|

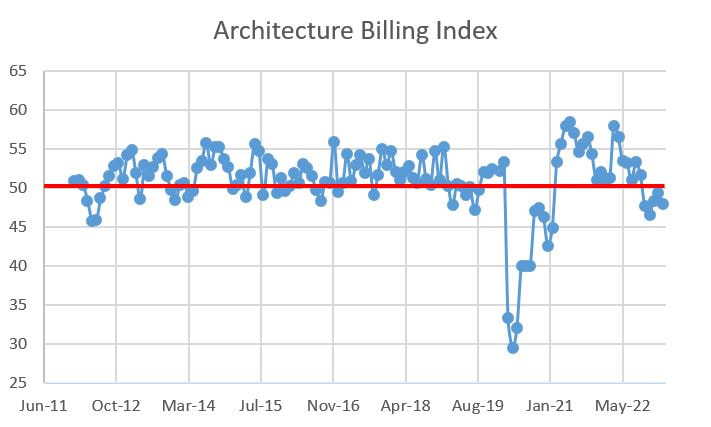

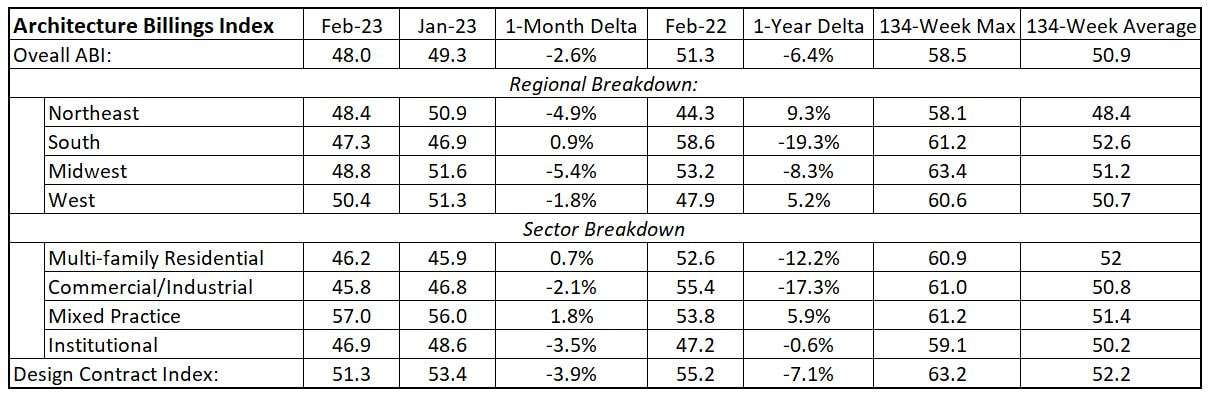

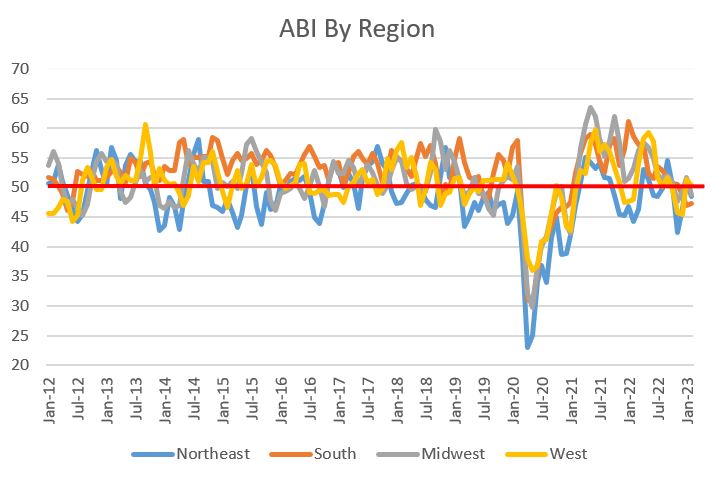

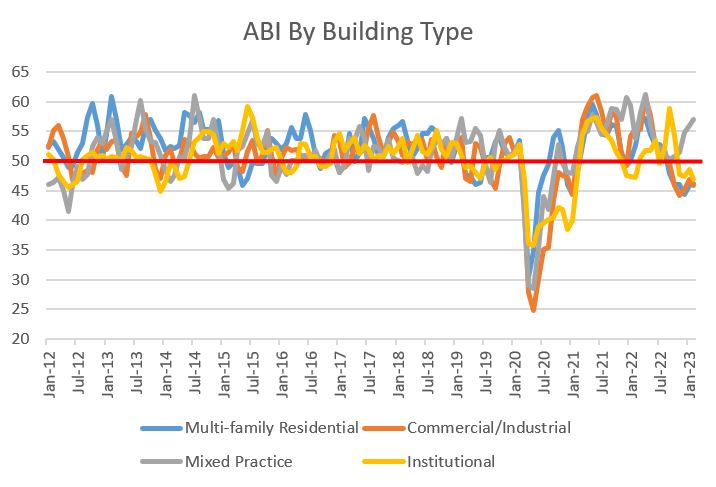

The slide in architectural billings continued this month with the American Institute of Architects (AIA) reporting an Architecture Billings Index (ABI) handle of 48 for February, down from 49.3 in January. This is the fifth straight month of sub 50 results indicating a secular decline. The ABI is a nine-to-twelve-month leading indicator of vertical construction activity, with ABI measures above 50 indicate that billings are increasing and those below 50 signal a decrease. After a few weeks of discussing potential bank failures, this result in ABI is an unwanted coda to a period of bad economic news.  There were some slivers of good news in the granular data breakout, but the trends are not great. Billings in the West are above 50, but they are down month-over-month. The South, once the behemoth in activity, continues its slide. The only true bright spot is Mixed Practice, clocking in at 57, up from a robust 56 the month prior. Design Contracts remain above 50, but are way off from a year ago. Only the Northeast, West and Mixed Practice are up over the past year.  The best spin to put on this is that construction activity remains strong (for now...) and the recession that has been discussed for three years has yet to truly materialize. Given stubbornly high construction material prices and increasing interest rates, it is not surprising that design activity has softened. The big question is how long before we pull out of the tailspin. Up or down next month is a coin flip given the headwinds the economy is facing. The detailed data breakouts are below.

0 Comments

Leave a Reply. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed