|

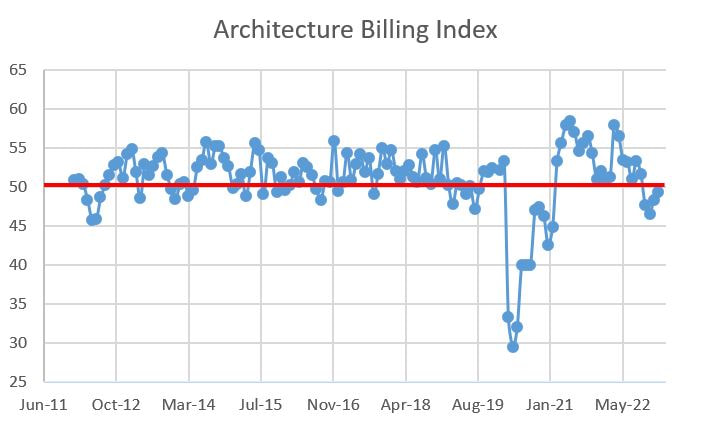

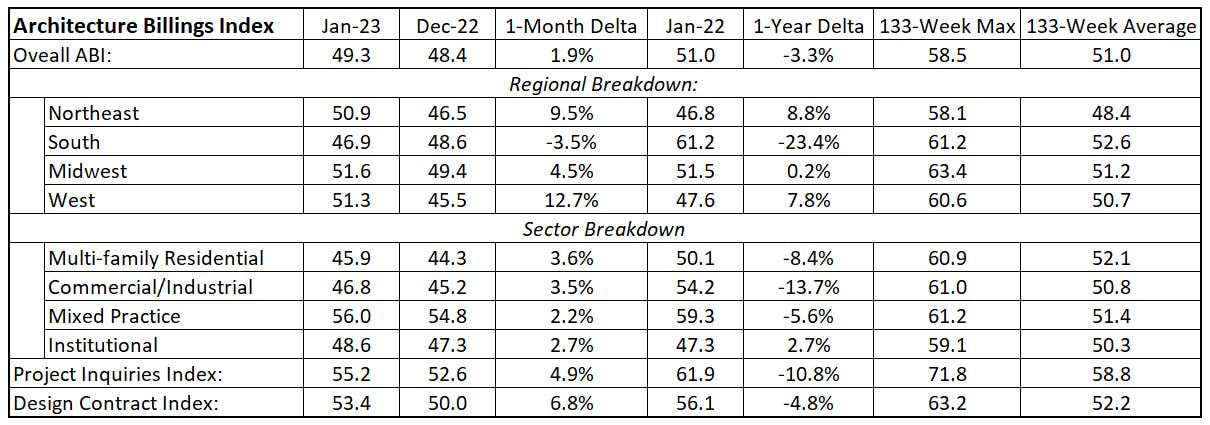

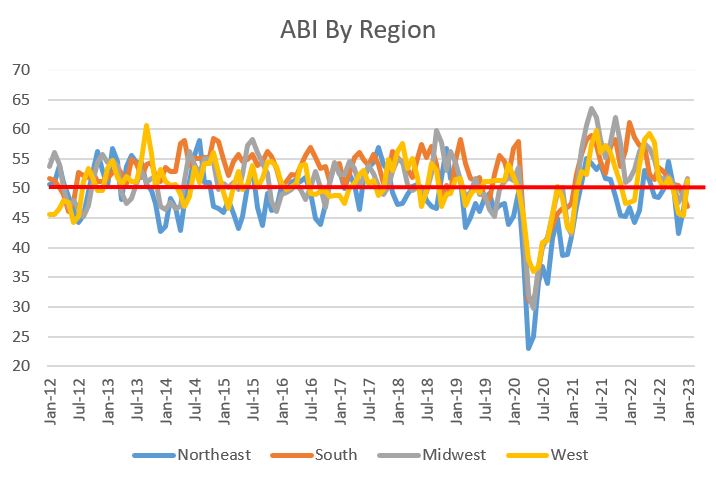

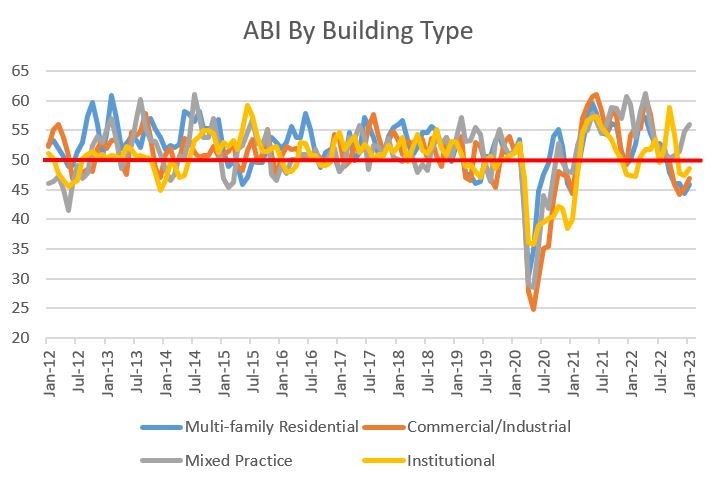

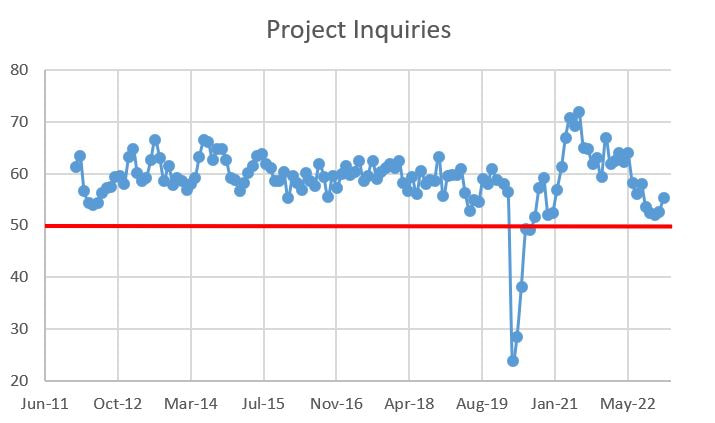

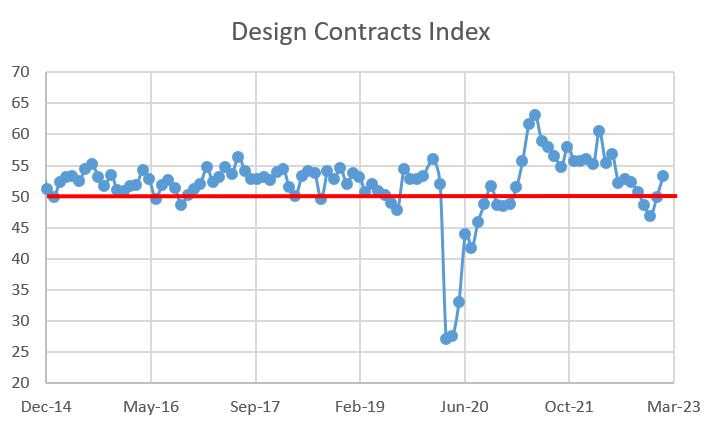

Let's get the bad news out of the way: the American Institute of Architects (AIA) released the Architecture Billings Index (ABI) results for January and it landed at 49.3. ABI measures above 50 indicate that billings are increasing, while those below 50 signal a decrease, so 49.3 demonstrate a slight decrease in billings. The ABI is a nine-to-twelve-month leading indicator of commercial building construction activity, so this would indicate reduced vertical construction activity sometime between October and the end of 2023.  All that being said, the granular data paints a better picture. Three out of four regional ABI figures were above 50, as was one of four building sector ABI measures. Seven of eight regional and building sector measures increased from the previous month, and both Project Inquiries and Design Contracts measures continued to be north of 50 and increased month-over-month. So yes, the overall ABI is still less than 50, as is half of the sub-ABI data points, but things are getting better with the promise of additional increases next month (fingers crossed).  The year-over-year data reveals some interesting insights. The overall ABI is down 3.3% (49.3 for January 2023 versus 51 for January a year ago), but those losses are goosed by dismal YoY results for the South (down 23.4%) and commercial/industrial projects (down 13.7%), with multi-family (down 8.4%) and mixed practice (down 5.6%) dog piling on the decline. The South has been on a heater since I started tracking this data and has the highest 133-month average, so that almost quarter decline is surprising. Similarly, multi-family and mixed practice have the highest 133-week sector averages but have had a very poor 12 months. Perhaps we are seeing a regression to the mean. My hypothesis for commercial/industrial is twofold: 1) the commercial office market is still a mess due to continued work-from-home practices, and 2) the industrial market, particularly warehouses and distribution projects, is coming down from the COVID e-commerce fever dream. The details are below:

0 Comments

Leave a Reply. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed