|

Despite my love of my favorite economic indicator, the AIA's Architectural Billings Index (ABI), I'm a bit late blogging about it (I blame the World Cup--I've been distracted). What matters is that the figures for May are up sharply to 52.5 from 49.6 in April. The details are below (any value greater than 50 means that architecture billings are increasing; conversely, any value less than 50 means billings are decreasing):

Regional (three month) Averages for May 2014:

This is the West's second month of declines, which troubles me. The West has been hot for a while, so we'll see if the declines have legs. Everything is cyclical, and as I've said in the past, there are still regions in the West that are booming (SF/SJ Bay Area, etc.). Sector Averages for May 2014:

The Inquiry Index is at 63.2 for May, up from 59.1 in April and 57.9 in March. This is correlated to more good news going forward. Hopefully these ABI figures, along with other construction economic indicators, shows the industry is ready to break out.

0 Comments

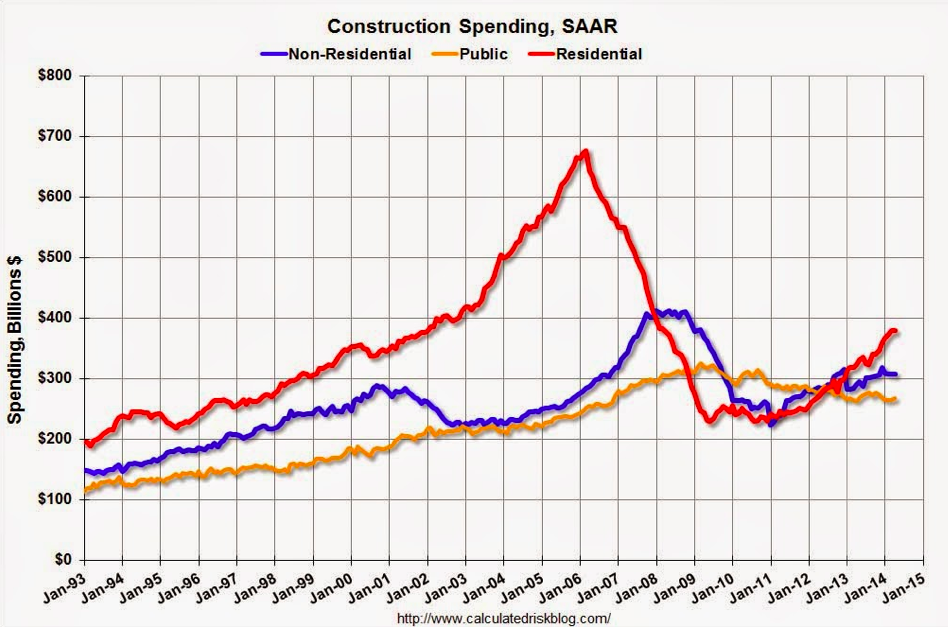

Residential and Public Sector Construction Spending is Up, Non-Residential Building is Down Again6/5/2014 The Department of Commerce's U.S. Census Bureau reported construction spending for April 2014 a few days ago. April's figure of seasonally-adjusted annual rate (SAAR) is $953.5 billion, up 0.2% from $951.6 billion in March. Modest improvement, but the details are more telling. The SAAR for private construction was essentially flat at $686.5 billion, down a hair from $686.8 billion in March. Public construction, which has been on a long downward slide, ticked up 0.8% to $267 billion in April, above March's figure of $264.8 billion. I will come back to public-sector spending in a separate post in the next day or two because it's an interesting topic these days.

The increase in public sector construction spending is good for the construction industry. As Bill McBride from the Calculated Risk shows in the above figure, residential is also health. There are even more details to highlight, though.

Non-residential spending is down for the fifth month in a row, decreasing 1% in March after a 1.3% drop in February. Not necessarily a good sign. Fortunately, the residential market, combined with the public sector, picked up the slack. Residential was up 0.7% in March after being down 0.3% in February. The single-family housing starts were up 0.8% in March, but the bigger story is that the multi-family went bonkers and was up 3.2% in March after being up 2.8% in February. This makes sense to northern Californians as the multi-family market has been hot for some time, particularly in the Bay Area. A bit of a mixed bag, but so long as the overall spending is increasing, the construction industry as a whole will continue to strengthen. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed