|

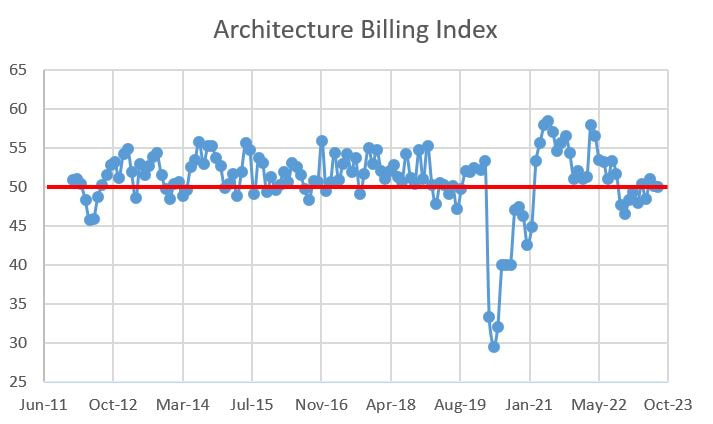

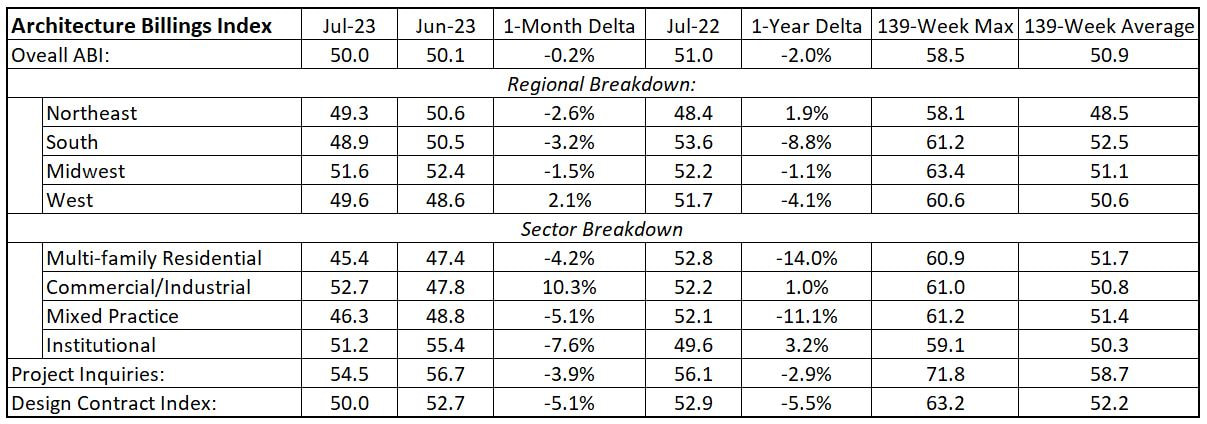

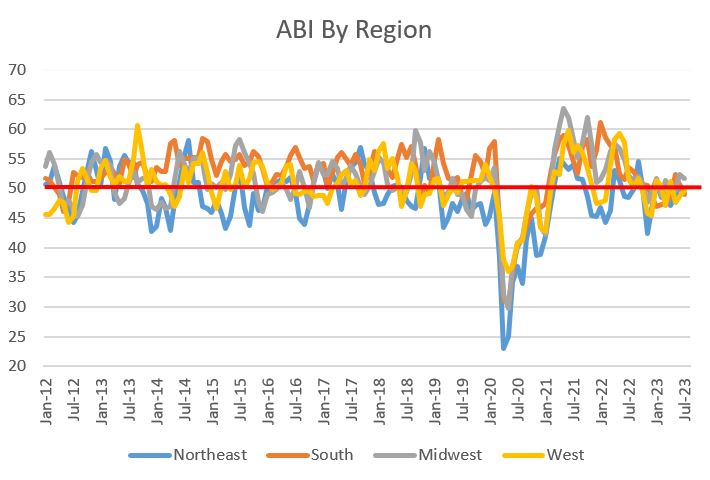

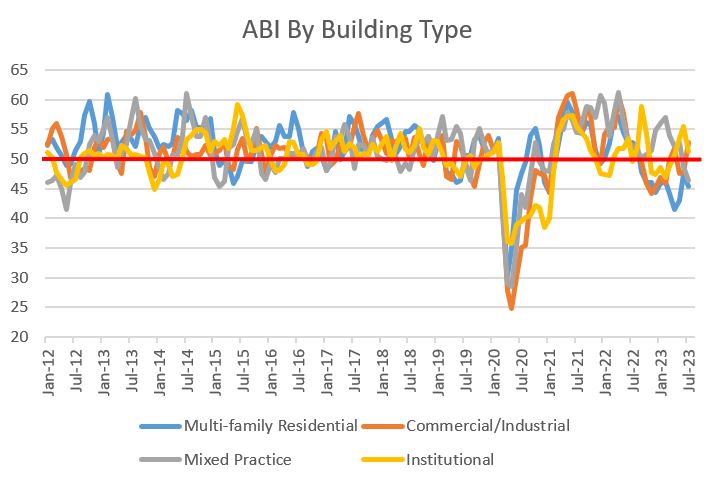

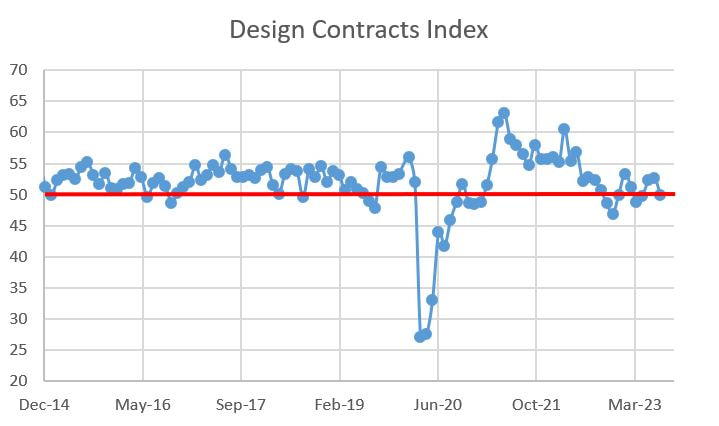

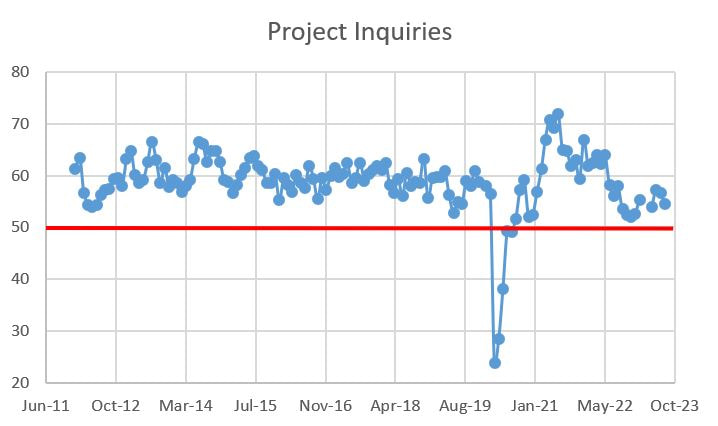

We are in strange times. The Federal Reserve Bank is increasing the effective fed rate in an effort to cool inflation, which is a response to a hot market. And yet demand persists. People keep spending money on houses (if they can find one), cars, COVID revenge travel, etc. Where is our pain threshold? How high do interests need to go before the market taps out? While one data point does not define a trend, the most recent report on Architectural Billings Index (ABI) published by the American Institute of Architects, delivered a 50 handle. The ABI is a nine-to-twelve-month leading indicator of building construction activity, with ABI measures above 50 indicating that billings are increasing and those below 50 signaling a decreasing billings. So July's reading is neither going up nor down. Is this the breaking point?  The details show a more mixed picture. The Midwest has increasing billings, while the other geographic areas are down. In terms of product, Commercial/Industrial and Institutional are up while Multi-family and Mixed Practice are cratering. Project inquiries, a measure of people planning projects for the future, is above solidly above 50, but it is way below the average for the past 11 years. Good news plus bad news equals break even.  The next few months will be very revealing. While the Fed indicated a week ago that they are done hiking rates for the near term, it is maintaining optionality to increase funds later this year. Which is Latin for they are waiting for more info before making a definitive call. Just like the rest of us. Until then, hold on tight. The details follow:

0 Comments

Leave a Reply. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed