|

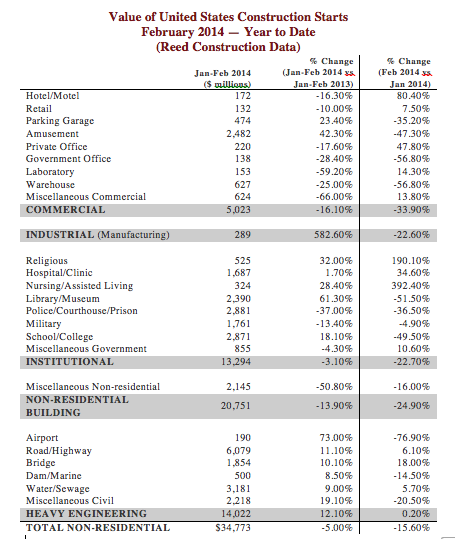

Earlier today, I wrote about how the AIA ABI is showing continues strength in the multi-family commercial construction segment, but also how the commercial/Industrial segment is improving as well. Not a few hours later did I come across the following article stating that non-residential starts are down for the third month in a row. Some of the data from that article is displayed below:

So what gives? My take is that the AIA ABI is a leading indicator which typically predicts construction activity nine to 12 months in advance (it's a measure of architectural billings, which occur well in advance of actual construction), while construction starts are a more contemporaneous measure of construction activities (usually within the past month or so). The winter was particularly brutal on the east coast and midwest, so construction starts were slowed, but that bad weather may not have had the same negative effect on architectural billings. In sum, it will take a while to know exactly how the economy is doing, but hopefully ABI (forward looking) trumps starts (backwards looking) as a predictive indicator of the health of the construction industry.

0 Comments

I just read this article exclaiming "Nonresidential Construction Materials Prices Tick Higher in January." But the title is a bit misleading. Sure, the article says that there have been large recent price increases in cement, natural gas, iron and steel, copper, and architectural metalwork. Ok, that's important and those are key materials for construction. But later, the article states that there have been large price decreases in diesel fuel, asphalt, nonferrous pipe and tube, and construction equipment and leasing. Doesn't this indicate that the price of construction materials is a mixed bag? The key for contractors is to regularly check market prices for commodities and materials as to be aware of the price changes and make sure they account for them in their bids as necessary.

Somehow buried in the article is the slight mention that construction downside risks have fallen. This, to me seems important. The article states that the major risks facing construction economics, albeit small, are issues stemming from a tapering of quantitative easing, debt default in a (none in particular) European country, and a (none in particular) European country exiting the Euro. My favorite leading indicator of soon-to-be construction activity was just released. The AIA ABI figures for February 2014 were just posted and there was another slight improvement, from 50.4 in January to 50.7 in February, for the aggregate nationwide number, which is great. Any value greater than 50 means that architecture billings are increasing; architecture billings are a nine to 12 month leading indicator for construction activity. But the devil is in the detail, which are shown below:

Regional Averages for February 2014:

That last value is of particular importance to me because most of my students work or will work on the west coast. While certain regions (San Francisco/San Jose Bay Area) are still very strong, the recovery elsewhere has been slow to materialize, if there even is a recovery. Hopefully this turns around soon. Sector Averages for February 2014:

As has been the case for several months, the multi-family residential market continues to pace commercial construction. In talking to contractors that serve this market, it sounds (anecdotally) that there is still room to grow, with one contractor in particular telling me that they are beginning to turn work away because their backlog is bursting. The increase in commercial/industrial is also promising. Project inquiries declined to 56.8 from 58.5 in January and from 59.2 in December. Multi-family continues to drive the construction industry. Based on my previous post, hopefully |

Archives

January 2024

Categories |

RSS Feed

RSS Feed