|

In spite of being healthy for the overwhelming majority of 2015, the architecture (and by extension, construction) industry are showing some signs of weakness. These may be the side effects of widespread anxiety that are also showing up in angry politicians domestically, global geopolitical uncertainty, falling commodity prices (oil!), all of the above or none of the above. It is also unclear as to whether this is a trend or an outlier, but nonetheless, architecture billings fell last month and that's something we in the construction industry should be watching.

Let's review the hard data, but first the obligatory background: the ABI records architectural billings on commercial building projects. Any value greater than 50 means that architecture billings are increasing; conversely, any value less than 50 means billings are decreasing. The ABI is a leading indicator of commercial building construction by approximately nine to 12 months. The composite January 2016 ABI figure was 49.6, down from 51.3 in December 2015, showing a contraction in architecture billings. In similar fashion, the new project inquiry index declined to 55.3 in January, down from 60.5 in December. While this is far from great news, remember that one data point does not make a trend. Here's are things are stacking up in your neck of the woods:

Sector Averages for January 2016:

One last reminder, this is one month's worth of data. No need to quit the industry just yet. Long term trends are still very positive, but it may be time to focus on building a career with a stable company. If downward trends continue, as would not be unexpected given the tear the AEC industry has been experiencing for a year (or more, depending where you live in the U.S.). The crazy period of contractors hiring people as fast as possible may be ending (or at least cooling) and they will become increasingly choosy.

0 Comments

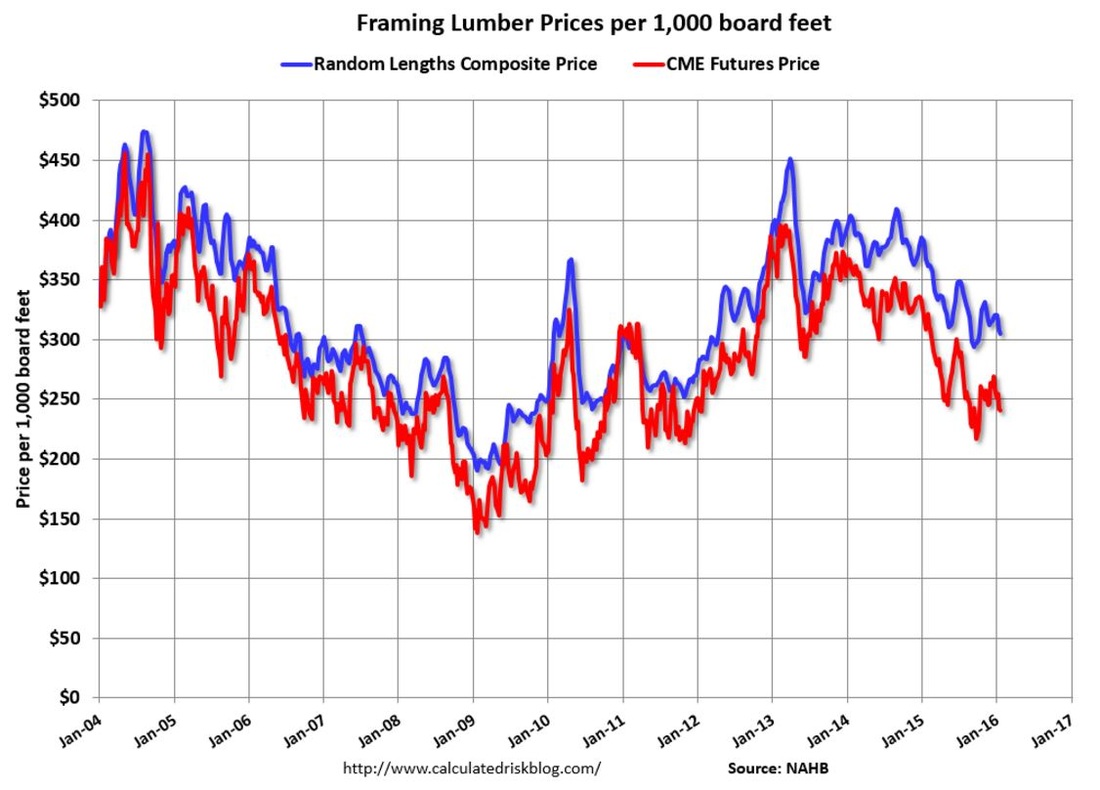

Here's some bonus economic news: the price of framing lumber is down since last year. You should definitely read Bill McBride's take on this (and follow his Calculated Risk blog on Twitter), but here's the Cliff Notes summary.  The latest construction industry employment data dropped last week. First the good news: 18,000 jobs were added, dropping the industry's unemployment rate to 8.5%, its lowest level in 17 years. Better yet, wages are starting to creep up, which is a sign that employers finally recognize that they need to pay for top talent. Now the bad news: 18,000 new jobs is great, but it actually represents a declining rate of job creation in the industry. The long-term employment needs very high, particularly in craft labor and replacing retiring baby boomers, but the decline in hiring may be another signal that the super hot market for projects is cooling for the near term.

So why do I bring this up? Well, for Sac State CM grads, the last few years have been very good. Our 4 (5?) year streak of 100% employment shows all signs of continuing this year, but the days of multiple high full-time offers simply because you received your degree may be over. Next year's graduates may have to work a little harder, but thankfully they've leveraged the strong job market over the past few years to get great internship experience (and because they're a relatively small class, they won't overwhelming oversupply the job market). But for you younger students, the competition for internships will likely become fiercer, so consider participating on an ASC competition team (if you aren't already), getting an internship sooner than later (maximize the job market in your favor while you still can) and prepare to fight a little harder in the future for internships and full-time jobs. As the Navy SEALs say, "the only easy day was yesterday." CapEx is short for capital expenditure. It represents money that businesses use to purchase or upgrade physical assets, such as property, plants, equipment, etc. Why is this important? Well, a recent article has stated that CapEx investment in the U.S. is on the decline. This trend started in the energy industry (e.g. the oil extraction and processing), but is spreading outward. When companies allocate less funds for CapEx, that means construction activity decreases. Think about it: every time Amazon allocates money for a new distribution center or Google for a new R&D center, physical buildings (and the associated infrastructure) usually needs to be constructed. CapEx goes to more than just construction projects, but a lot of assets bought with CapEx budgets need to be constructed. This could be another clue that the construction industry is headed for a slowdown in the near term.

The Associated General Contractors of America (AGC) reported today that says, in a nutshell, that construction spending was strong for 2015 but tailed off towards the end of the year. Construction spending in December was measured at $1.117 trillion seasonally adjusted annual rate (SAAR), which was 8.2% higher than the rate measured in December 2014. However, the rate was only 0.1% higher than November, which was already revised downward. What does this all mean? The construction market has been fairly brisk throughout 2015, but what remains to be seen is whether the industry is now just catching its breath or if it's completely winded.

Focusing on the bright spot, the multi-family sector of the industry is strong, as I mentioned nine days ago.Multi-family defied the December slowdown and jumped 2.7% last month and was up 12% year-over-year. Compare this to the single-family market, which was up 1% in December and 8.7% since 2014. It will be interesting to see how this growth plays out in the future and I plan on looking into it deeper. The rate of spending for private non-residential construction fell 2.1% from November 2015 to December 2015 but was up 11.8% from a year previous. Public construction was up 1.9% in December 2015 from the previous month and up 3.9% from a year ago. Public construction has been fairly stagnant for a few years. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed