives

January 2024

Categories |

RSS Feed

RSS Feed