|

I thought I was done talking about real estate for 2012. But a wave of good news has been landing so I wanted to pass it along. Just to reiterate, my primary interest in the single family housing market is that it is an indicator of the health of the overall construction market and the economy in general. Very few of my students and industry friends are in the single family construction industry, but good health in that market generally points to good news in the market for other (bigger and more complicated) construction projects. I'll separate the news by date. See if you can detect the trend: December 20, 2012:

December 26, 2012

December 27, 2012

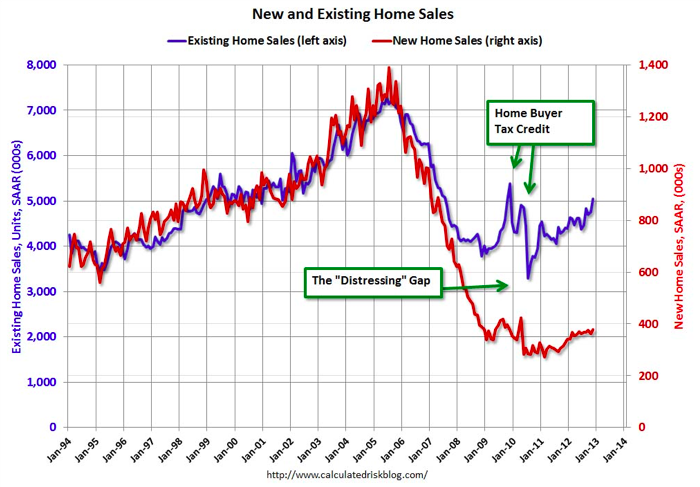

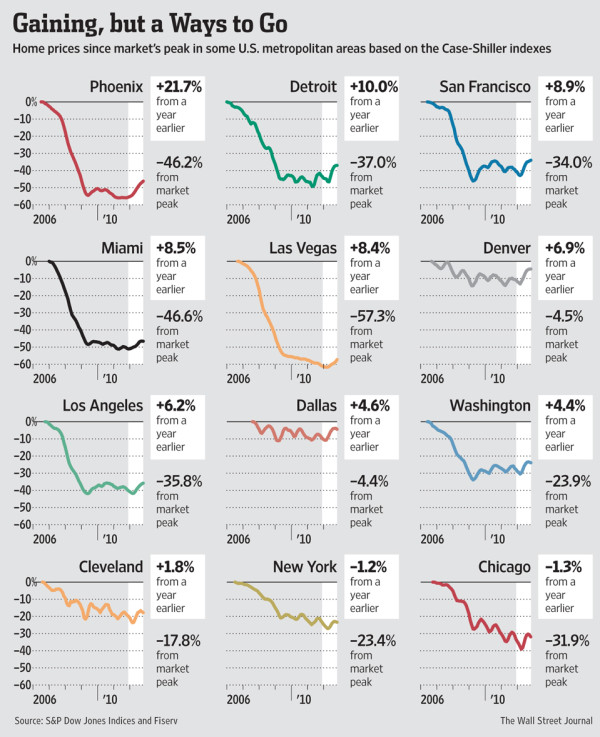

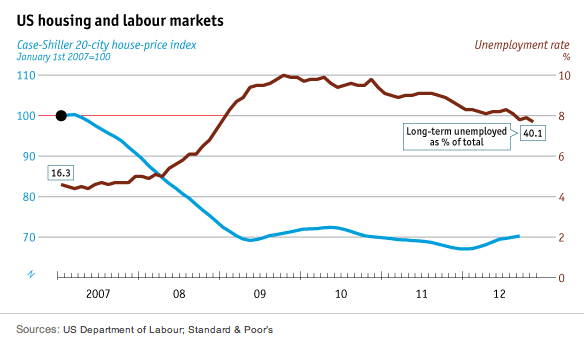

Existing home sales outpaced new home sales during the recession because many of the existing home sales were of distressed homes at bargain basement prices. New homes could not compete with the lower priced existing homes, so sales of new homes fell. As the number of distressed properties decreases, new home sales should increase, closing the "Distressing " Gap. This is good news for general contractors, because as new homes are built, so are adjunct buildings (schools, firehouses, retail, etc.). Other Miscellaneous Data:   Looking at the two figures above, the Case-Shiller price index is getting better in most places in the U.S., particularly the places that were hit hardest during the downturn (Phoenix, Las Vegas, Miami, I'm looking at you). However, we are still a long way from the pre-recession peaks. The second figure I threw in this post because I found it interesting. It seems, at least from 2007 on, that the Case-Shiller index and unemployment are inversely proportional. So, if unemployment decreases, hopefully Case-Shiller will increase (sort of a master-of-the-obvious observation). OK, so what does all the data above show? It seems to indicate that the housing market is getting better. This would traditionally indicate that the economy is getting better and that construction activity should be increasing (institutional and commercial construction tend to lag housing). This should be good news for general contractors. Except... What's the bad news? Sorry, but we're not completely in the clear. In fact, there is a considerable amount of uncertainty in the market. It stems partly from:

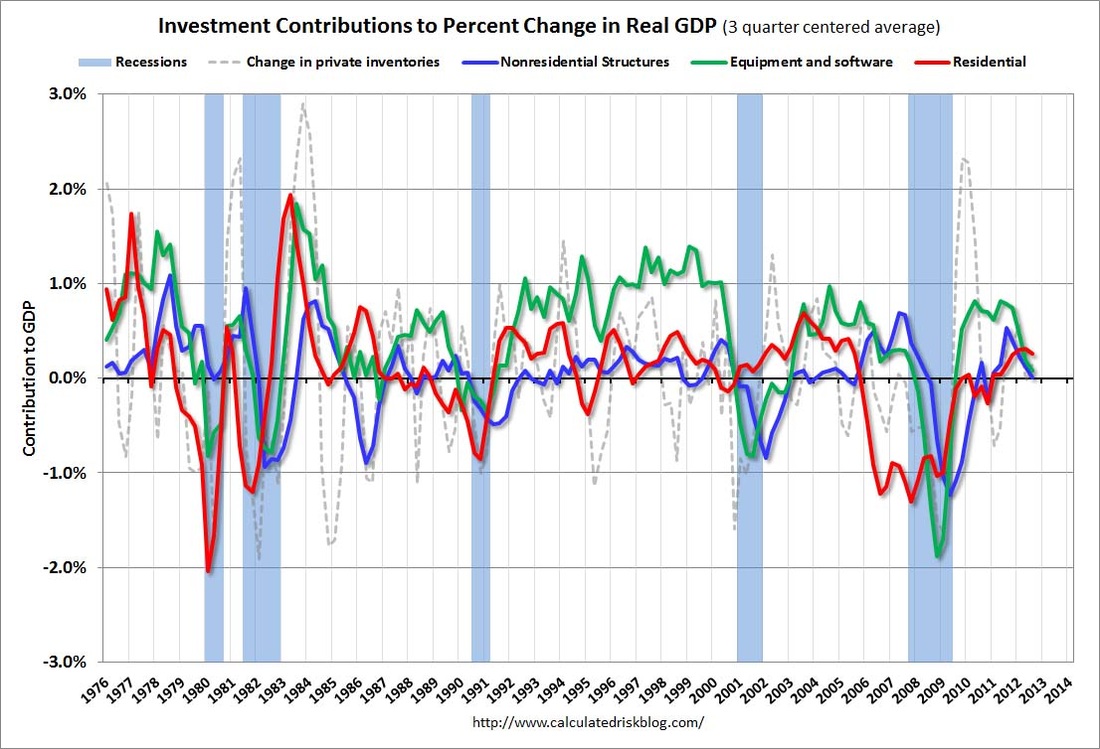

So the housing market looks like it's improving and the data supports that it is. But lurking in the background is a fragile economy (and we haven't even mentioned the fiscal cliff or any other external factors that could upset the market). If this housing market improvement has legs, then that's good news for the construction industry (and the economy as a whole). If it doesn't, well, we're stuck in the same slow construction market we're currently slogging through. I guess like many things in life, we'll just have to wait and see. But wait there's more! I want to leave you with one last figure, again courtesy of Bill McBride:  The above figure shows the contribution to GDP from residential investment (which includes home building), equipment & software, nonresidential structures (what general contractors should be interested in), and "change in private inventories." These are the four categories of private investment. As discussed above (and in other posts), residential real estate tends to be a leading indicator of the economy and nonresidential structure investment is a lagging indicator (equipment and software is neutral). But this didn't happen in this recovery--housing has lagged. This was due to the inventory that grew so large during the recession (but has been slowly been whittling down). Perhaps this recent (2012) strengthening in the housing market is the indicator that the economy is getting stronger, all other signs weakness notwithstanding. If so, then expect the blue line in the figure above to reverse course, a trend that would be positive for general contractors. For Bill's full post on this (which is a very worthy read), click here.

0 Comments

Leave a Reply. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed