|

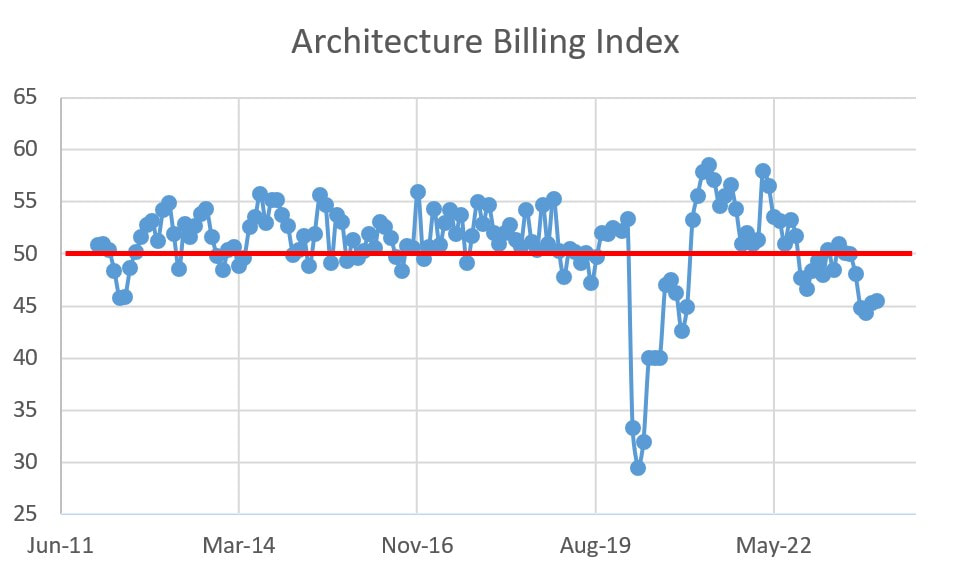

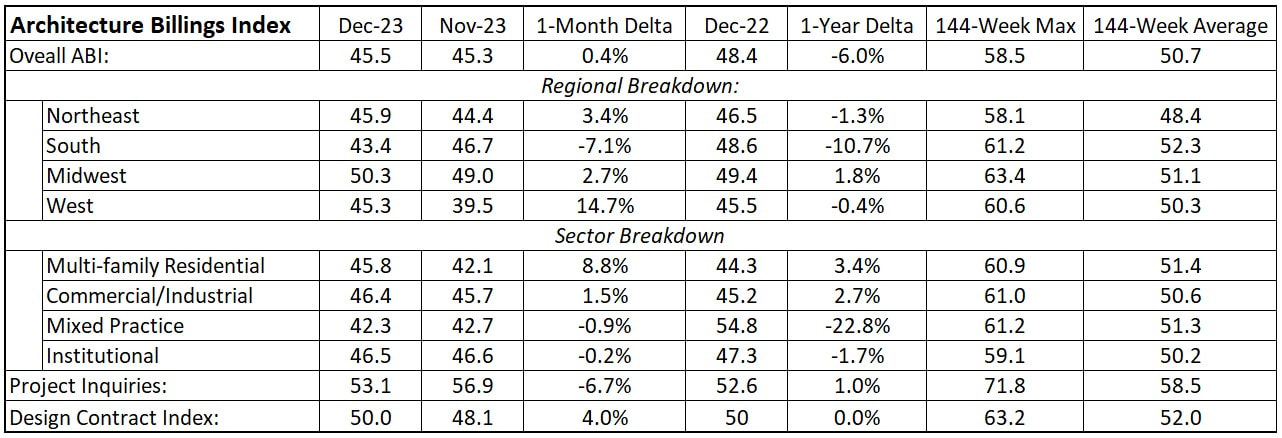

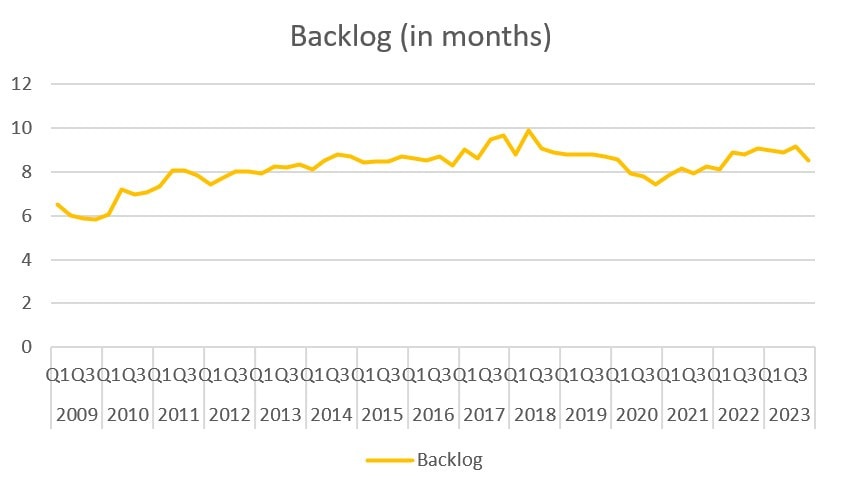

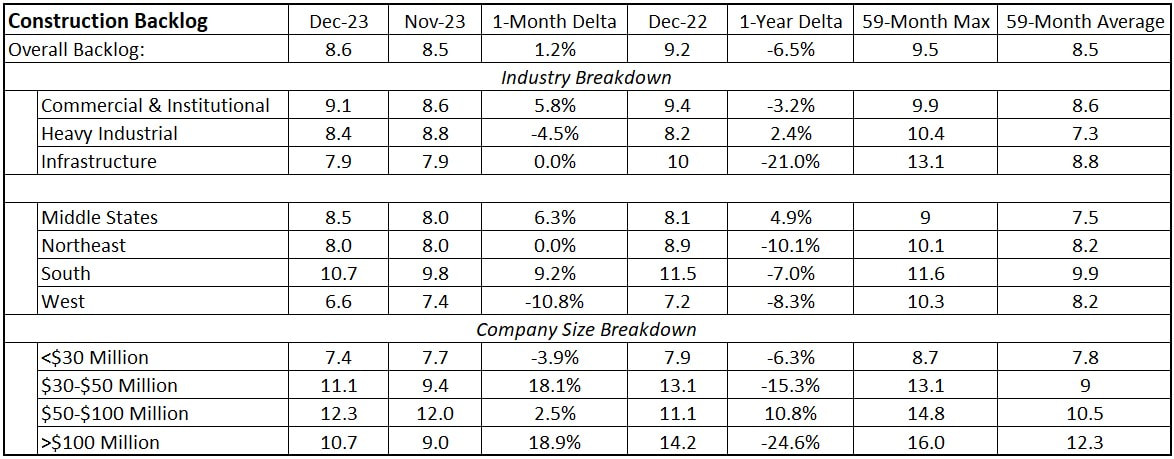

It has been a few months since I reported on architecture billings or contractor backlogs, and I kind of wish I remained in hibernation. While 2023 started off well enough, design activity turned sour around July. It is not all bad news, though. Contractor backlogs held steadier throughout the year, albeit with a dip in Q4. While this is predictable given the Fed Funds Rate increases, which were fully intended to pump the breaks on an overheated AEC industry, I didn't expect the design slowdown to happen so quickly or sharply. Using the data published by the American Institute of Architects in the form of the Architectural Billings Index (ABI), we can see how design activity has slipped in the second half of the year to levels not experienced since we crawled out of the COVID pit of doom. That is the bad news. The good news is that the last two readings have signaled a slight rebound. Again, this slowdown may be the industry coming to terms with the Fed Rate, which I have discussed recently. It is important to repeat that the ABI is a leading indicator of construction activity by nine to 12 months, so it foreshadows how busy contractors will be.  The data for the entire year is a bit manic. In spite of poor performance over the past six months, the month-over-month data is not too shabby. The South, long the darling of construction activity, was the only truly poor performer, and its cooling period was over the entire year. Aside from that, only Mixed Practice performed poorly year-over-year. Those two sub indices weighed heavily on the overall ABI, which declined 6% over 2023. All indices are below the 144-week averages and way below their highs.  The finer details are articulated below in the other sub indices. Institutional design is weathering the storm better than most sectors and that is not completely surprising given government investment in infrastructure. That leads us to contractor backlogs. Using the Construction Backlog Indicator (CBI) index published by the Associated Builders and Contractors, we can determine in the here-and-now of how busy contractors are. Backlogs measure how much work contractors have banked. In the case of the data presented below, it represents how many months a contractor would stay busy without securing any additional work. When backlogs are high, contractors are relatively busy and have pricing power. When backlogs slip, contractors have less work lined up and, thus, lose pricing power. Overall backlogs have slipped over the last quarter of 2023, however they are still above the 59 month average. Additionally, many of the sub indices are up month-over-month. The year-over-year story is a bit different, with the overall backlog index down 6.5% and some big sub index losses, including Infrastructure (-21%), the Northeast (-10%) and contractors with $30 to $50 million in revenues (-15%) and those with revenues grater than $100 million (-25%).   Based on the shape of the graphs (and giving grace to the differences in scales), it is clear that backlogs are less volatile that ABI. That said, in a perfect world, increasing ABI would be a catalyst for increasing backlogs, albeit with a nine to 12 month (give or take) lag. That said, given that the ABI started to struggle about six months ago, I would expect backlogs to continue their slipping over the first half of 2024. The light at the end of the tunnel is that the Fed is giving strong signals that it will decrease the Fed Rate in the second half of 2024. If the Fed handled the interest rate lever correctly, and there is strong evidence that it has shown great dexterity in cooling the economy without driving into the recession ditch, then the second half of 2024 may see increased design activity and the ABI rip north.

0 Comments

Leave a Reply. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed