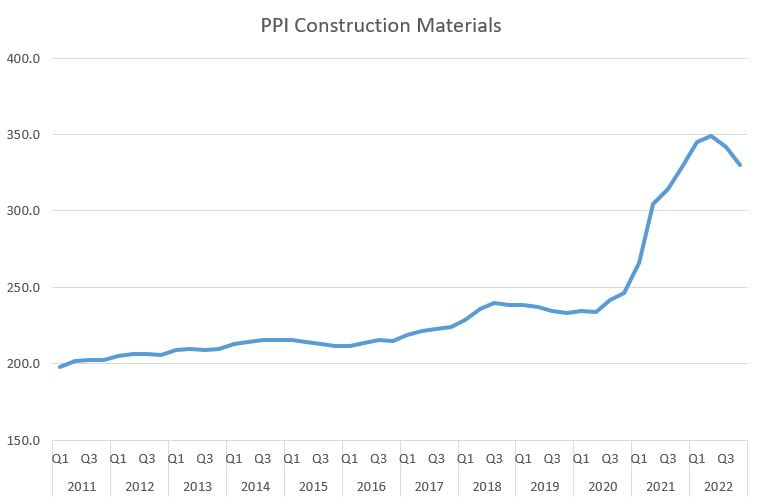

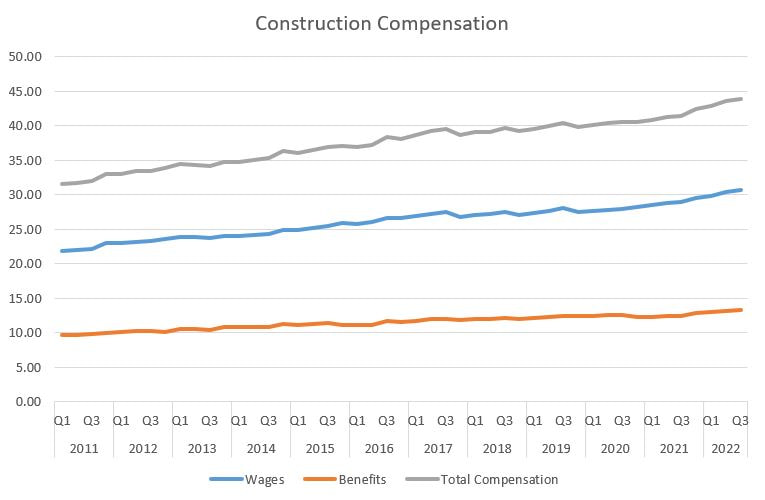

Construction Labor Costs are Rising, but Not Even Close to Increase in Material Price Increases3/29/2023 I read an article today stating that construction employment is up in 45 states last month. Given how busy the construction market is, and should in theory continue to be with government investments in infrastructure, this makes complete sense. Then I went down the rabbit hole: many of the projects we have put out to bid or proposal recently have been coming in at costs higher than expected. Is this due to increasing labor and/or material pricing? The short answer is both, but one in particular. The supply chain issues since the onset of the COVID-19 pandemic have been well articulated and continue to present times. The lack of labor, due to double whammy of fewer people entering the trades and a mass retirement of people on the tail end of their careers, is also a well know problem. So going further down the rabbit hole, which one is more acutely leading the the increasing cost of construction? It turns out materials pricing has the bigger lever.  While declining 5% since the first quarter of 2022, construction material prices, as measured by the Producer Price Index for Construction Materials, are up over 40% since starting a skyward upward trend in the second quarter of 2020. Keep in mind, the y-axis is relative, with 1982 being pegged at 100. Labor costs are also up recently, but the increase is much more subtle.  The y-axis on this chart is in dollars. Since 2011, total compensation has increased on an annualized rate of 0.7% per year. Since Q3 of 2021, the annualized growth rate doubled to 1.5%. This is a big jump, but the increase pales to the increases in construction materials.

For the time being, the extraordinary cost in construction can be blamed on material prices. If demand for construction stays at current levels and 1) supply chains get ironed out, and 2) we do not increase the number of people entering careers in the skilled trades, this dynamic could flip and labor costs will be the cause of accelerating construction costs.

0 Comments

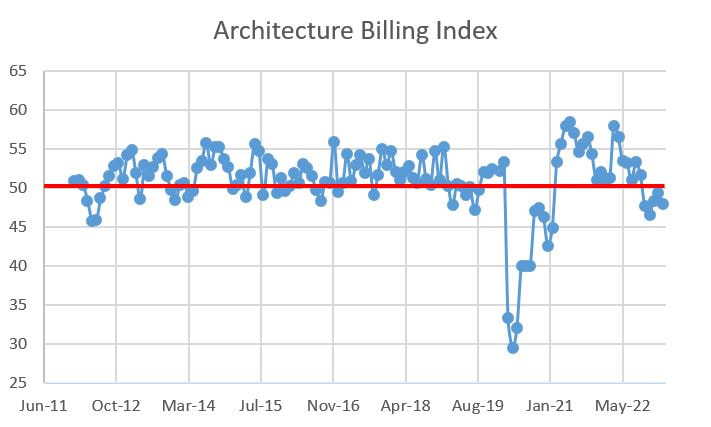

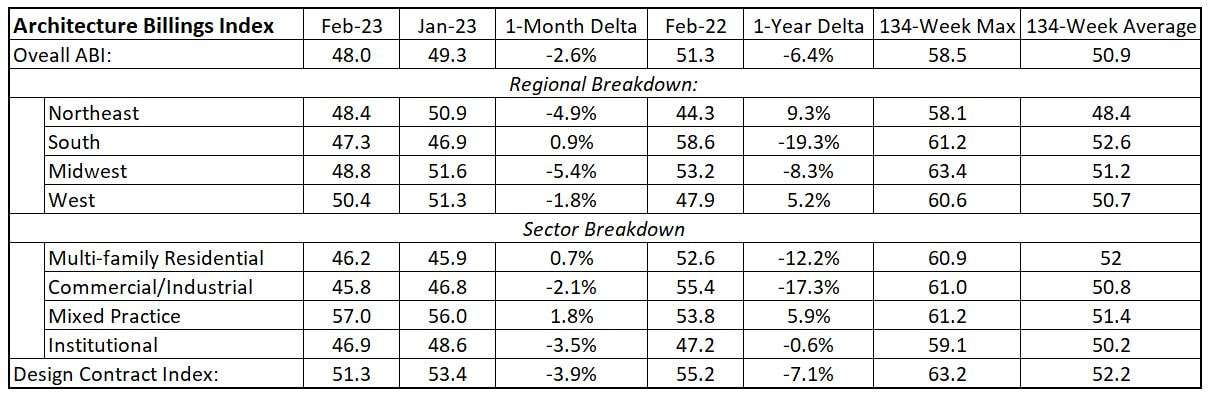

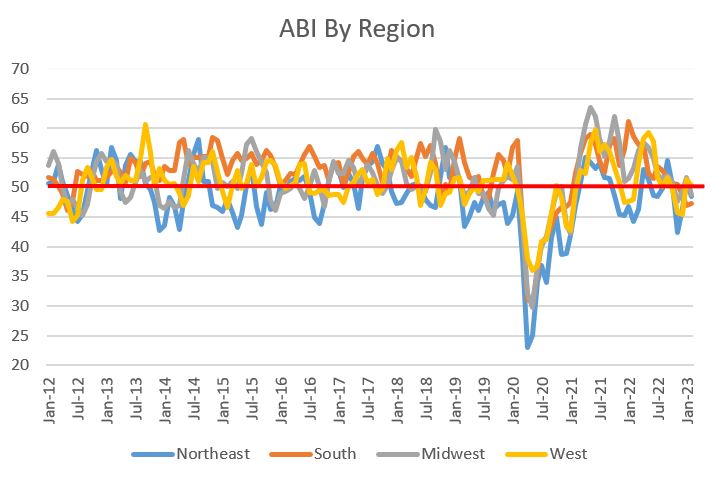

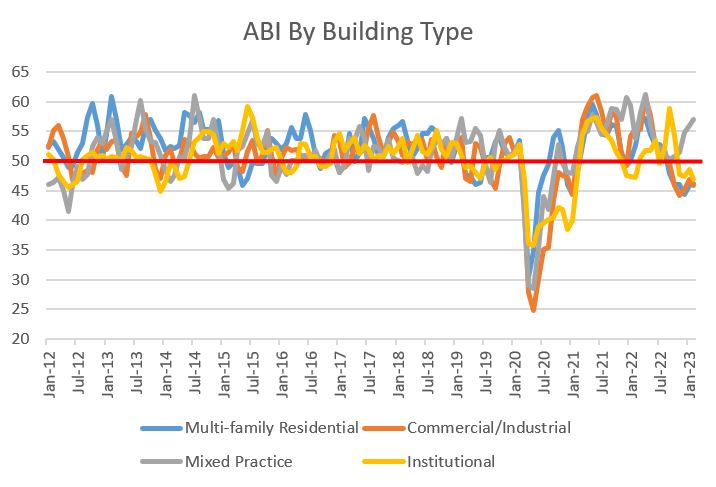

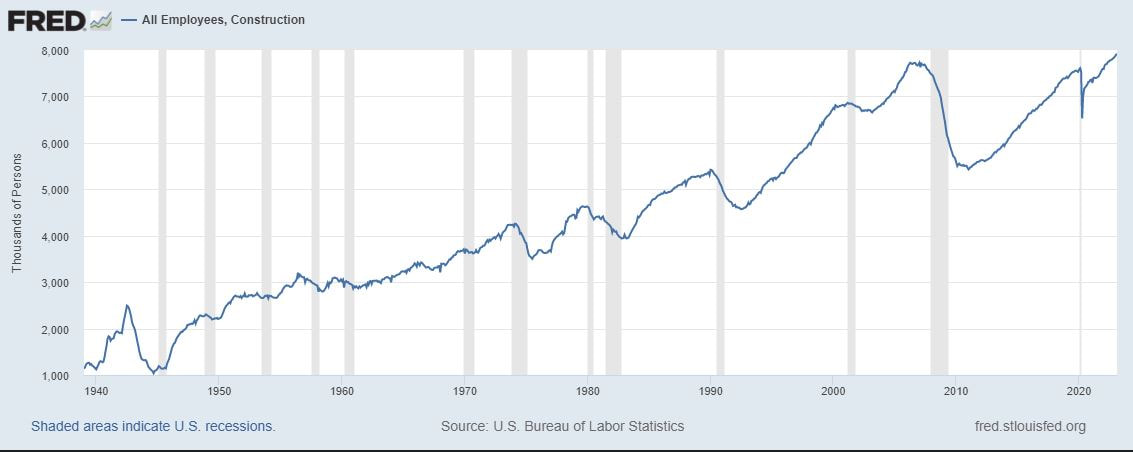

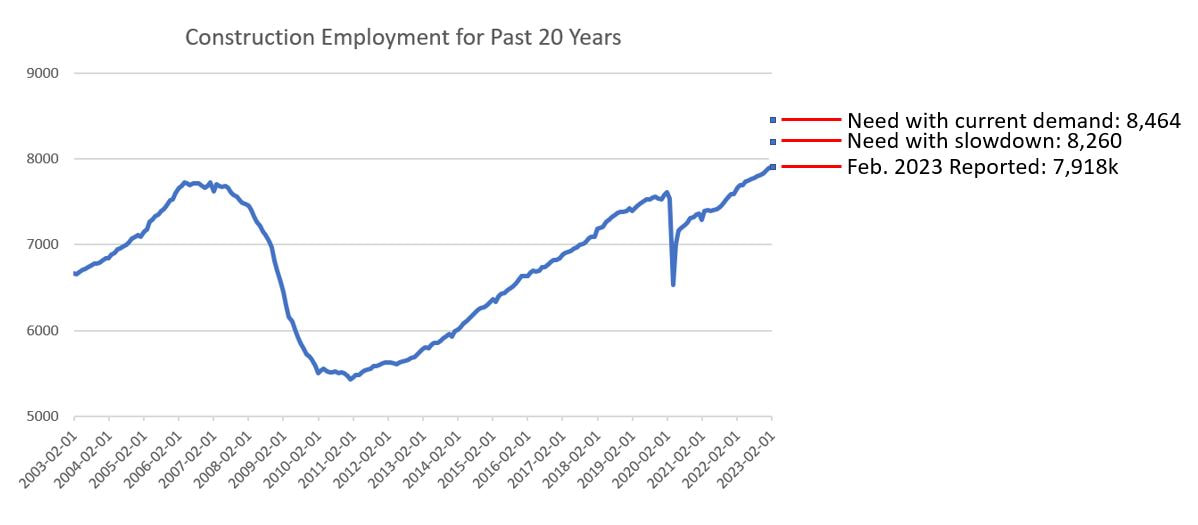

The slide in architectural billings continued this month with the American Institute of Architects (AIA) reporting an Architecture Billings Index (ABI) handle of 48 for February, down from 49.3 in January. This is the fifth straight month of sub 50 results indicating a secular decline. The ABI is a nine-to-twelve-month leading indicator of vertical construction activity, with ABI measures above 50 indicate that billings are increasing and those below 50 signal a decrease. After a few weeks of discussing potential bank failures, this result in ABI is an unwanted coda to a period of bad economic news.  There were some slivers of good news in the granular data breakout, but the trends are not great. Billings in the West are above 50, but they are down month-over-month. The South, once the behemoth in activity, continues its slide. The only true bright spot is Mixed Practice, clocking in at 57, up from a robust 56 the month prior. Design Contracts remain above 50, but are way off from a year ago. Only the Northeast, West and Mixed Practice are up over the past year.  The best spin to put on this is that construction activity remains strong (for now...) and the recession that has been discussed for three years has yet to truly materialize. Given stubbornly high construction material prices and increasing interest rates, it is not surprising that design activity has softened. The big question is how long before we pull out of the tailspin. Up or down next month is a coin flip given the headwinds the economy is facing. The detailed data breakouts are below.    There was a lot of news on the employment front. On Thursday March 9, the Associated Builders and Contractors (ABC) reported that the number of construction job openings was almost halved from December 2022 to January 2023 (a decrease from 488,000 to 248,000). This was a shocking development until a few days later when construction employment was reports by the Bureau of Labor Statistics as reaching 7,918,000, the highest level ever. The construction industry has been steadily increasing in employment since May 2021.  Current employment levels are well above the previous peak of 7.7 million in May 2007. This is amazing given the Fortune article published on March 10 (sorry, paywall protected) recounting an anecdote in the latest version of the Fed's Beige Book about a Montana-based contractor that flies its employees around in a private jet to fill operational need. As wild as that sounds, the article cited ABC data that shows we need to hire a lot more people even if the need for construction slows.  According to ABC, if the economy slows, an additional 342,000 construction workers will be needed, or 4.3% more than current levels. Should the need for construction stay at its current rate, an additional 546,000 workers will be needed, or 6.9% more than current levels. Given almost two years of employment gains, including adding 24,000 from the previous month, one might think that we will eventually add enough jobs, even it it takes a long time. But the Fortune article drops another statistical nugget that is terrifying for those trying to hire construction workers: a quarter of all construction workers are over the age of 55, revealing a demographic headwind that will make it incredibly difficult to to ever hire enough workers to meet foreseeable demand.

Increasing wages and a concerted effort to invest in infrastructure by local, state and the federal government, making construction jobs viable for the long term, might help attract people to the industry, but we will need more than that. Immigration reform and automation can also help, but both of those have policy implications. The future is bright for those in the industry, yet we have a lot to do to make the construction industry more appealing to a new generation of employees. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed