|

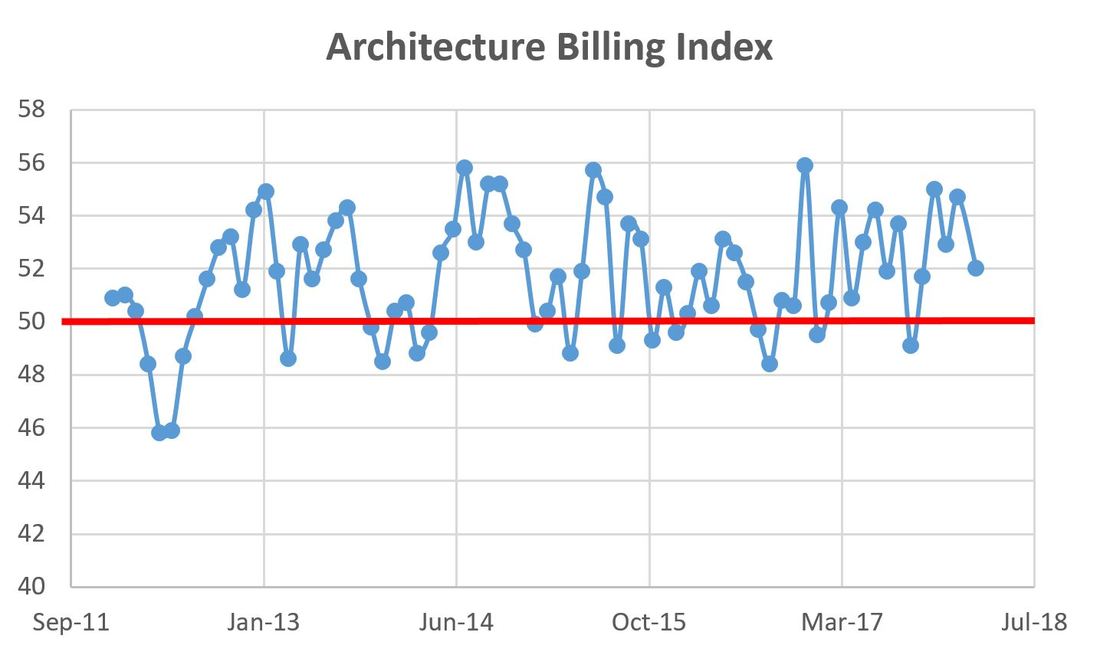

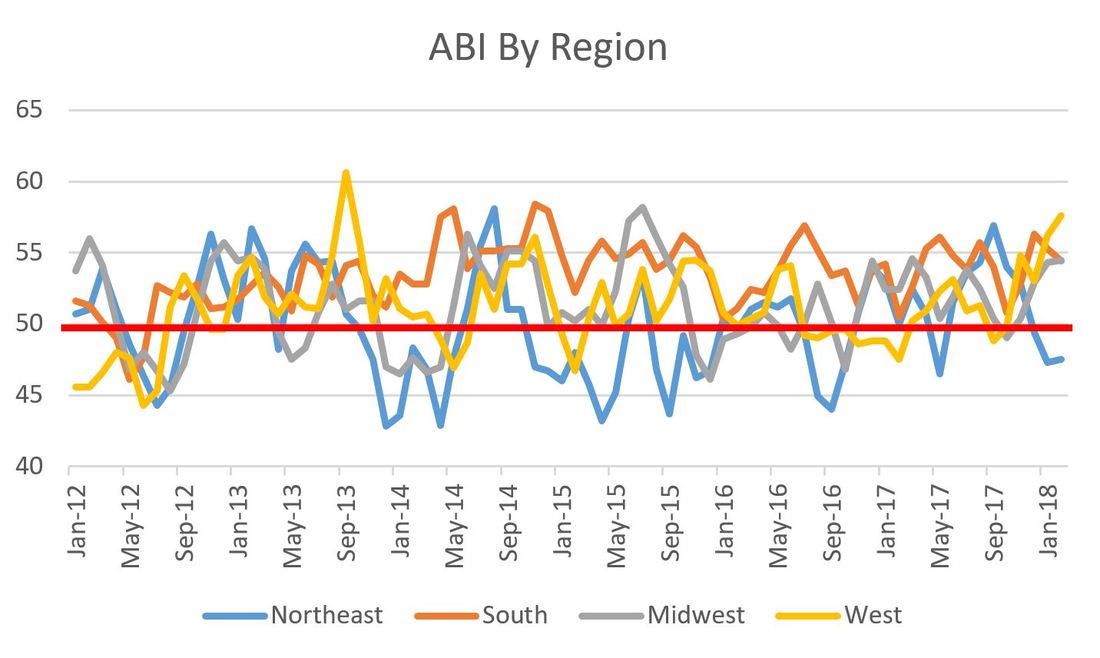

I was so busy last week that I almost forgot to report on my favorite forward-looking economic indicator for the construction industry: the Architectural Billing Index reported by the American Institute of Architects. While a one month dip is no need to panic, I kind of wish I had forgotten to check for an entire month. February 2018's ABI came in at 52, a sharpish drop from January's 54.7. Drops happen, even in strong construction markets (recall a drop from 53.7 in August 2017 to 49.1 in September 2017). And the number is still above 50, so that means billings are increasing, albeit slower than last month. Per my typical spiel, any value greater than 50 means that architecture billings are increasing; conversely, any value less than 50 means billings are decreasing. The ABI is a leading indicator of commercial building construction by approximately nine to 12 months.  Here's is the regional breakdown for February 2018:

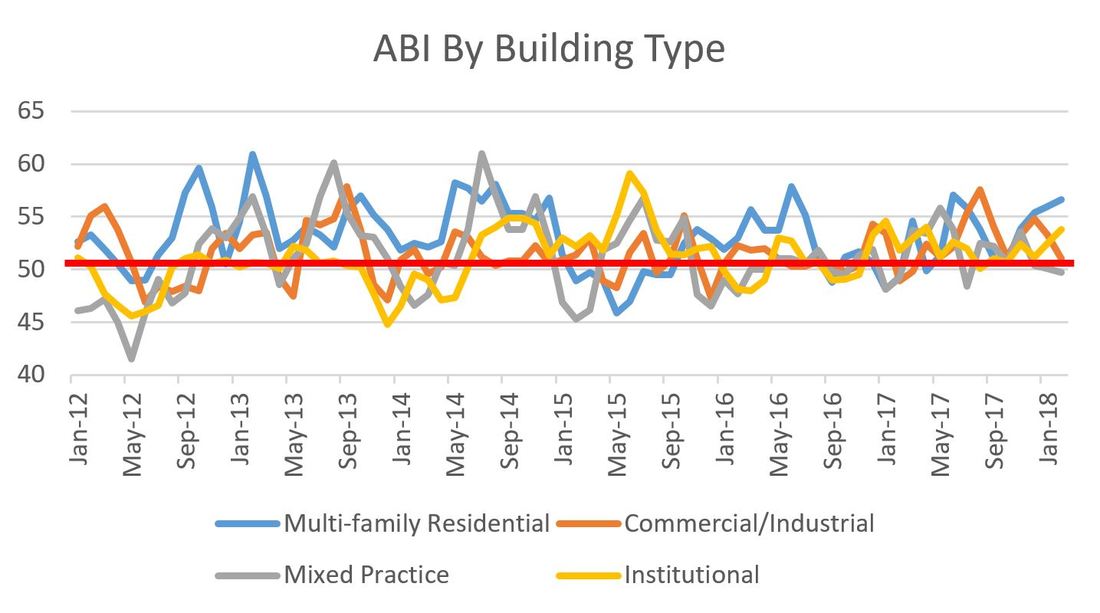

Sector Averages for March 2018:

So, yes, the ABI declined in February, yet it is difficult to even insinuate that this is the canary in the coal mine for a wide market cool down. Even though the thin labor market, skyrocketing material prices and trade wars have people nervous, the bad news thus far is really localized to the Northeast and, to a lesser extent, the Mixed Practice sector. Stay tuned to next month to see if the next data points point to a negative trend.

0 Comments

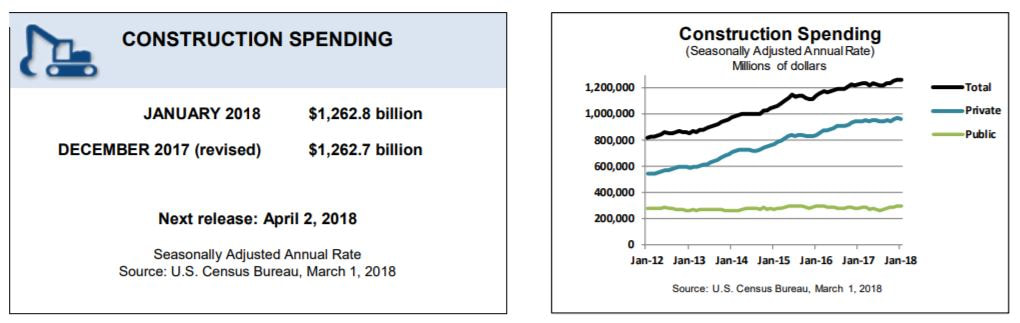

The United State Census Bureau reported construction spending for January 2018. Overall, spending in January 2018 was basically the same as December 2017 ($1,62.8 billion in January versus $1,262.7 billion in December) and up 3.2% from January 2017 ($1,223.5 billion). Private construction dipped 0.5% from December to January due mostly to a decline in non-residential construction (residential was up slightly). Public construction was up 1.8% from December to January based on strength in the education and highway segments. The full press release can be downloaded here.

|

Archives

January 2024

Categories |

RSS Feed

RSS Feed