|

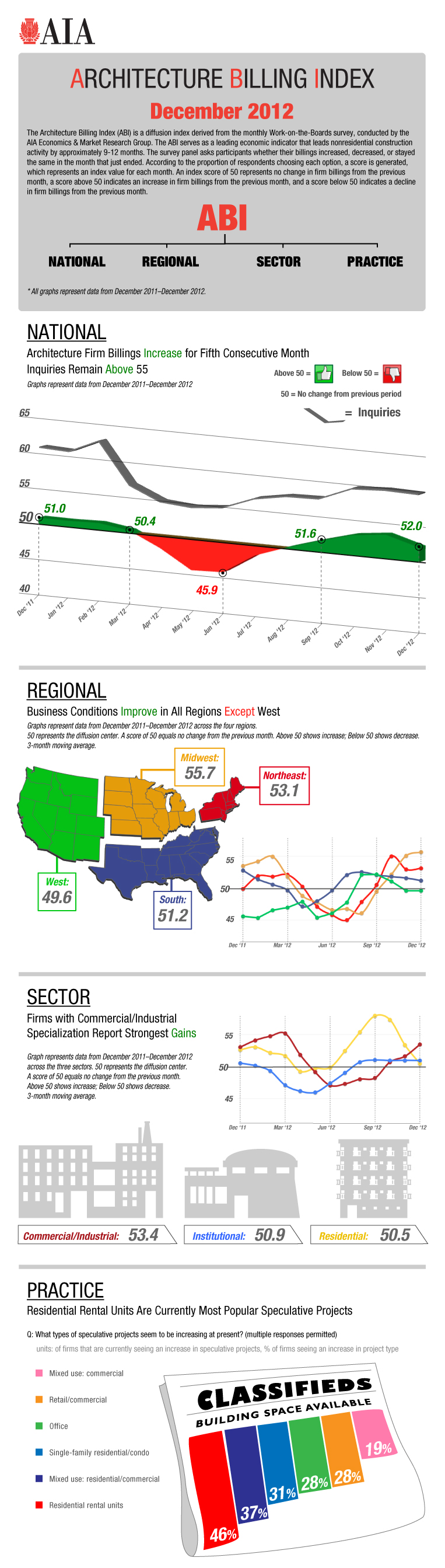

I'm not sure how I missed the November ABI data, but since it's a new year, let's start fresh. And luckily, it's good news. The AIA's Architecture Billing Index (ABI), a leading indicator of construction, is up again, and 2012 finished at its highest since 2007. Booyah! The full press release can be found here.  The only real bad news, at least for us in the west, is that the measure is still slightly below 50 for that region (less than 50 corresponds to a decrease in billings, greater than 50 is an increase in billings). The west has shown some weakness over the past few months, but it's way lows of May 2012. Every sector is above 50, which is also good. All in all, a pretty good report, particularly since the economic recovery is still a bit fragile.

0 Comments

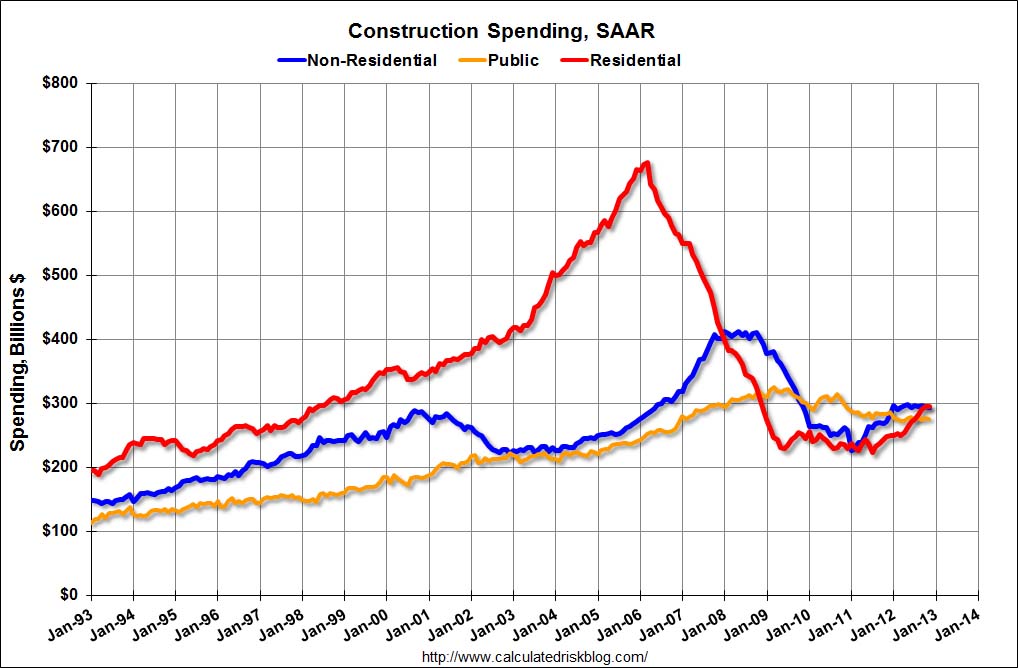

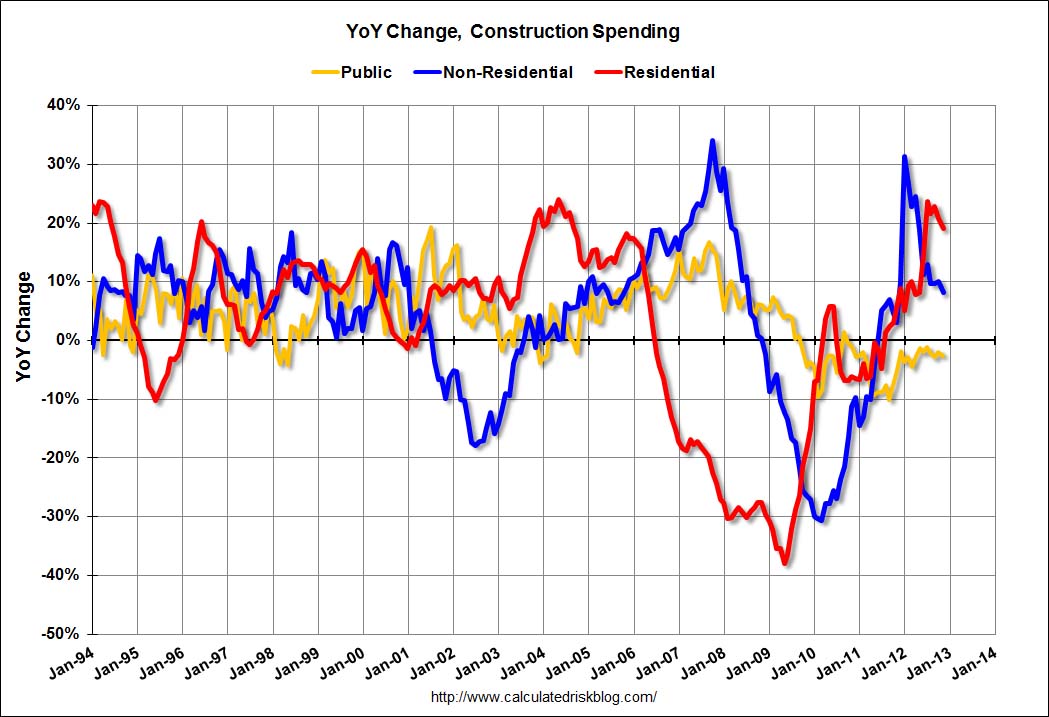

While the stock markets are going bananas over the avoidance of the fiscal cliff, some bad news has come out regarding the construction market. Per Ruth Mantell at the WSJ Market Watch: Outlays for U.S. construction projects declined in November, missing Wall Street's estimates, the U.S. Commerce Department reported Wednesday. Construction spending fell 0.3% in November, while analysts had expected a gain of 0.8%. Spending for October was downwardly revised to a gain of 0.7%, compared with a prior estimate of a 1.4% increase. In November, spending on private construction declined 0.2% while spending on public projects fell 0.4%. Spending on private homebuilding rose 0.4%. Home building is still going strong, but spending on projects municipal and commercial buildings is down. Even worse, analysts were expecting an uptick in building. Yikes! Let's hope this is an anomaly. [UPDTADED January 8, 2013] Here are two graphs from Bill McBride at the Calculated Risk blog that graphically represent how construction spending is trending:   So yes, this recent news is not great, particularly since the current recovery is still in a fragile state, but that can be expected from a weak recovery--there will be fits fits and starts. And this is one data point; a definitive trend cannot be determined yet. Next month's report will be very interesting. The good news is that we're in a much better place than we were in 2008-2010.

|

Archives

January 2024

Categories |

RSS Feed

RSS Feed