|

While still below the frothy levels of 2005 and 2006 (which is a good thing), the housing market seems to be making somewhat of a comeback. This sentiment is not based solely on today’s homerun report that there were 894k housing starts this month (above the forecast of 840k and more than the 872k last month). There’s actually several months of positive trends.

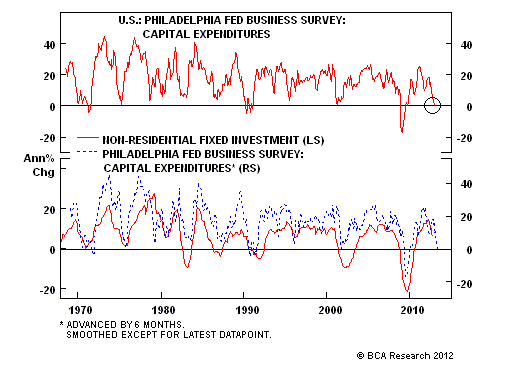

The housing market is not without its issues. Many people have been reducing their levels of household debt (deleveraging), although this great article by Joe Weisenthal presents the idea that a balance sheet recovery may be leading people to borrow money for housing. But for even those that want to buy, capital is still tight. Just because rates are low doesn’t mean that mortgages are easy to get. But with shrinking inventory and housing starts increasing, the news seems to be positive for homebuilders and, by extension, construction related to homebuilding. But what about private industry? Well, that’s a different story. Companies investing less in capital expenditures. Similar to families, companies are trying to reduce their debt levels and are decreasing the rate of investment in new facilities (or “non-residential fixed investments” in the figure below).

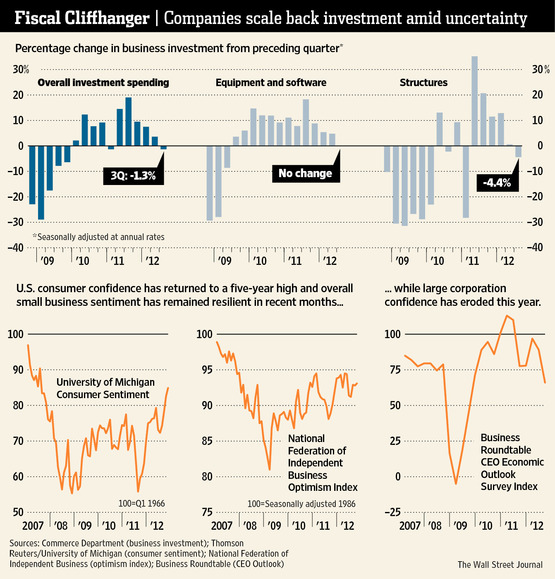

The better figure is the one below. It echoes the sentiment that companies are bearish on building structures, as investments are down 4.4% (see upper right graph in the figure below). A big reason for this pessimism: there is a general lack of confidence which may be the product of policy fear, market fear, regulatory fear, etc. Confidence is much higher than it was in 2009, but it’s trending downward in 2012 (see lower right graph in the figure below).

The bottom line is that homebuilding looks good, particularly in a market segment looking for good news, but commercial and industrial builders should still be cautious, as their corporate clients seem to be holding back on capital investments in structures.

0 Comments

Leave a Reply. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed