|

In a recent post, I wrote that capital expenditure (capex) spending, which includes the money allocated for building physical structures such as offices and manufacturing plants, is down, due in large part to uncertainty. That was a very blanket statement that doesn't apply to all companies. Take Amazon, for example. In the past five years, Amazon has spent $5.3 billion on capex, with $2.4 billion (43%) of that in the past 12 months.

So how, after such a painful economic downturn, can Amazon allocate so much money to capex? Simple: they have the cash and are using it wisely. Surely, Amazon is taking advantage of a soft construction market to stretch their capex dollars, of which they have $5.25 billion on their balance sheet. Know who else has a lot of cash on their balance sheets? Google ($16.3 billion) and Apple ($10.7 billion). Both of those companies are also investing heavily in capex. Apple had the best general contractors bidding for its proposed new campus. They get the benefit of high competition between reputable builders and relatively lower prices. The bottom line is that the market for commercial/industrial construction is tough, but there are some bright spots. In order to get that work, though, builders need to have a strong reputation to be invited to bid, meaning only a few will benefit from these capex expenditures.

2 Comments

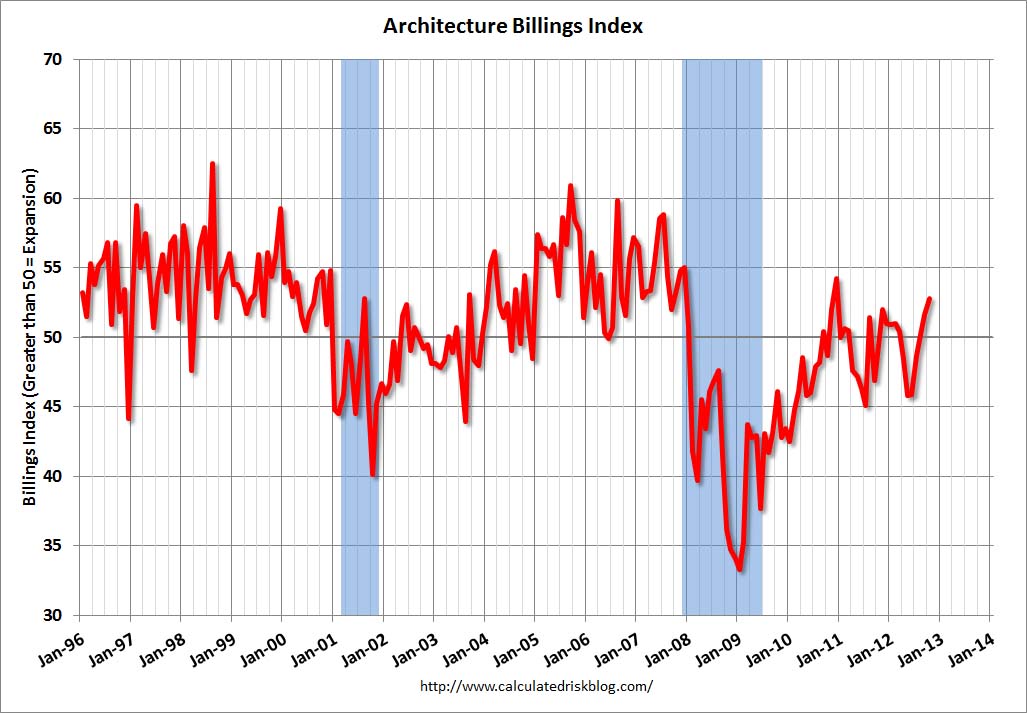

Architectural billings may be signalling a turn in the economy, but the gains are being localized is certain segments. Noted economist Nouriel Roubini tweeted today "Cash-strapped US consumers apparently cheery & spending while cash-rich US firms cutting sharply on capex [capital expenditures] spending & cautious on hiring." I think that summarizes the current market and builders need to be aware of that sentiment. Just before Thanksgiving, the American Institute of Architects (AIA) released their most recent Architecture Billing Index (ABI) figure. This measure is considered a leading indicator of non-residential construction by 9-12 months (and I'm assuming this means single-family home building is not included but multi-family housing is included since residential billings are a part of the measure). The October ABI score was reported as 52.8, up from 51.6 in September (measures over 50 signal increases in billings and measures under 50 signal decreases in billing). Even better, the October ABI for new projects was 59.4 versus 57.3 in September. Since design is *roughly* 10% of a building's cost, even modest increases in architectural billings can be leveraged into much larger amounts of money being allocated for building construction in the following months. If this is the case, these positive trends in ABI could reverse corporate America's reluctance to invest in capital expenditures like buildings and other facilities (as I discussed below on 11/20/2012--"Manic news for builders). ABI values over time can be seen in this figure created for the Calculated Risk blog (http://www.calculatedriskblog.com). The trend has been upward (albeit choppy) since January 2009:

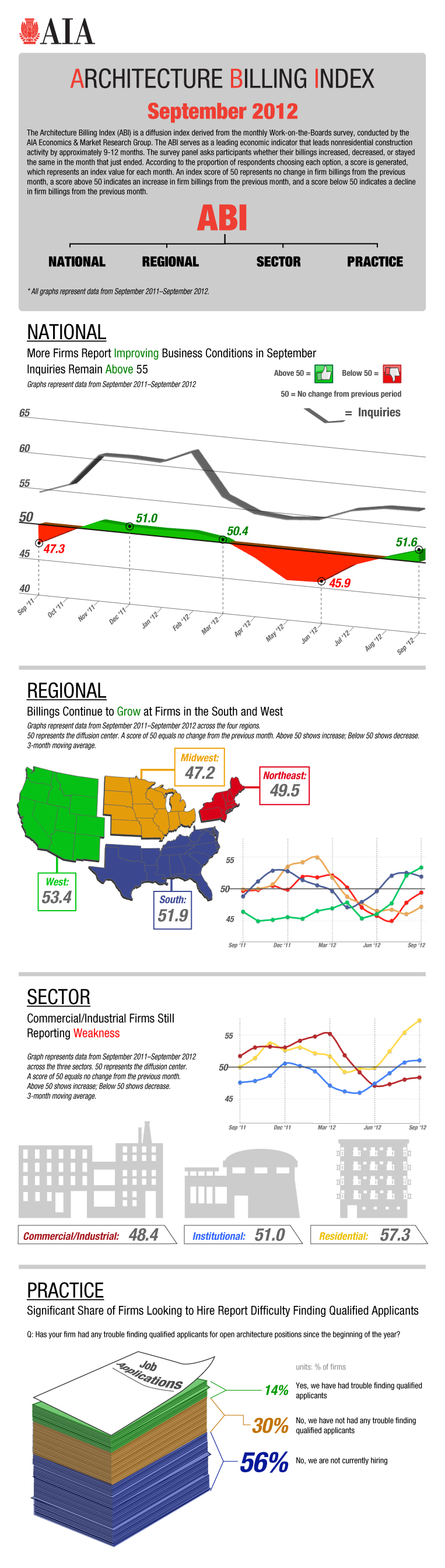

But like anything else the devil is in the details. Let's dig into the AIA's report, which can be read here but is nicely summarized in this figure produced by the AIA:  To access this figure, click here. The gains in ABI have been concentrated in the south (which has been growing faster than most regions in the U.S. for some time, relatively speaking) and the west (which was hit harder in the previous recession, again relatively speaking, and thus likely to see a bigger rebound). Also, the gains in ABI are due mostly to billings in residential, with some gains due to institutional (in northern California, hospital, prison, and university work seems to be the overwhelming majority of building construction, so this doesn't surprise me). (As a side note, it seems to me that institutional would likely follow housing, as schools and hospitals tend to be built as housing is built, but that's a very simple hunch on my part.) Commercial/industrial is a drag on ABI and this indicates there is decreasing amounts of this work in the pipeline for contractors.

There are some other things people need to be aware of. While these positive trends in ABI for residential, combined with recent bullish news coming from single-family home builders, is good news, it's contingent upon some trends that must be mentioned. First, much of the home buying is due to policies that are driving the cost of borrowing for a home down. With the Fed keeping rates low, mortgage rates are also low (a 30-year mortgage at 3.75%? Yes, that's really good for a borrower!) and quantitative easing injecting money into the economy, right now is a great time to buy a house, assuming you can qualify for a loan. Second, the housing market is being buoyed by $25-30 billion (yes, billion with a "b") in private equity investors buying homes with the intent to rent them (Barry Ritholtz states that this buying could be 20% of the current market in this video). Barry continues to point out two very important issues that will change the housing market for the worse if they occur: 1) if the U.S. falls back into a recession, all of those PE buyers will bail out of their housing positions and flood the market, which will cause the housing prices to drop. Secondly, if policymakers at the federal level (the President and Congress) choose to eliminate or cap interest mortgage deductions, the market for housing, whether it be for single- and/or multi-family homes, will drop like a stone. This second issue is unlikely, as mortgage deductions are very popular with voters and thus messing with them would be political arsenic for elected officials, but it's being contemplated as a measure for national debt reduction. The bottom line is that architectural billings are up, which is a good sign for the building industry, but the constructors need to be cautious. First, the gains in billings are in the housing (and, to a lesser extent, institutional) market sector, which is being driven by favorable macroeconomic factors that have a finite shelf life should the economy not see more wide-spread improvements. Secondly, businesses still seem reluctant to invest in capex such as buildings and industrial facilities. These two issues are, on some level, related (although it's way above my expertise to explain why). I'll feel a whole lot better if/when the commercial/industrial portion of the ABI measure improves. News from Apple this morning stated that construction on the company's mammoth new corporate campus in Cupertino has been delayed. My first reaction was that there were either delays in environmental impact reports or in the permits from the city or state. This report from Bloomberg states that the city council still needs to approve the plans (which were originally submitted by Steve Jobs), which makes sense as the plan check process for this multi-billion dollar project is probably tough for Cupertino to swallow quickly. The state seems to be less of an issue, seeing as it granted an expedited permit under the new Jobs and Economic Improvement through Environmental Leadership Act. The delays were announced as an Apple representative also said that the design for the project had been changed. The design changes were not requested by the city. I suspect (and we're all forced to suspect because in typical fashion, Apple is being fairly opaque with specifics) that the changes fall under the category of value engineering. A few months ago, the rumor mill "revealed" that a joint venture of DPR and Skanska was awarded the project (my friends at DPR, to this date, will not confirm this even though it seems to be the worst kept secret in the construction industry). Since the construction contract award, the proposed design changes include removing a foot bridge, adding a central utility plant, and changing the site grading plan so that there is no soil off haul, among others. Those types of design changes have the finger prints of value engineering all over them. These types of changes are not unexpected--when you go through the painstaking process of hiring a general contractor for such a costly project, some of the selection criteria typically include providing services for value engineering in the effort to save costs. So while the delays on the city permitting side may be slightly bad news (as the tone of the Bloomberg video embedded in the article suggest, those are really just the types of inconveniences that projects of this size attract. If the other side of the delays involve value engineering, time/cost trade-offs are very likely worth it to Apple.

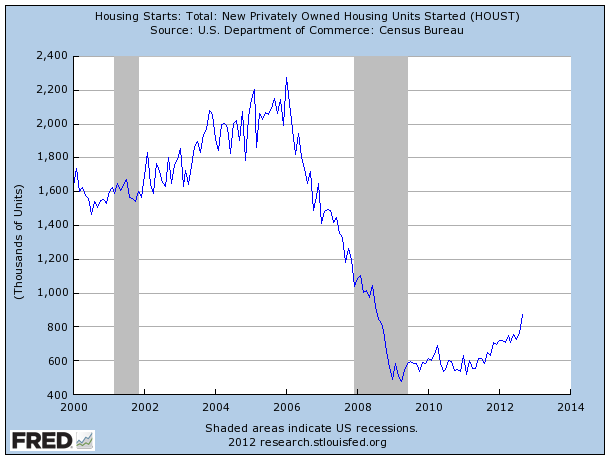

While still below the frothy levels of 2005 and 2006 (which is a good thing), the housing market seems to be making somewhat of a comeback. This sentiment is not based solely on today’s homerun report that there were 894k housing starts this month (above the forecast of 840k and more than the 872k last month). There’s actually several months of positive trends.

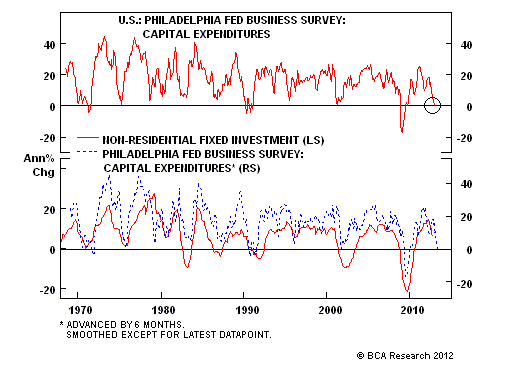

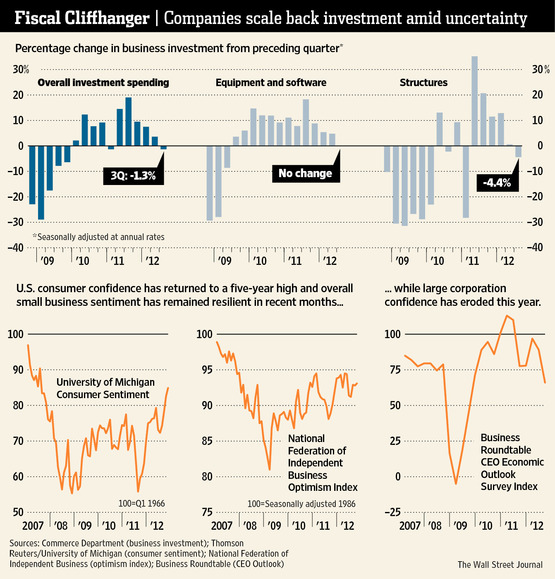

The housing market is not without its issues. Many people have been reducing their levels of household debt (deleveraging), although this great article by Joe Weisenthal presents the idea that a balance sheet recovery may be leading people to borrow money for housing. But for even those that want to buy, capital is still tight. Just because rates are low doesn’t mean that mortgages are easy to get. But with shrinking inventory and housing starts increasing, the news seems to be positive for homebuilders and, by extension, construction related to homebuilding. But what about private industry? Well, that’s a different story. Companies investing less in capital expenditures. Similar to families, companies are trying to reduce their debt levels and are decreasing the rate of investment in new facilities (or “non-residential fixed investments” in the figure below).

The better figure is the one below. It echoes the sentiment that companies are bearish on building structures, as investments are down 4.4% (see upper right graph in the figure below). A big reason for this pessimism: there is a general lack of confidence which may be the product of policy fear, market fear, regulatory fear, etc. Confidence is much higher than it was in 2009, but it’s trending downward in 2012 (see lower right graph in the figure below).

The bottom line is that homebuilding looks good, particularly in a market segment looking for good news, but commercial and industrial builders should still be cautious, as their corporate clients seem to be holding back on capital investments in structures.

Over the last 40 years, many industries were enjoying vast improvements in productivity. Much of that productivity was due to the widespread adoption of information technology (IT). Once WinTel computers and connectivity became the norm, information flowed relatively freely between employees and employees, and people could produce, analyze, and communicate data at increasingly faster rates. However, many of these productivity gains from IT were largely missed by the construction industry.

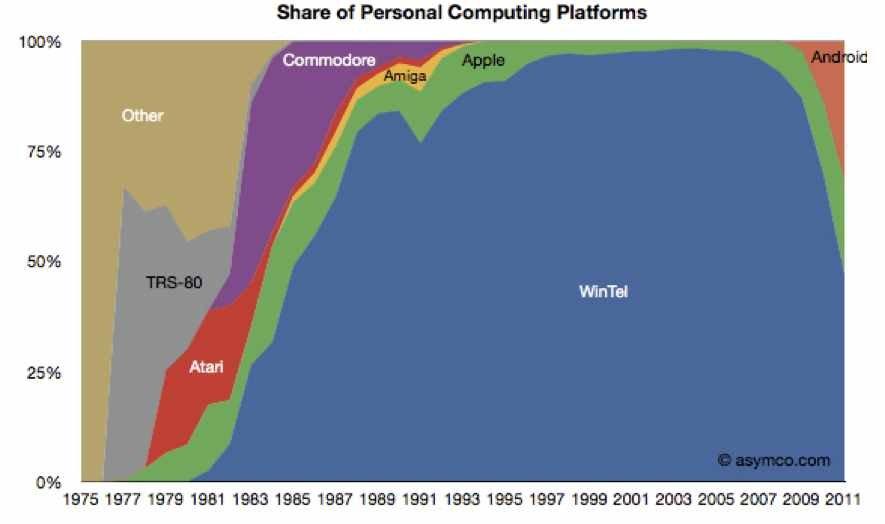

There are many reasons why the IT revolution silently passed the construction industry. Two of these reasons are that technology companies, primarily in software development, were reluctant to build software for builders. First, construction companies are cheap, particularly when it comes to new technologies. The rate of R&D spending in the construction industry is paltry at best. I don’t have the exact figure, but it’s maybe 1-2% of revenues. R&D does not equal technology adoption, but suffice it to say, contractors are, by and large, not technology savvy. The second reason, which is related to the first, is that many of the people in the construction industry are luddites. The visual of the crusty superintendent in the field resisting every effort to become more digital is not that far off. So, when you couple a parsimonious industry with people that resist your products, it’s no mystery why all but a few software companies ignored the construction industry. These issues are rapidly dissipating. Many companies, from tried and true construction technology developers (see this robot being built by DPR and Trimble) and some Silicon Valley start-ups (PlanGrid being my favorite), are building new products for the construction industry. At the same time, there’s a huge turnover in talent in the construction industry. As many (technophobic) baby boomers are setting off into retirement, they are being replaced by a new crop of newbies that have grown up with computers and cell phones and are very comfortable with the onslaught of new software and hardware products. This new generation of construction professionals is important. The construction industry, like all industries, will need people that are comfortable with an ever-changing technology landscape. Whereas technologies of past decades took years to be adopted and even longer to be made irrelevant, the lifecycle of technologies coming online today are being rapidly adopted and are made obsolete just as quickly. In the figure below, look how long it took society-altering technologies, such as electricity and radios, to become widely adopted. Now look at computers, cell phones, and the internet. The adoption of new technologies is happening much faster now. What’s more, technology is being developing at an increasingly faster pace with prices for products dropping (see Moore’s Law). It’s almost impossible to fathom what the technology landscape will look like in the construction industry in a decade, but I’m willing to bet green money that it will look dramatically different than it does today.

And this doesn’t just apply to “macro” technologies (computers, phones), but also “micro” technologies (operating systems). A decade or so ago, when builders decided to invest heavily in computers, much of the risk was mitigated by the fact that the world was dominated by WinTel machines (computers with Intel processors and the Windows operating system). The biggest decision was HP vs. Dell, which was a decision based primarily on cost (with service as possibly a consideration). Now, there real competition among operating systems, and the market will likely get more fragmented in the near future.

So what does this mean for builders? Well, putting it simply, builders need to become savvier. While that sounds incredibly trite, it means that the ENTIRE company must become more savvy. Not just the IT manager and staff, but also senior management, office personnel and field personnel.

Going forward, I will be offering my thoughts and analysis on the subject of technology in the construction industry. But in the near term, I want to mention some key developments that are going to dramatically affect the construction industry: BIM: If you work in the construction industry and haven’t heard of BIM (building information modeling), then you must be living in a cave. BIM is a perfect example of what smart investment in IT can yield. BIM allows contractors and subcontractors/trade partners to perform clash detection before materials are actually installed, saving critical time on site layout and, even better, avoiding rework or late problem discoveries that may lead to project delays. What’s even better about BIM is that it has increasing returns, meaning that the more people that use it, the more valuable it is. That helps increase its return on investment made in BIM for all parties that make the investment. Cloud computing: Almost everyone has heard of the cloud by now, which is good. Even better about the cloud is that it allows project participants to share data easily, irrespective of the device or operating system they’re using (so long as you have an internet connection and a credible web browser, but that should also be a given. If it isn’t for your company, contact me ASAP!). Most of the contractors I communicate with on a regular basis are already leveraging the cloud with high returns. BYOD: BYOD, or bring your own device, means that many of the people participating on a project are bringing their own computing devices (smart phones, tablets, laptops, etc.). Unlike the past, when IT managers only had to worry about building a system around WinTel machines, they must now be prepared to work with wide variety of platforms. Managing a network consisting of phones, laptops, desktops (yes, they still exist) is enough work, but managing those devices with a multitude of operating systems, such as Android, Windows, and iOS further complicates things, particularly when many of these devices are owned by individual employees. And not to cry that the sky is falling, all of this leads to security issues, both between devices and between people. When individual employees walk out the door each night and can take key project information with them on their devices, you had better be thinking about managing data security. The point I want to leave you with is that technology is coming furiously to the construction industry, much faster than it has in the last 5 to 10 years (much faster!). This is a good thing. But companies, from top management on down to the lowest ranks, must be aware of this change and prepare properly in order to see a positive return on investment (or simply to not be run over). There are many more issues to discuss, so I will periodically write about them here. Until then, happy computing.  Construction materials have seen their overall composite prices fall this year (see line for Industrials, which includes building materials, in the figure to the left). Some key construction materials that have seen price declines includes steel (down 1.9% in October) and plywood (down 1.8% in October) However, because of price increases in some key building materials, materials prices are still outpacing the increases in contractors' bids. According to Ken Simonson, chief economist for AGC, the price gains in diesel fuel (up 2.3% in October) and copper (up 2.8% in October) have continued to put pressure on contractor bids. For more info, see this article and check out the AGC list for Producer Price Indexes here.

Last night I wrote that positive trends in real estate, specifically reduced inventory and increased starts (see below), was a positive sign for the construction industry.

Well, I may have spoke a bit too soon. In a conference call today, D.R. Horton CEO stated that "I don't see a lot of jobs being created." This is bad because a rally in home building, and thus the infrastructure related to home building, are tied to low unemployment. High unemployment is bad for home builders because it leads to higher mortgage delinquencies and foreclosures. So the market for new homes may stall out until more jobs are created.

So that's the ugly side of today's manic news. The good news is that the demand for single-family rental homes is surging, up 25% over last year in some cities and up in 22 of 30 markets tracked by CoreLogic (as reported this article in the WSJ). This is natural in slow markets. With unemployment high and credit for new home buyers tight, renting is a logical solution for many people. However, here's what's good for the construction industry. There is a lot of institutional money flowing into this market, which has long been dominated by mom-and-pop buyers that managed a few properties at a time. If large investors have a lot money allocated to an asset class that has seen it's supply decrease by 11% since last year, either a) the price of rental properties will increase, b) more rental properties must be constructed (spurring new construction and the infrastructure to support it), c) or both, generally speaking. So the housing market news is still mixed but trending good in my humble opinion. Unfortunately, it's heavily dependent on reducing unemployment. Per the Calculated Risk blog (a good one is you're a finance junkie), there's good news coming from homebuilders. For the complete story, click here. This excerpt is the best part:

"As at September 30, D.R. Horton sales order backlog of homes under contract jumped 49 percent 20 7,240 and the value of the backlog increased 61 percent to $1.7 billion." Most of my readers are likely not going to work in the single-family housing construction market, so why is this important? Well, the key word is backlog. There has been good news coming out of the homebuilding market recently, but my hunch was that homebuilders were selling the houses that they overbuilt during the housing bubble and were trying to reduce a glut of inventory. But this data suggests otherwise and that much of the sales are coming from new houses. So again, why is this important? New houses = new infrastructure and all that comes with it (new schools, new retail centers, etc.), which means more construction in the areas that will likely interest my readers. Hopefully this trend continues. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed