|

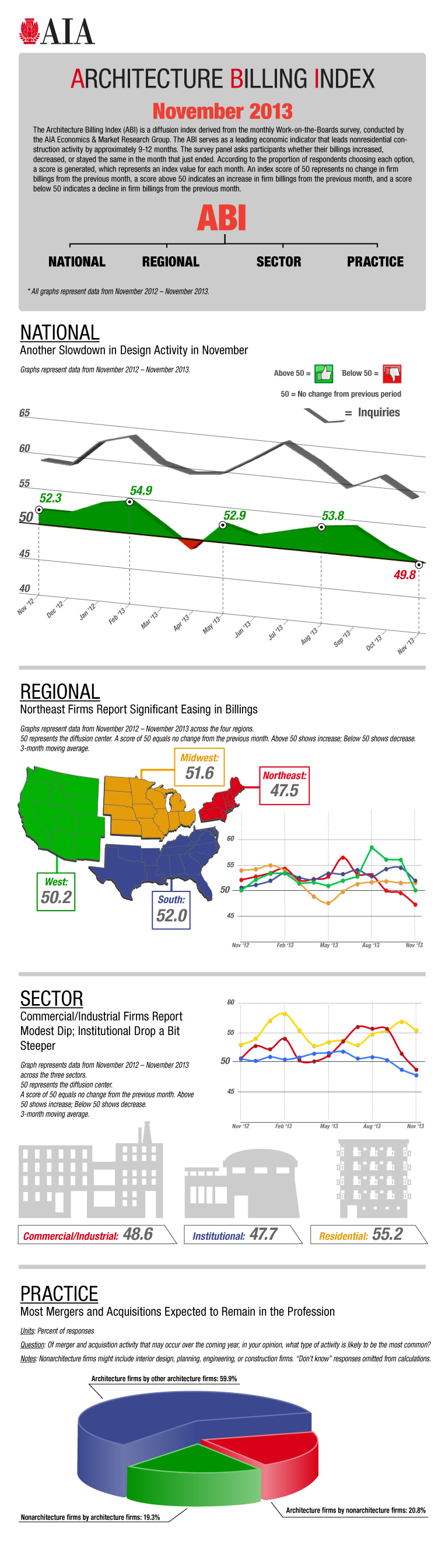

I'm about two weeks late with this (sorry, I was traveling…), but the American Institute of Architects (AIA) released the most recent Architectural Billings Index from November. It's down from last month and November's value of 49.8 is slightly below the Mendoza Line-like threshold of 50 (a value >50 indicates and increase in billings; a value <50 indicates a decrease in billings). The ABI is considered a leading indicator for construction activities. Decreasing architectural billings seems ominous, but like most things in life, the devil is in the details. Most of the pain is being felt in the Northeast. Everywhere else in the country is above 50 (the south has been clearly above 50 all year). Furthermore, in terms of product type, multifamily residential continues to show strength while commercial/industrial and institutional projects have dropped below the 50-point mark. The rundown is below:  The full AIA report can be read here. Anecdotally, this makes sense to me. Many of the 30+ tower cranes in San Francisco are hovering over high-rise residential tower projects, a market that has been strong for some time. It's important to note that the health of macro markets (the West) should not be confused with micro markets (San Francisco). While San Francisco is in beast mode in terms of building, Sacramento (90 mile miles to the east) continues to struggle. While multifamily is picking up slightly in Sacramento (16 Powerhouse, 25th and R), hospital work is the major source of activity in a market that's overall very slow. Like they say about real estate: location, location, location.

1 Comment

|

Archives

January 2024

Categories |

RSS Feed

RSS Feed