|

Today is a big day on the construction economics front. For a deep dive, go to Bill McBride's Calculated Risk blog. A few graphs on the site tell a good story:

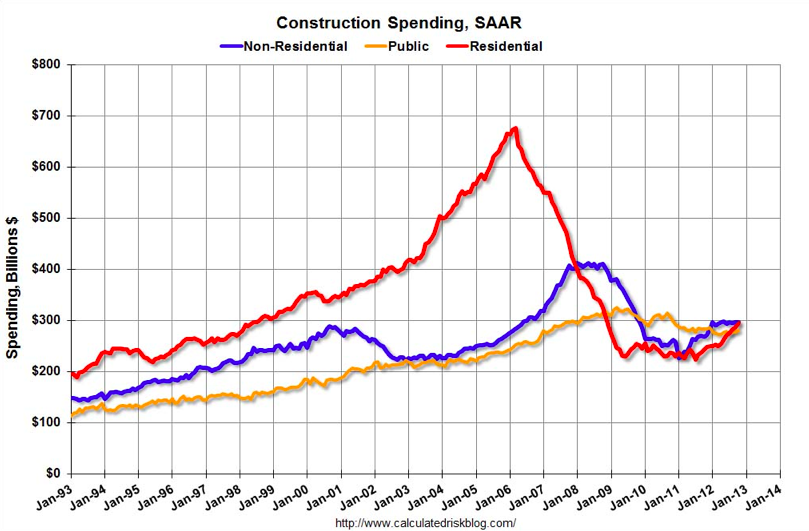

First, we (and by we I mean the construction industry) are still WAY off our past highs (as if anyone needs me to restate the obvious). But the trends have been getting better (much better if you go back to the lows). Most of the recent gains have been in the single-family housing construction market, a continuation of a trend that has been described by me in the past and by Bill McBride today. The commercial, industrial, and infrastructure markets are still a bit weak.

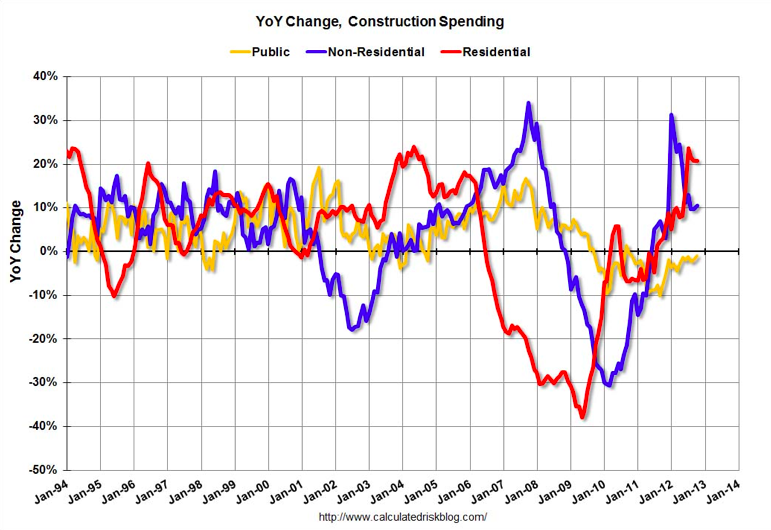

Looking at year-on-year data, the strength in the residential market is even more pronounced. However, there are signs of strengthening in the public market (projects sponsored by local, state, and federal government agencies). Baby steps for sure, but every little bit helps. The non-residential (read: commercial) market has seemingly fallen off a cliff after some really nice gains from 2010 to early 2012. As I have written in the recent past, this seems to be due to uncertainty in the business community. I'm sure all of this fiscal cliff stuff is not helping that...

The bottom line: spending on construction is growing and we're way off the industry lows of 2009 and 2010. Most of that growth is in single-family housing, which is the largest portion of the U.S. construction industry. This doesn't help the larger commercial contractors and their subcontractors I regularly talk to (the ones that hire my students and support my department!), but hopefully optimism in the housing sector will create some optimism in the rest of the industry.

0 Comments

Leave a Reply. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed