|

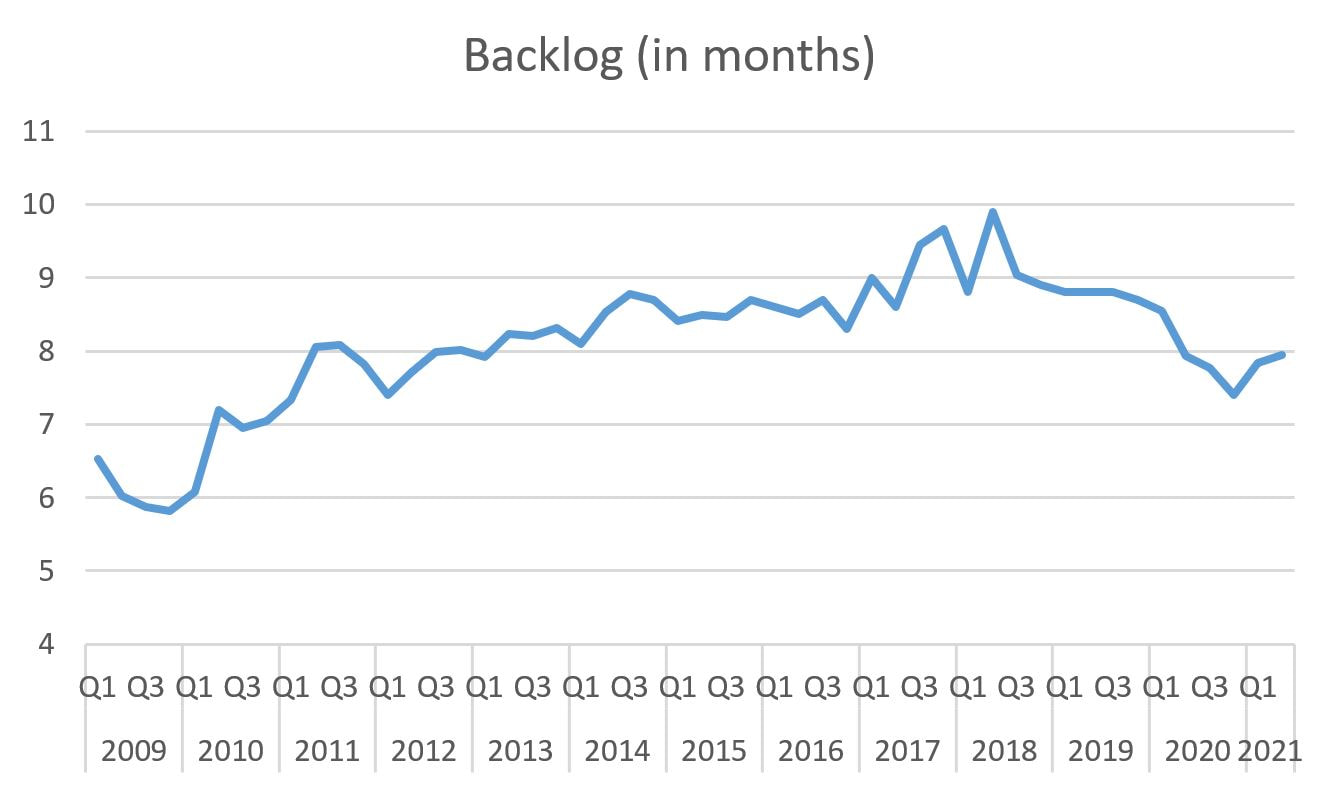

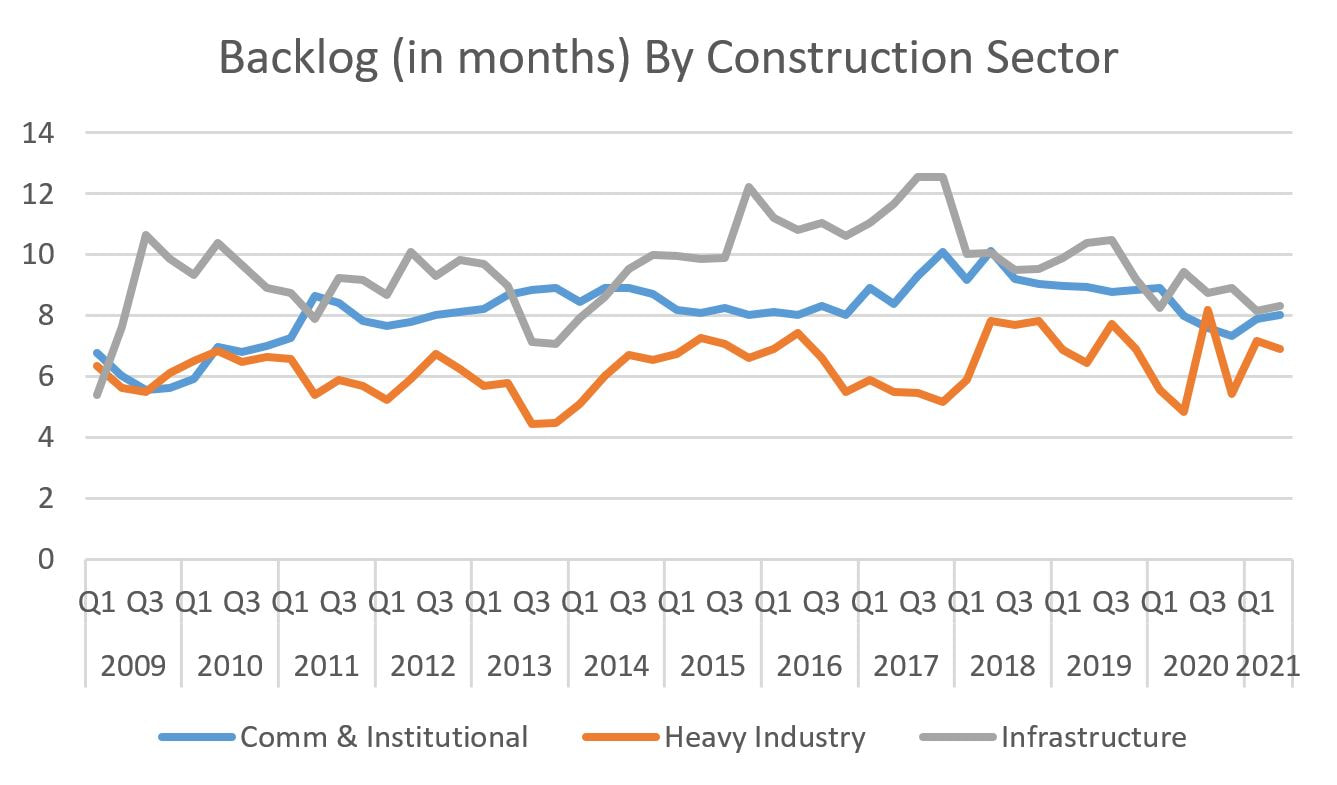

It has been a while since I've posted about contractor backlogs. I'm the guest speaker for an ASCE-ITE chapter in the southeast next week and we will be discussing (shocker) construction economics. Construction input costs are up (another shocker: it's predominantly due to material costs), but costs are also a function of contractor backlogs. When backlogs get deep, contractors raise fees, leading to higher project costs and when they slide, contractors decrease their fees in order to be more competitive. Simple supply and demand. So, how are backlogs? Luckily, our friends at the Associated Builders and Contractors (ABC) publish this data. Generally speaking, they have been increasing in the aggregate since November 2020 with a few dips along the way. The November 2020 backlog data point of 7.2 months was the lowest result since Q4 2010 (the data used to be released quarterly and now it is monthly. Please note that I have aggregated the monthly data into quarterly data in the graphs below. The aggregate backlog data is shown below:  So the general trend is positive, yet let look at the details, starting with the industry sector breakdown for May:

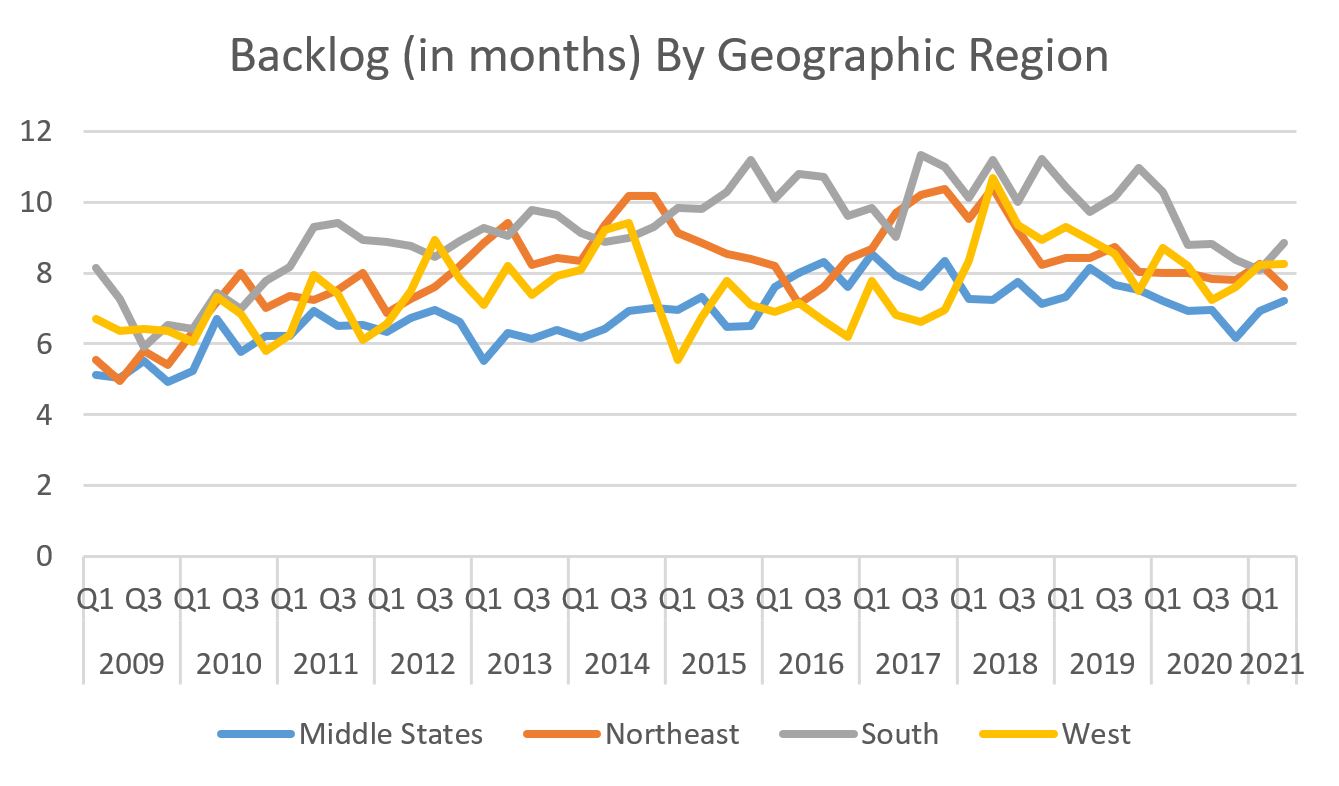

Moving on to geographic area, the results are more mixed:

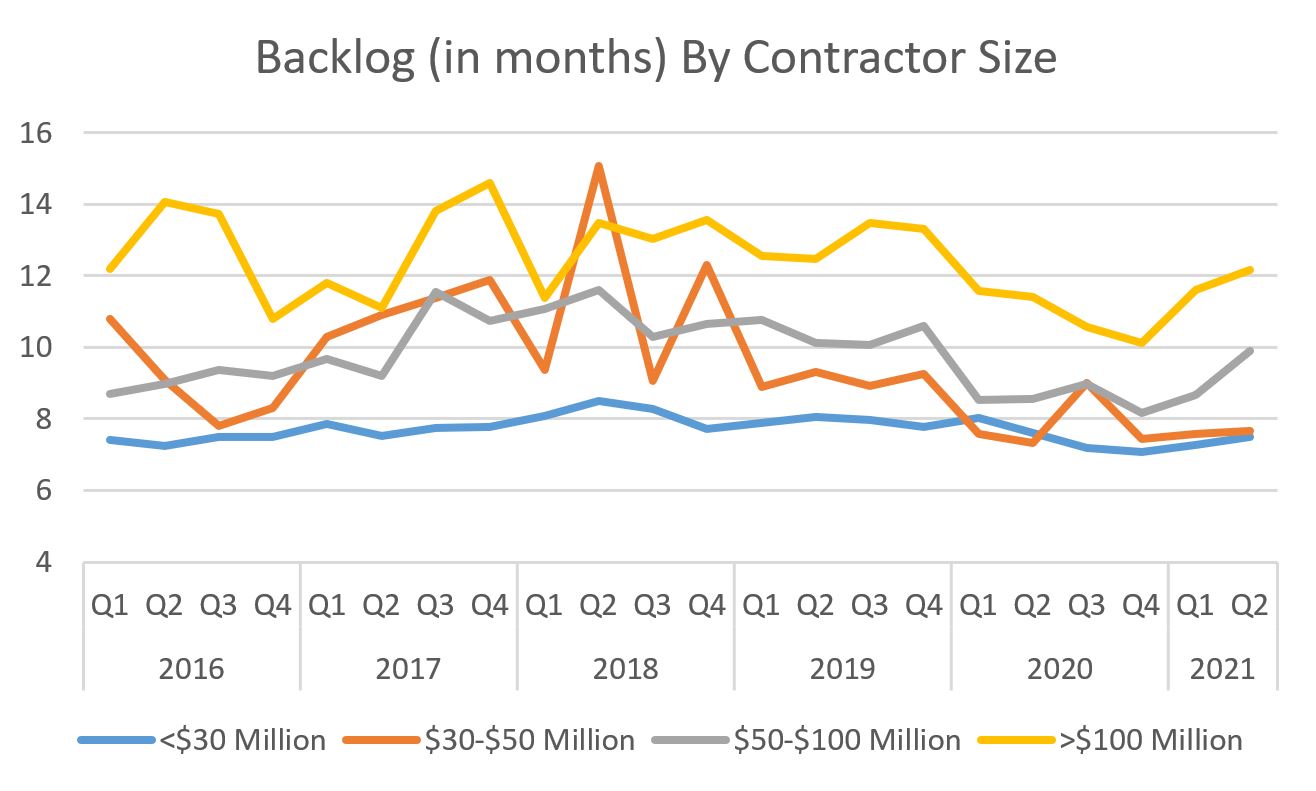

Lastly, the backlog data by contractor size:

So, mixed bag with the general trend moving upwards. This is far from a bold prediction, yet my gut tells me that increasing backlogs will be another tailwind (if you are a contractor and like higher fees) or a head wind (if you, like me, are on the owner's side of the contract).

0 Comments

Leave a Reply. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed