|

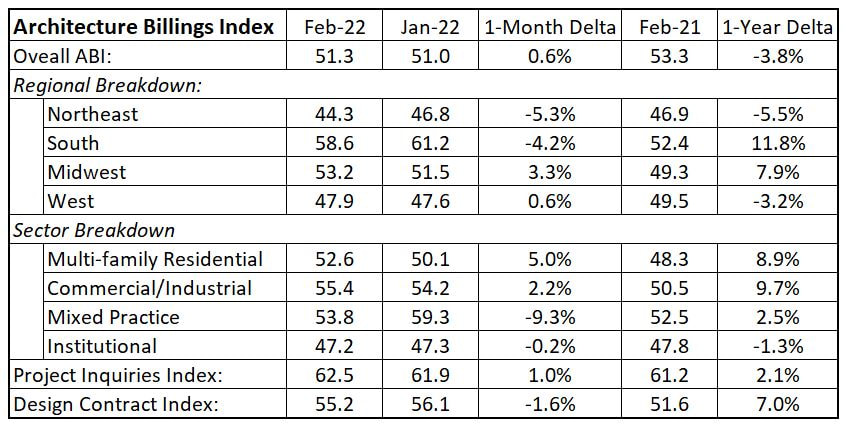

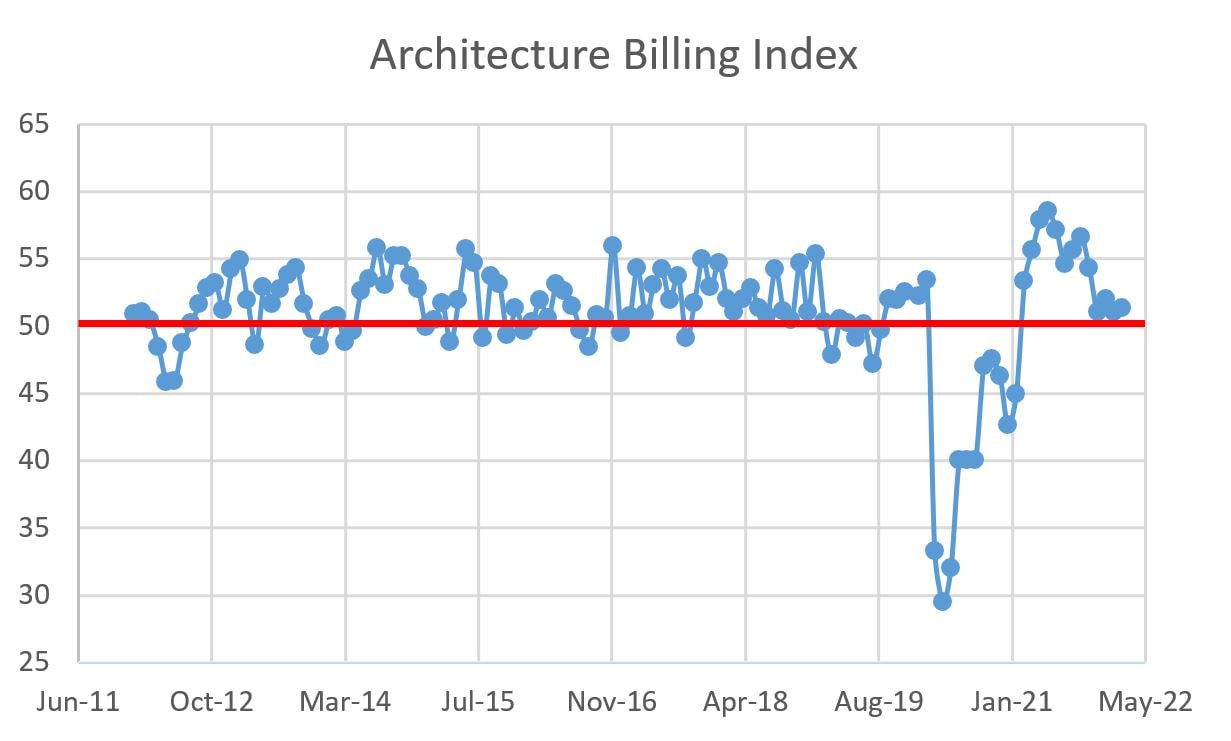

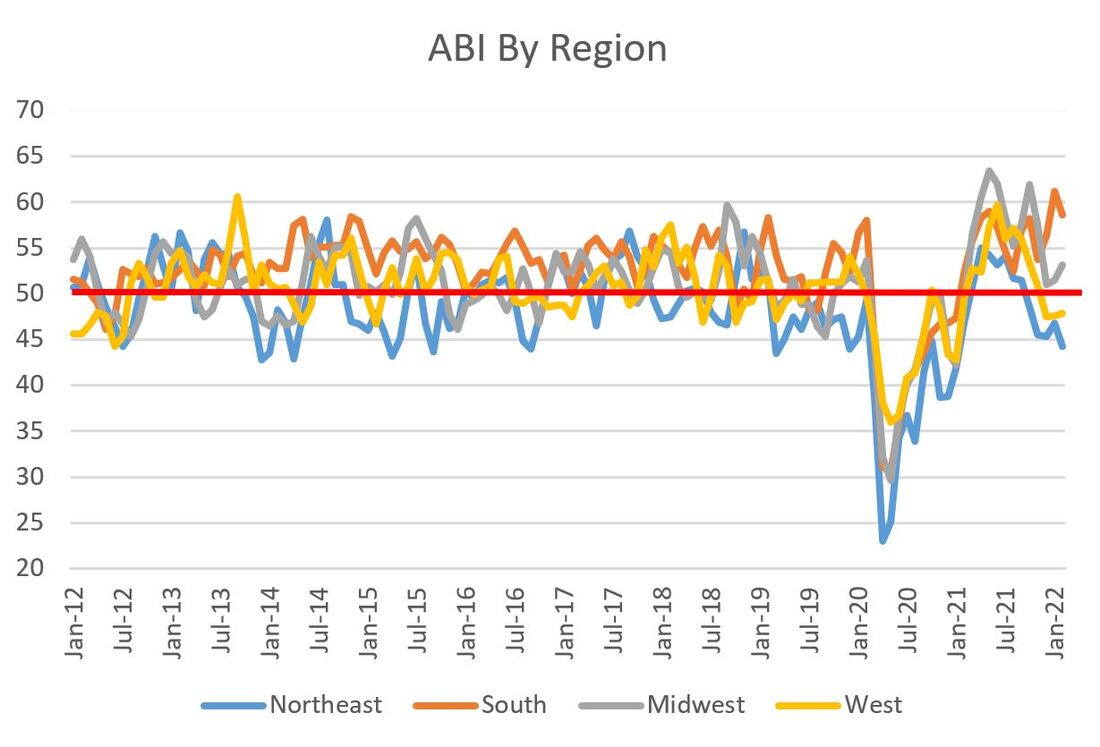

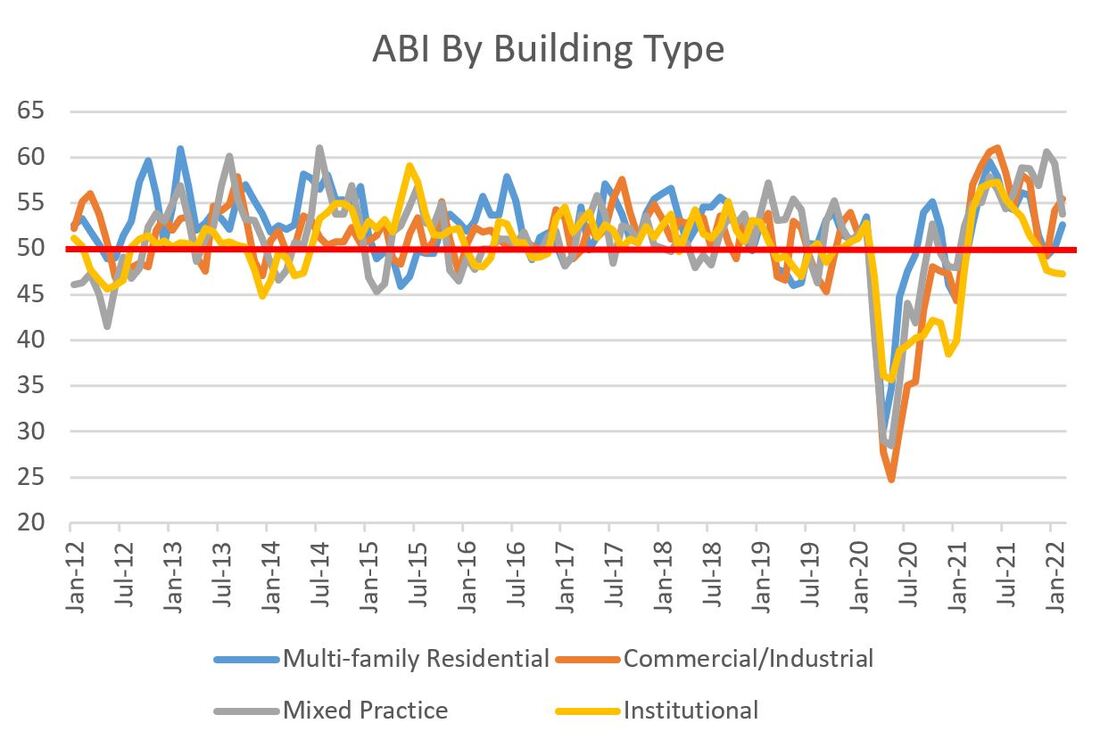

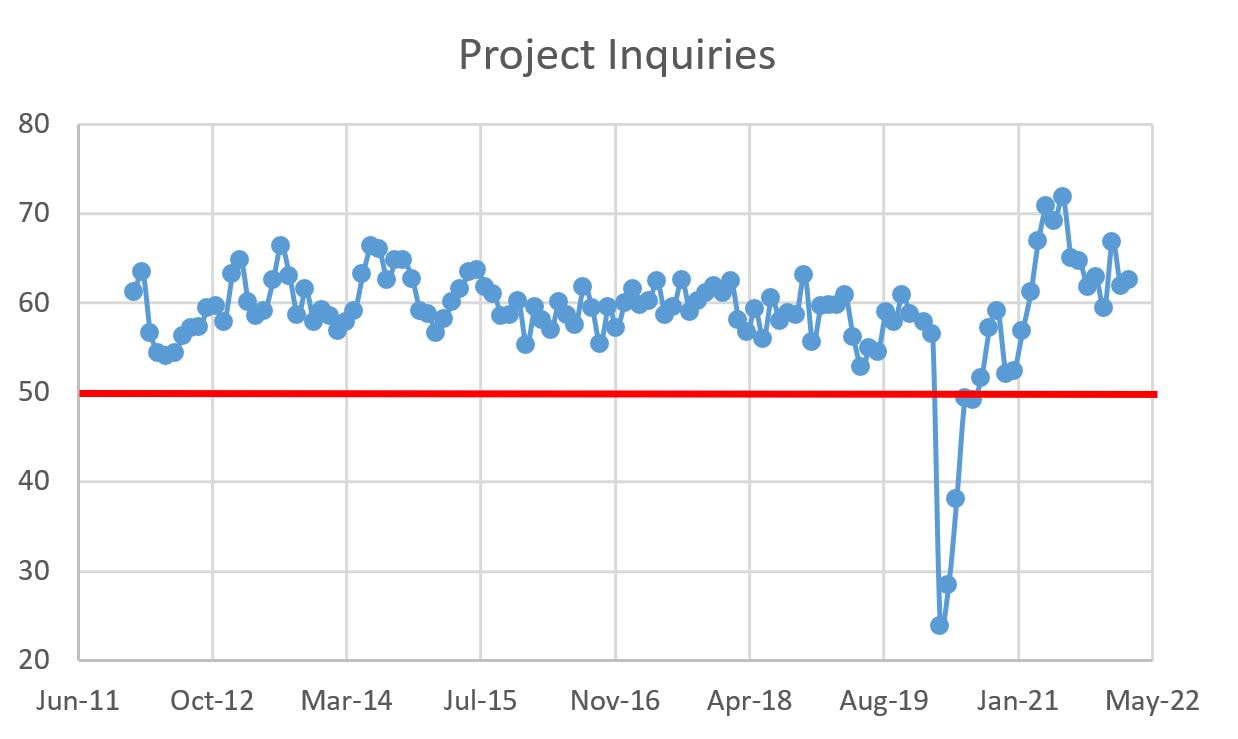

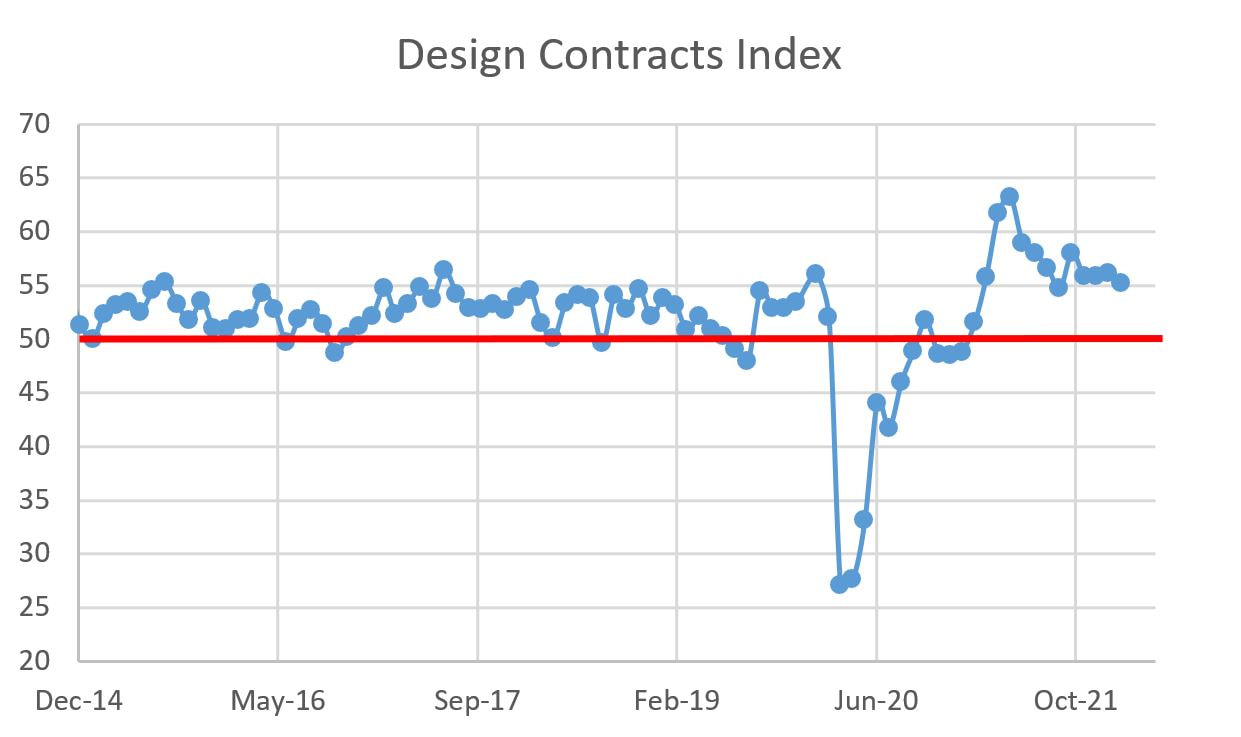

Ok, that title is a bit misleading. This month, there was incremental growth in the American Institute of Architects (AIA) Architecture Billings Index (ABI), with February clocking in at 51.3, up from 51 in January. Under the surface, the regional and sector numbers show a lot of volatility with some big swings up and down. But first, a reminder that the ABI is a nine-to-12 month leading indicator of commercial construction activity, with values greater than 50 signifying increasing design billings and values less than 50 signifying a contraction. Based on the general economy, it should be no surprise that the granular ABI figures are volatile. Last month, I mentioned headwinds facing the AEC industry like material price escalation and a general lack of labor. February looked over at January and said "hold my beer" and introduced a war in the Ukraine that is leading to skyrocketing fuel prices (over $6/gallon in California!). So the fact that we saw any increase in the overall ABI is astounding, not to mention a 5% increase in multi-family (the housing crisis seems to be the only constant) and a nice 3.3% jump in the Midwest. However, the B-side to those gains are sharp drops in Mixed Practice (-9.3%), Northeast (-5.3%) and the South (-4.2%...but don't cry for them or their still lofty regional ABI figure of 58.6). The details are below, but overall, the design and construction industry is still chugging along.

1 Comment

|

Archives

January 2024

Categories |

RSS Feed

RSS Feed