|

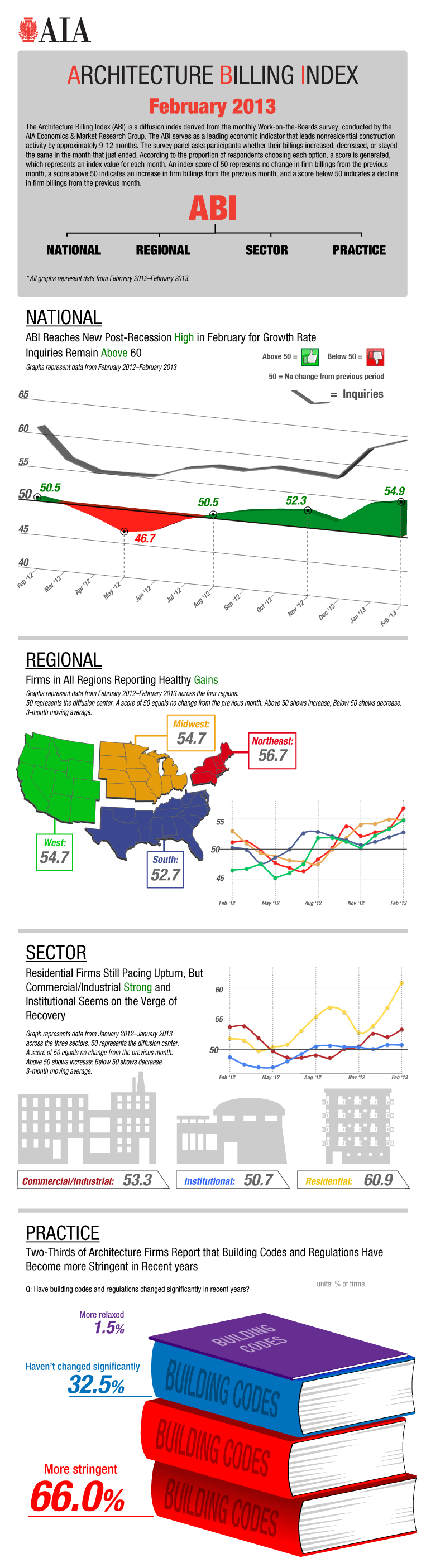

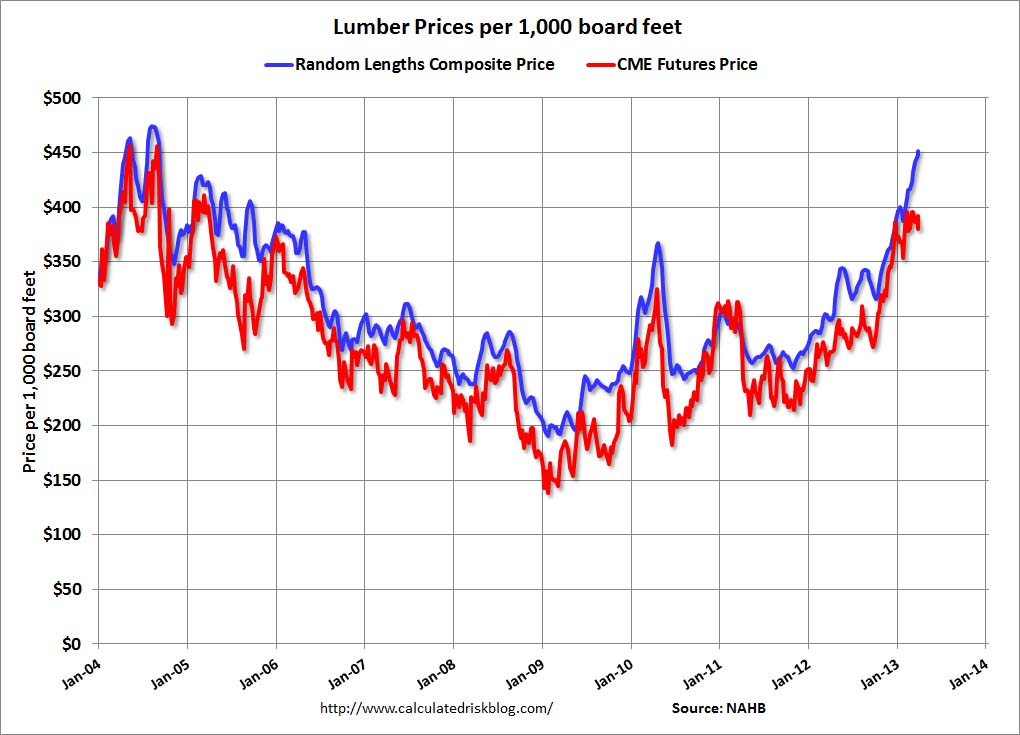

I've been a huge cheerleader for the recent growth in the construction industry. Part of this is because, as a college professor teaching in the Construction Management Department at California State University, Sacramento, I want the industry to do well because it means jobs for our students. And the job market, by all indicators, is improving. Anecdotally, students graduating from our department are getting job offers (with many good students getting multiple offers) and the salaries are bananas. Internships for continuing students are plentiful. There is data that shows that employment is gaining throughout the entire construction industry, primarily driven by the housing sector (I've written about the growth of the housing sector before, but here's a report published by the National Association of Home Builders with data). While single-family home builder data is nice, it's not really the market we prepare our students for. Most of our students work for large commercial general contractors, heavy-civil contractors (for infrastructure projects), or specialty subcontractors (electrical, mechanical, plumbing, etc.). Those markets also appear to be doing well, possibly riding the coattails of the housing boom (when you build houses, you also need to build ancillary projects like roads, schools, apartments, retail centers, etc.). As I promised a few weeks ago to post, the figure below shows the AIA Architectural Billing Indices for differing sectors of the construction industry and for differing regions of the country:  The ABI is above 50 for each region (above 50 means billings are increasing). Additionally, the ABI is above 50 for each construction sector, and it's above 60 for the residential sector (by residential, AIA means multifamily structures, such as apartments and condominiums). So, this is all good, right? Cracks in the Armor? I don't want to cry "the sky is falling!" However, there are some issues that we need to be cognizant of. First, home builder sentiment is falling. On April 15th, the NAHB reported that the Housing Market Index (HMI) fell from 44 in March to 42. Home builder confidence also slipped. This is not a huge deal as both HMI and confidence had been on a tear previous to the April figures release. And this is just one month "slide." Also reported on April 15, though, was a report stating that it is increasingly difficult to secure Acquisition Development and Construction (AD&C) loans for home building. Again, this is not directly related to the types of commercial and infrastructure projects that CM students are typically involved with, but they are a leading indicator of the projects they are involved with. If capital is difficult to get for home building projects, it will put a crimp in that sector of the economy that may very well spill over into other sectors of the construction sector. Just to show how manic the housing market is, the very next day, April 16th, it was reported that housing starts far exceeded expectations (7% increase). But that number is heavily weighed by multifamily construction (up 31%, which is good for CM students), but down 4.8% in single family housing (again, as a leading indicator, this is not so good). Also, the number of housing permits fell 3.9%. For an article summarizing all of this data, check out this summary created by the Business Insider. Things are a lot better than they were in the construction sector's dark days of the Great Recession, but some of the gains are slipping. So housing starts go up and down, as does home builder sentiment. Home builder stocks are on a tear (possibly getting bubbly), but they also correct from time-to-time. Those are indicators, but there is a lot of noise with them, particularly when applying them to larger commercial construction projects. The data that really has me thinking (and a little concerned) is the price of commodities tied to construction, particularly lumber. Check out this graph provided by the always on-the-front-edge-of-data Bill McBride at the Calculated Risk blog:

By itself, climbing lumber prices aren't necessarily scary. But combine them with a hiring frenzy (ok, maybe not a frenzy, but a big uptick nonetheless) that will likely lead to an increase in the cost of labor, and capital markets that are still a bit locked up in terms of lending for construction projects, and that's kind of a crappy cocktail. Increasing labor and commodity prices typically signal an improving economy, but if developers cannot get money to pay for them, then what's the point? Plus, the economy is still too fragile for large price increases to be absorbed by buyers not overly willing to pay a premium.

One last thing, and it's subtle. Caterpillar Inc. reported less than stellar earnings today. CAT is considered a bellwether stock for the overall economy, but the construction industry in particular. A big portion of the blame for their most recent decline in profits was due to problems in the mining industry (CAT supplies a lot of machinery to mining companies). But buried in this Wall Street Journal article is a sentence that caught my attention: "First quarter sales of construction equipment dropped 17% to $4.2 billion" It doesn't say where the decline in construction sales occurred (if it were limited to overseas, it may not affect the U.S. Or maybe it would.), but still, that's not particularly good news even without specifics. The bottom line: no need to panic yet (or at all), but keep your ears to the street and be cautious about the near-term health of the construction sector.

1 Comment

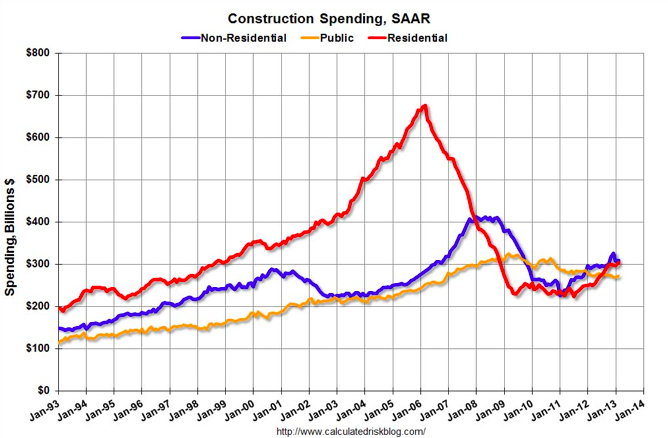

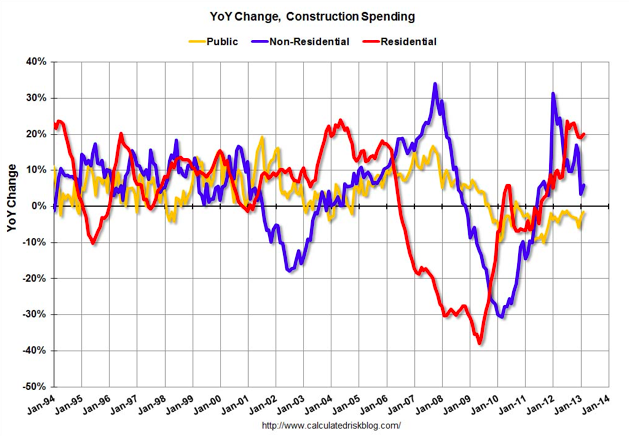

There was more good news regarding the construction industry last week. According to the U.S. Census Bureau announced last week that construction spending for the month of February grew 1.2% from the previous month and 7.9 percent above February 2012. See the press release here. The improvement of construction spending month-over-month and year-over-year can be seen below (as provided by Bill McBride at www.calculatedriskblog.com):

A lot of the growth is due to the residential sector, but non-residential construction is up 6% year-over-year. This news is good for larger general contractors (like the ones I deal with and that my students go to work for). However, public construction spending (for things such as roads, schools, etc.) is down 1.5% year-over-year. So, it's a bit of a mixed bag, but overall, it's good news. And the housing sector tends to be a leading indicator for larger commercial and civil structure construction, so there may be better news on the horizon.

In other news... There was an article on the proposed new Apple campus in Cupertino, CA in Bloomberg Businessweek on April 4. According to the article, the 4-story, 2.8 million square-foot headquarters building's proposed cost has ballooned to ~$5 billion dollars (~$1,800/SF). There is an effort underway to value engineer $1 billion from the cost. Some people are piling on and questioning the wisdom of 1) constructing a building that is a giant donut (this type of space arrangement can actually isolate employees, which is is counter to the Silicon Valley ethos of creating spaces that increase the probability of chance meetings and collaboration, and 2) building an elaborate (ostentatious?) self-celebratory structure. I'm not going to weigh in on this because my attitude is that if you don't like how Apple spends it's money, you're free to sell your stock. Apple is sitting on a 12-figure cash stockpile, and they have to spend it somehow (with real estate having certain beneficial tax advantages). If you don't own stock in Apple (and presumably don't live in the shadow of the proposed structure), why do you care? But what I will mention is that there will almost certainly be a halo effect in that multiple additional peripheral structures will be constructed (hotels, banks, law firms, accounting firms, etc.). Also, as a net zero energy building pushing the edges of design and construction, the AEC industry will certainly learn something from this project (good, bad or otherwise). So net-net, I think this will be good for the construction industry. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed