|

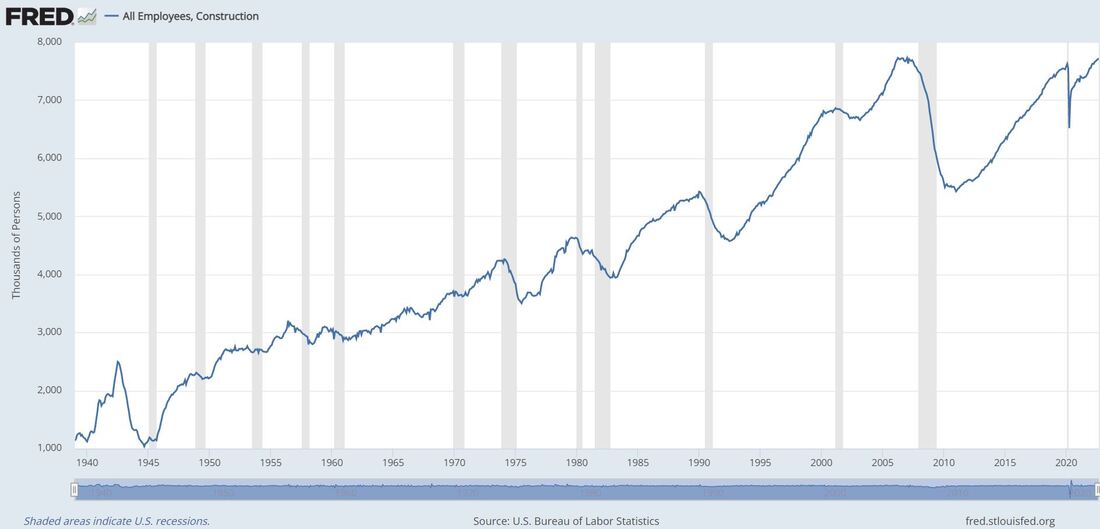

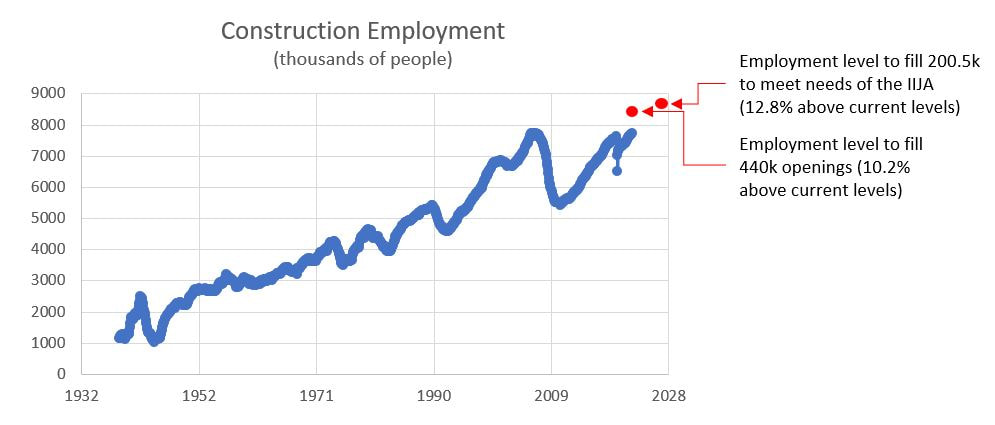

I read an interesting article in the McKinsey Quarterly this weekend regarding construction employment. Almost everyone in the Architecture-Engineering-Construction (AEC) industry knows there is a labor shortage, acutely for skilled trade positions. What I found particularly interesting is that the demands for such labor will increase markedly over the next few years as projects funded by H.R.3684 - Infrastructure Investment and Jobs Act (IIJA) commence. As of September 2022, there were approximately 7.7 million people working in the construction industry.  This amount is just slightly less than the peak construction employment achieved in April 2006 (7.719 versus 7.726 million to be more precise). However, the gains in employment since the market cratered in the housing bust that catalyzed the great recession of 2007-2008 are not enough. There are currently over 440,000 openings in the construction industry.  If those open positions are to be filled, we need to increase construction employment by over 10%. But that’s not all. The McKinsey article estimates that we will need over 200,500 additional positions between 2027 and 2028 to accommodate the projects that will be funded by the IIJA. Most of these jobs will be in areas that most people associate with traditional infrastructure, such as:

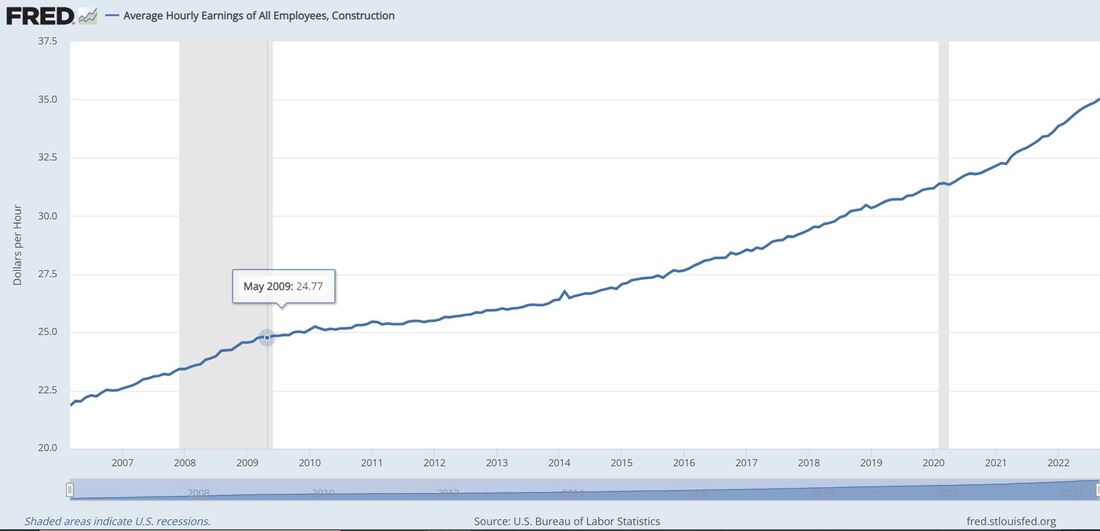

Yet, the biggest increase in employment will be necessary to build broadband infrastructure (9,100 engineering positions and 35,000 trades workers). These totals do not include people in the industries tied to delivering construction materials, which is in even greater need. The McKinsey article offers some recommendations for increasing construction employment (upskilling/reskilling existing workers, hire from nontraditional segments e.g. military, enticing people into the workforce with subsidized housing and other benefits e.g. childcare, and of course apprenticeships. Another key point to entice people into the construction industry is the pay. Strong demand for people for the foreseeable future and steadily increasing compensation are great selling points. However the case is made, it needs to be made strongly, because the construction industry is understaffed just as we are finally making serious investments in our built environment.

0 Comments

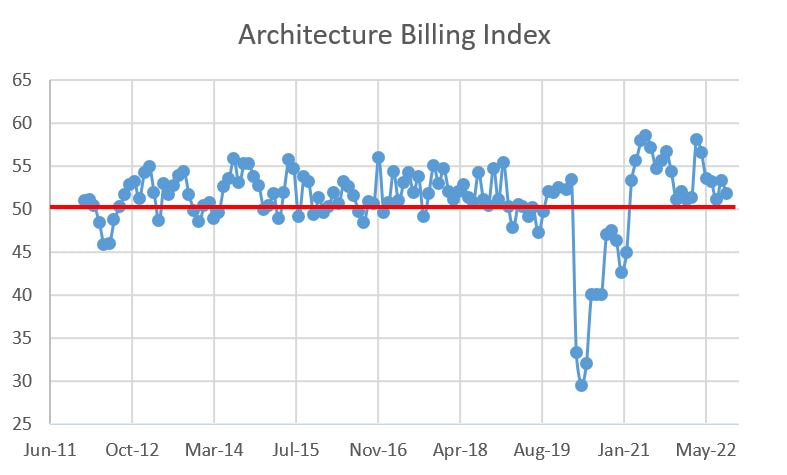

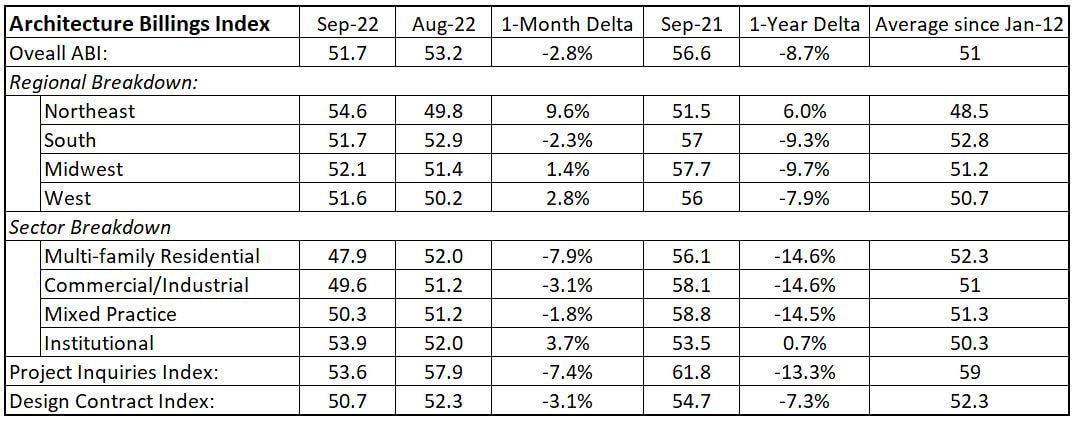

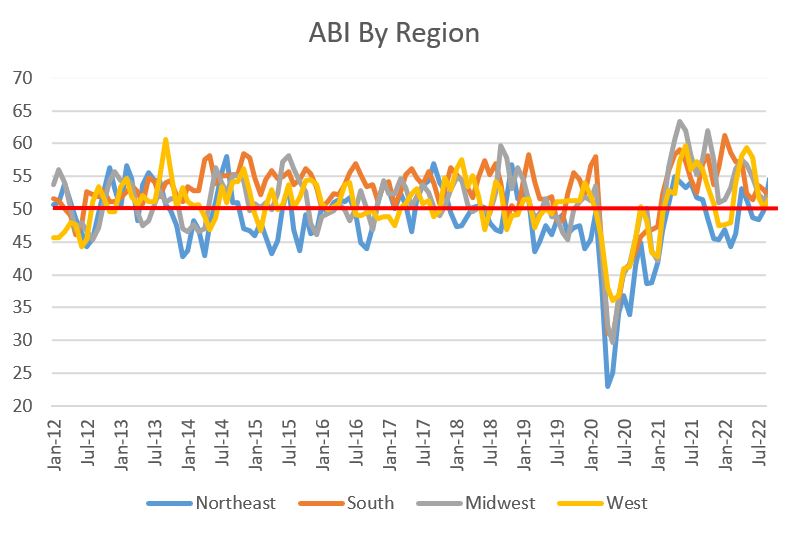

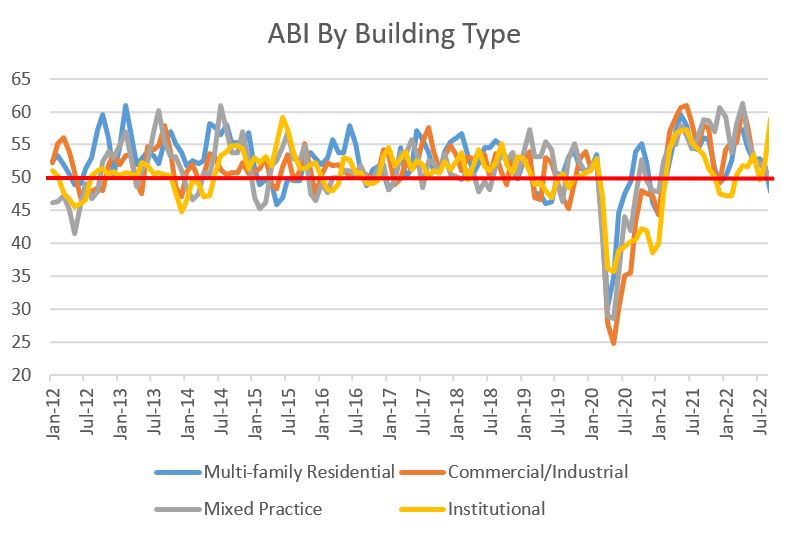

The American Institute of Architects' (AIA) Architectural Billings Index (ABI) measure for September slipped to 51.7, down from 53.3 the month prior. While this is a relatively steep drop, the losses were localized to two key areas that will be discussed below. And while the ABI slipped, it is still above 50 and is actually higher that it was in July. ABI measures above 50 mean billings are increasing, while those below 50 signal a decrease. The ABI is a nine-to-twelve-month leading indicator of commercial building construction activity. The amount of up-and-down activity in ABI is not surprising giving the gyrations in the overall economy.  When digging into the details, what jumps out to me are the September result for the South and Multi-family residential, the two sectors that have been in their own secular bull market for quite some time.

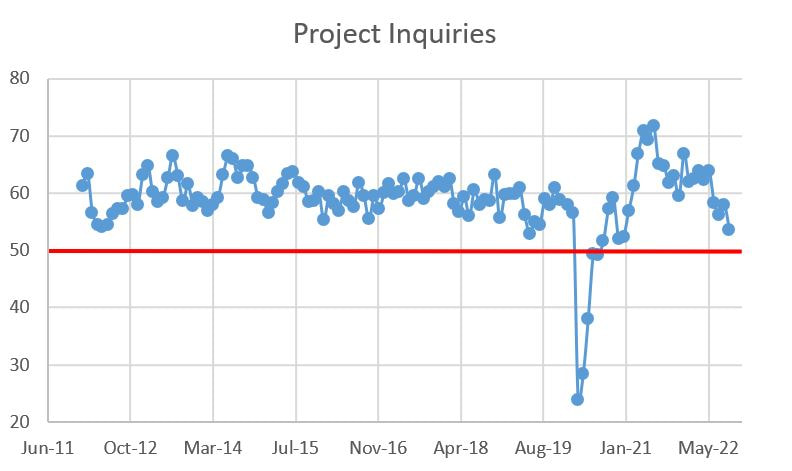

The graphical data is below, yet the big story of today is the steep slide in the South and Multi-family. That said, while ABI is a leading indicator, the more leading of the leading indicators are the Project Inquiry and Design Contract indices, and both are down on a month-over-month and year-over-year basis. Even worse, they are well below their 10+ year averages. The next few month could see even greater paring unless there is a bump from the infrastructure bills.     |

Archives

January 2024

Categories |

RSS Feed

RSS Feed