|

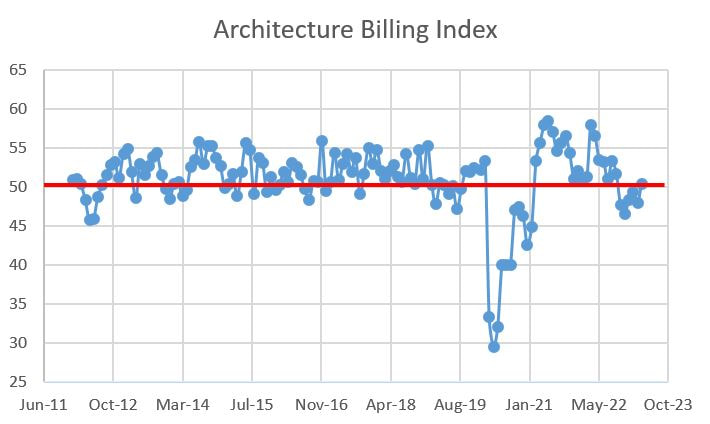

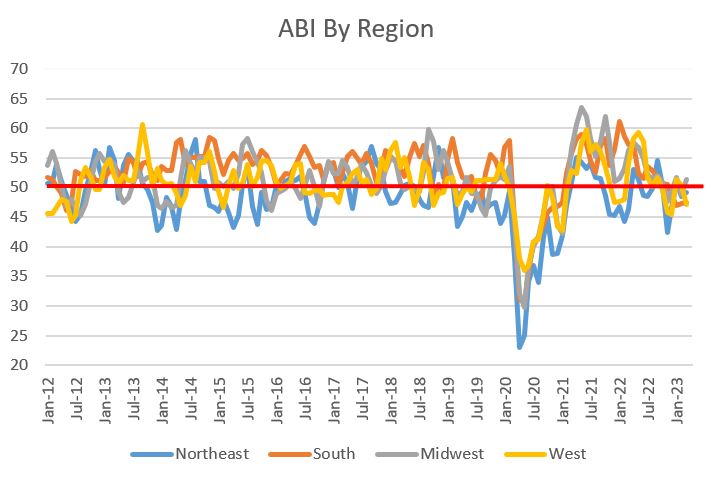

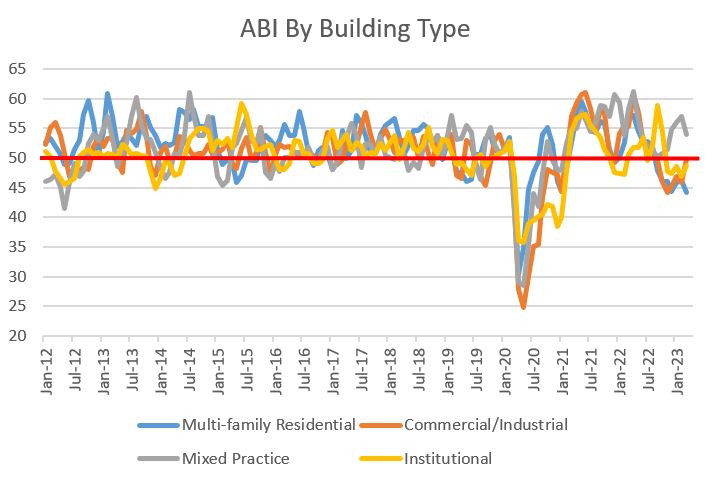

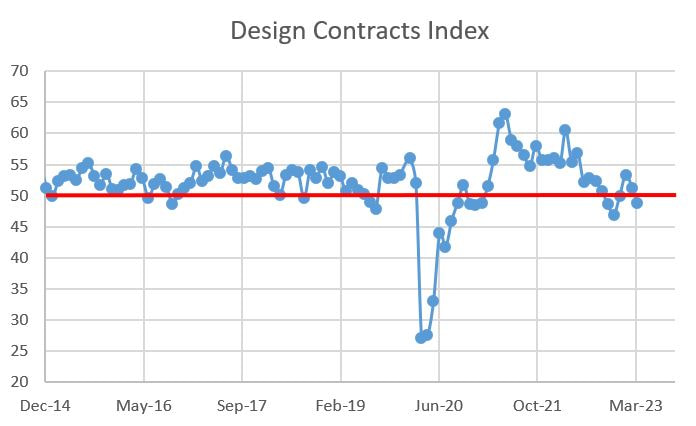

I read an interesting article last week that discusses how current market uncertainty has created a divide between winners and losers in the construction industry. That article was great foreshadowing for the March results of the Architecture Billings Index (ABI) as reported by the American Institute of Architects (AIA). The good news is that overall billings increased month-over-month, clocking a 50.4 handle in March, up from 48 in February. The bad news was widespread declining billings in the sub categories. Adding insult to injury, the numbers are way down on a year-over-year basis. A quick reminder that the ABI is a nine-to-twelve-month leading indicator of building construction activity, with ABI measures above 50 indicating that billings are increasing and those below 50 signaling a decreasing billings. The overall billings tend is displayed below, with March's figure peeking just above the 50 line:  A dive into the details shows the extent of the carnage. While there were month-over-month improvements in the ABI in all geographic regions save the West and there were big sectoral gains in Commercial/Industrial and Institutional projects, only the Midwest and Mixed Practice have an increasing rate of design billings; all other sectors are decreasing. So the positive overall ABI of 50.4 is being propped up by projects in the Midwest and Mixed Practice projects. Everything else is a drag. If we zoom out and look at ABI performance over the past year, we see darker clouds. The overall ABI, as well as many sub-ABI measures, are down by double digit percentages. Multi-family, once the darling of the AEC industry and the sector that managed the COVID pandemic the best, is falling like a stone with a drop of almost 23%. It's not time to panic. With the construction market starved for labor and still finding it difficult to procure materials, having some sectors cool while others heat up will keep many contractors busy for a while. Furthermore, many of the sub ABI figures are flirting with the 50 level, meaning a few good months of future performance could turn the tide. Chances are we will just have to become comfortable with this "on the one hand, on the other hand" type of fluctuating good/bad news cycles. A lot of people watching the banking industry are wondering if lenders with a lot of commercial real estate loans on their books are the next shoes to drop in the Silicon Valley Bank/First Republic Bank failure melodrama. If weakness is revealed, I suspect the breaks will lock up on the design and construction industry. Let's hope not. Detailed regional, sectoral and contracts information is as follows:

0 Comments

Leave a Reply. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed