|

Typically, I love receiving AIA's Architectural Billings Index (ABI) figures--it's my favorite economic indicator. But it's definitely less fun when the ABI is less than 50 (any value greater than 50 means that architecture billings are increasing; conversely, any value less than 50 means billings are decreasing). So when April 2014's ABI came in at 49.6, I was a bit disappointed. The silver lining: it's up from March's 48.8 figure. Huzzah…

As always, the details are a bit more revealing. Regional (three month) Averages for April 2014:

The west's slide to contraction is discouraging, as it's been fairly hot for a while. The south is booming and has been strong for a while. Sector Averages for April 2014:

Another bright spot (so long as we're looking for silver linings): the Inquiry Index is at 59.1, up from 57.9 in March. AIA Chief Economist Kermit Baker states that "Despite an easing in demand for architectural services over the past couple of months, there is a pervading sense of optimism that business conditions are poised to improve at the year moves on."

0 Comments

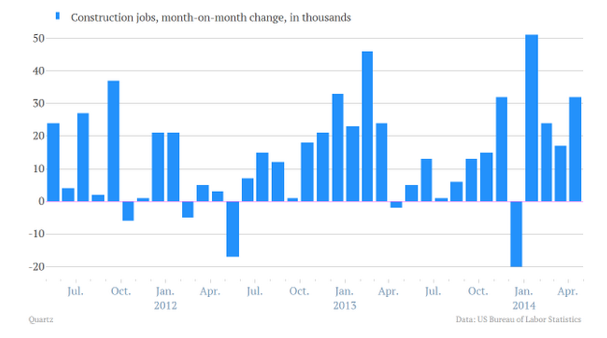

Last week, the U.S. Bureau of Labor announced that the economy added 288,000 jobs and the unemployment rate dropped to 6.3%. For the uninitiated, this is good news. More importantly for this readership, the construction sector is adding jobs at a very healthy pace. Here is the annual change in construction jobs over the past 12+ years: 2002: -85,000 2003: 127,000 2004: 290,000 2005: 416,000 2006: 152,000 2007: -195,000 (the pain starts) 2008: -789,000 (damn, this is beginning to hurt) 2009: -1,047,000 (we were just given a standing eight count) 2010: -192,000 (damn, this is one heck of a hangover…) 2011: 144,000 (so glad that episode is over) 2012: 114,000 2013: 156,000 Through April 2014: 124,000 (372,000 for all of 2014 on an annualized rate) Here is the most recent data in graphical form showing a nice recovery:

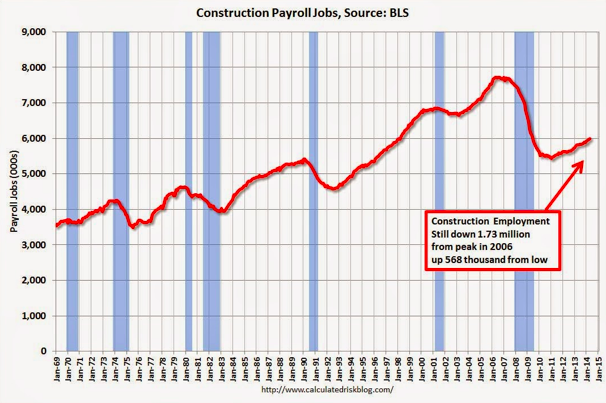

Here's a graph of longer-term construction employment. You can tell that there was one heckuva run up from approximately 1995 to 2006. (Graph from the Calculated Risk Blog)

It is unlikely we'll see construction employment as high as it was in 2006. But the good news is that construction companies are hiring again. This is good for college grads majoring in construction management, civil engineering and architecture. Hiring at Sac State's CM program has been very robust and we may have our third year of 100% job placement for grads in a row.

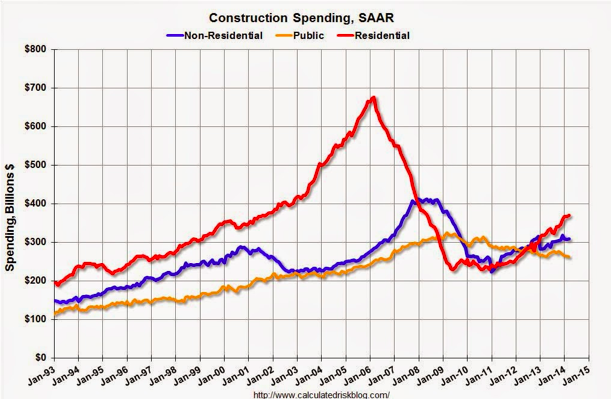

The U.S. Census Bureau reported yesterday that construction spending during March was a seasonally-adjusted $942.5 billion, or 0.2% above February's revised estimate of $940.8 billion. This March 2014 figure is 8.4% above March 2013's number. What's astonishing is that the gains are primarily from private construction projects. It's typically for public-sector construction spending to increase as a means for leading the economy out of a recession. Governments spend on infrastructure, etc. to create jobs (remember the discussions of "shovel-ready" projects that would get funded by federal TIGER grants?) and there was a peak in public-sector spending in early the first half of 2009. But since then, as the economy continues to improve (today's jobs number, an increase of 288k jobs and unemployment down to 6.3% shows an improving economy), it's been the private sector, as far as construction's concerned, that's leading the charge. Private construction's seasonally adjusted rate in March was $679.6 billion, an 0.5% increase from February. Public construction's was $262.9 billion, a 0.6% haircut from February's $264.5 billion number. Everything is off their peaks of past, but we're seeing some nice gains from residential and non-residential construction. Any improvements in public-sector construction, which given that our national infrastructure is in shabby shape and infrastructure will be necessary to support continued housing and commercial construction, will bolster the improving economy.

For more information, be sure to check out this post by Bill McBride.

|

Archives

January 2024

Categories |

RSS Feed

RSS Feed