|

The Associated General Contractors of America (AGC) was supposed to report on construction spending in August but can't due to the government shutdown (the Census Bureau is closed). This data point was going to be very interesting seeing as the AGC previously reported that construction employment increased in 194 of 339 metro areas year-over-year (August 2012 to August 2013) and that construction employment increased in 26 states from July to August. Both of these reports lean towards an ongoing improvement of the construction industry.

In its most recent press release, AGC states that the government shutdown may hamper the construction industry's long climb out of the hole created by the great recession. According to Stephen Sandherr, the AGC's CEO, "This shutdown poses a real risk of undermining the industry's long-awaited recovery."

0 Comments

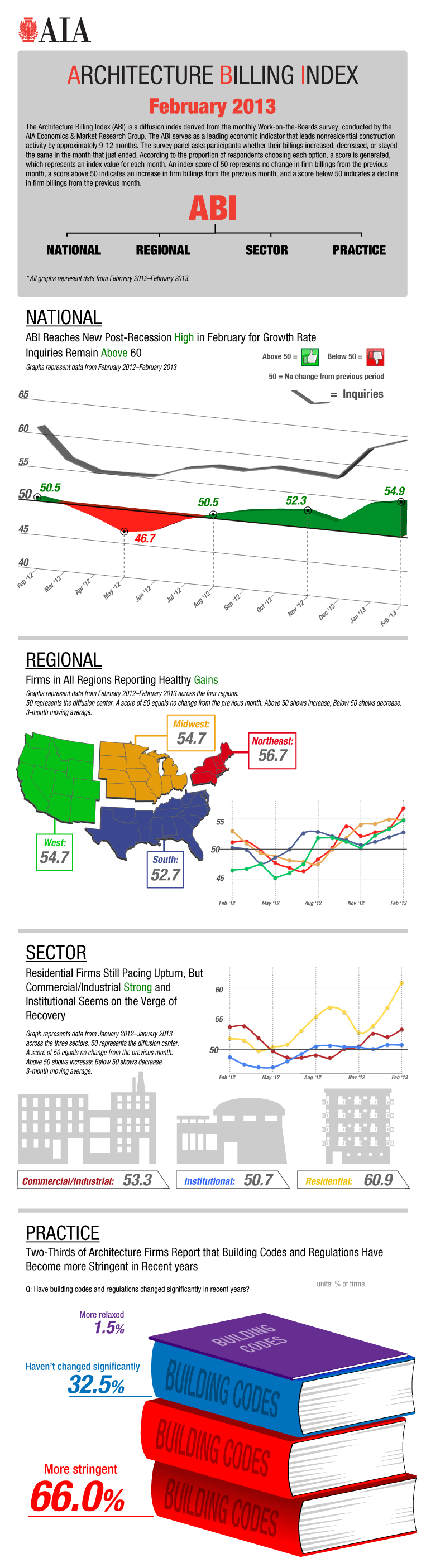

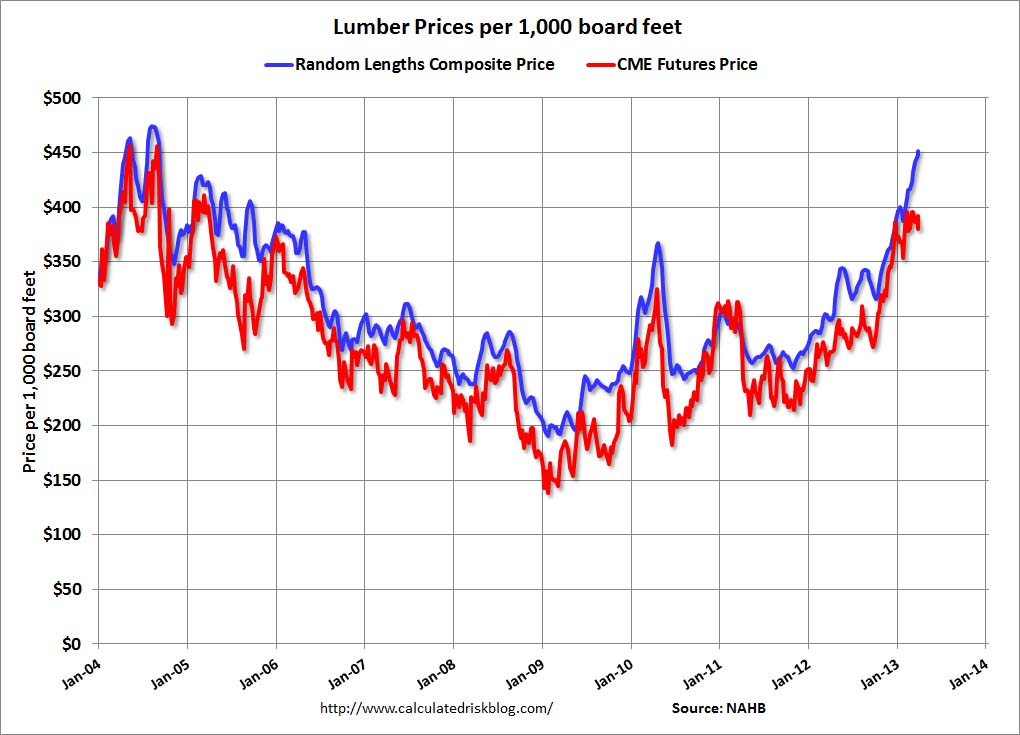

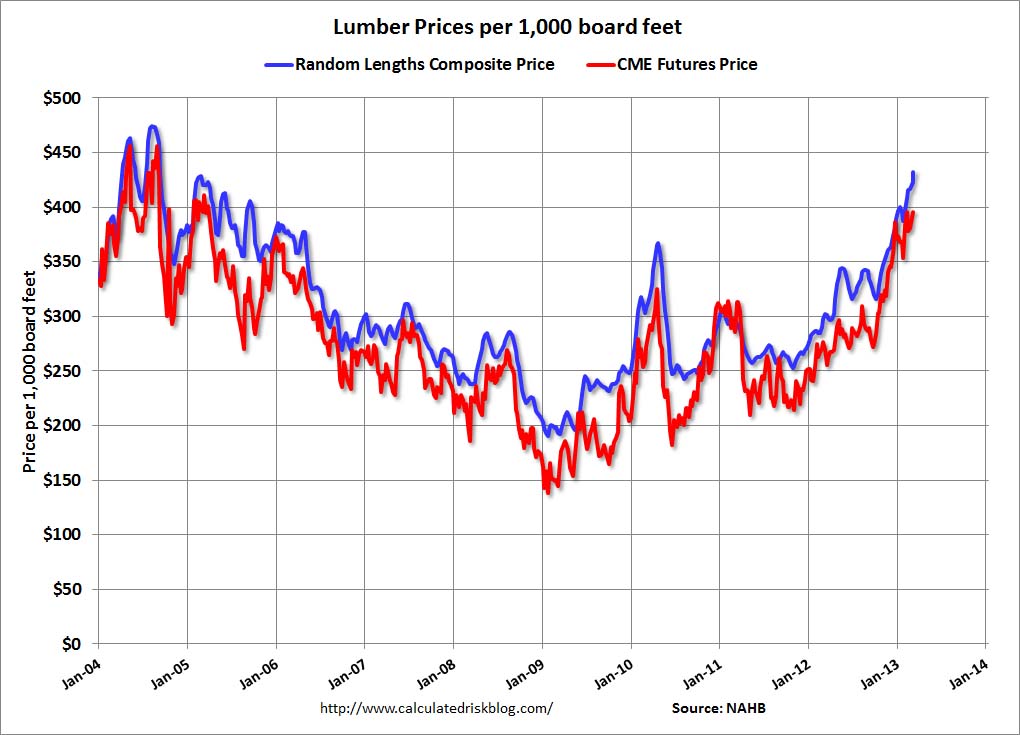

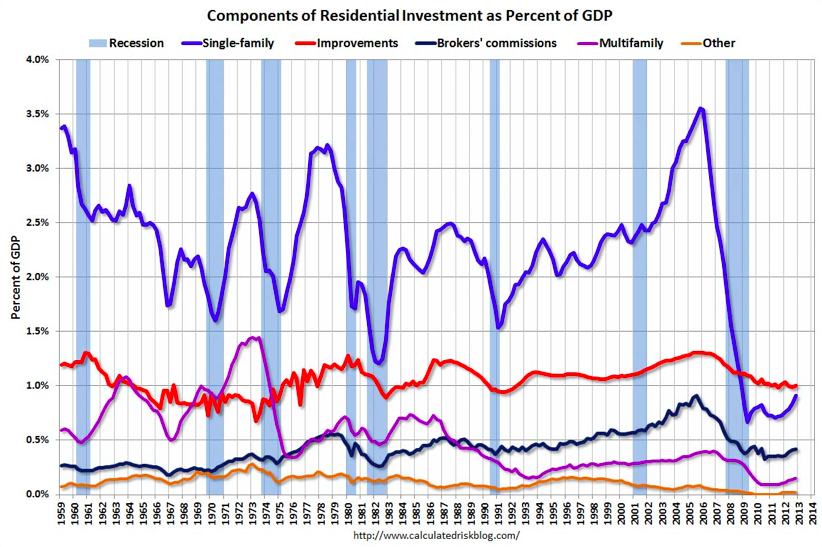

I've been a huge cheerleader for the recent growth in the construction industry. Part of this is because, as a college professor teaching in the Construction Management Department at California State University, Sacramento, I want the industry to do well because it means jobs for our students. And the job market, by all indicators, is improving. Anecdotally, students graduating from our department are getting job offers (with many good students getting multiple offers) and the salaries are bananas. Internships for continuing students are plentiful. There is data that shows that employment is gaining throughout the entire construction industry, primarily driven by the housing sector (I've written about the growth of the housing sector before, but here's a report published by the National Association of Home Builders with data). While single-family home builder data is nice, it's not really the market we prepare our students for. Most of our students work for large commercial general contractors, heavy-civil contractors (for infrastructure projects), or specialty subcontractors (electrical, mechanical, plumbing, etc.). Those markets also appear to be doing well, possibly riding the coattails of the housing boom (when you build houses, you also need to build ancillary projects like roads, schools, apartments, retail centers, etc.). As I promised a few weeks ago to post, the figure below shows the AIA Architectural Billing Indices for differing sectors of the construction industry and for differing regions of the country:  The ABI is above 50 for each region (above 50 means billings are increasing). Additionally, the ABI is above 50 for each construction sector, and it's above 60 for the residential sector (by residential, AIA means multifamily structures, such as apartments and condominiums). So, this is all good, right? Cracks in the Armor? I don't want to cry "the sky is falling!" However, there are some issues that we need to be cognizant of. First, home builder sentiment is falling. On April 15th, the NAHB reported that the Housing Market Index (HMI) fell from 44 in March to 42. Home builder confidence also slipped. This is not a huge deal as both HMI and confidence had been on a tear previous to the April figures release. And this is just one month "slide." Also reported on April 15, though, was a report stating that it is increasingly difficult to secure Acquisition Development and Construction (AD&C) loans for home building. Again, this is not directly related to the types of commercial and infrastructure projects that CM students are typically involved with, but they are a leading indicator of the projects they are involved with. If capital is difficult to get for home building projects, it will put a crimp in that sector of the economy that may very well spill over into other sectors of the construction sector. Just to show how manic the housing market is, the very next day, April 16th, it was reported that housing starts far exceeded expectations (7% increase). But that number is heavily weighed by multifamily construction (up 31%, which is good for CM students), but down 4.8% in single family housing (again, as a leading indicator, this is not so good). Also, the number of housing permits fell 3.9%. For an article summarizing all of this data, check out this summary created by the Business Insider. Things are a lot better than they were in the construction sector's dark days of the Great Recession, but some of the gains are slipping. So housing starts go up and down, as does home builder sentiment. Home builder stocks are on a tear (possibly getting bubbly), but they also correct from time-to-time. Those are indicators, but there is a lot of noise with them, particularly when applying them to larger commercial construction projects. The data that really has me thinking (and a little concerned) is the price of commodities tied to construction, particularly lumber. Check out this graph provided by the always on-the-front-edge-of-data Bill McBride at the Calculated Risk blog:

By itself, climbing lumber prices aren't necessarily scary. But combine them with a hiring frenzy (ok, maybe not a frenzy, but a big uptick nonetheless) that will likely lead to an increase in the cost of labor, and capital markets that are still a bit locked up in terms of lending for construction projects, and that's kind of a crappy cocktail. Increasing labor and commodity prices typically signal an improving economy, but if developers cannot get money to pay for them, then what's the point? Plus, the economy is still too fragile for large price increases to be absorbed by buyers not overly willing to pay a premium.

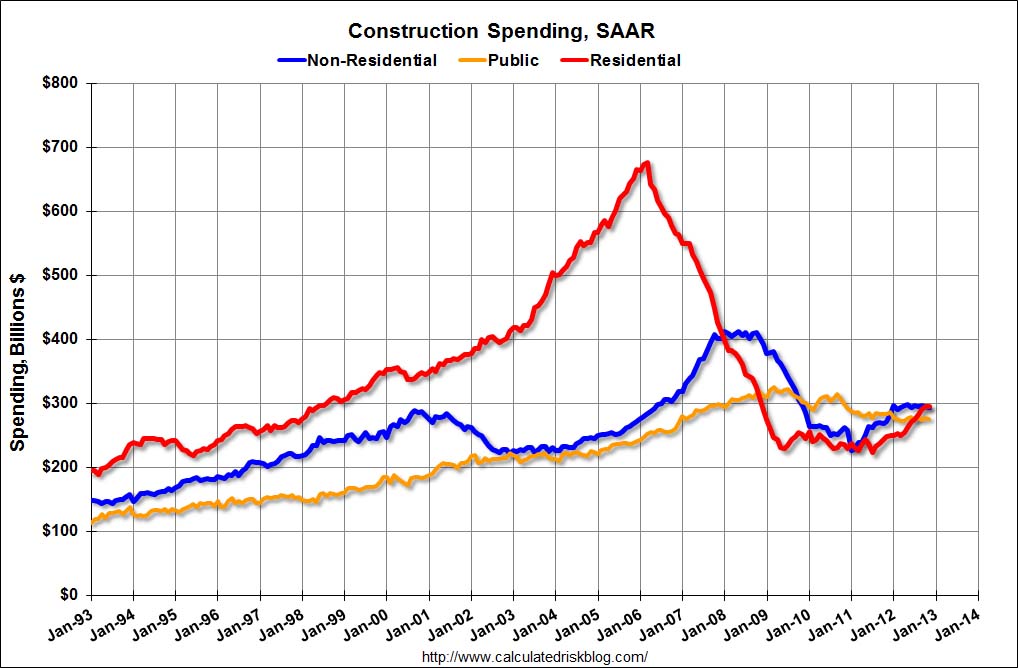

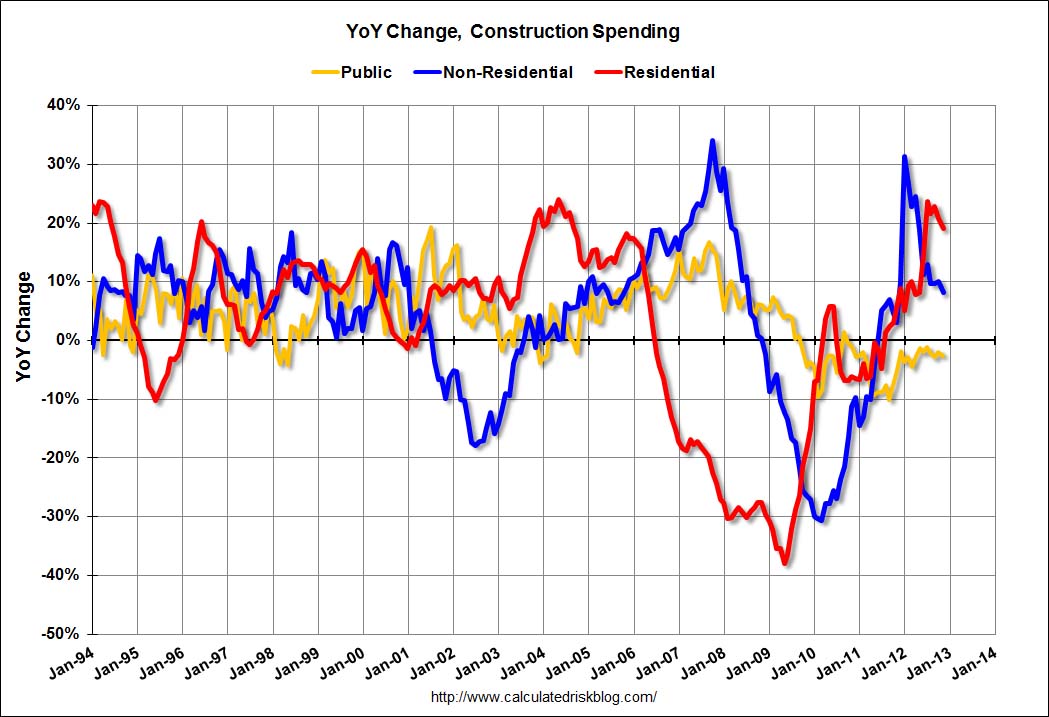

One last thing, and it's subtle. Caterpillar Inc. reported less than stellar earnings today. CAT is considered a bellwether stock for the overall economy, but the construction industry in particular. A big portion of the blame for their most recent decline in profits was due to problems in the mining industry (CAT supplies a lot of machinery to mining companies). But buried in this Wall Street Journal article is a sentence that caught my attention: "First quarter sales of construction equipment dropped 17% to $4.2 billion" It doesn't say where the decline in construction sales occurred (if it were limited to overseas, it may not affect the U.S. Or maybe it would.), but still, that's not particularly good news even without specifics. The bottom line: no need to panic yet (or at all), but keep your ears to the street and be cautious about the near-term health of the construction sector. There was more good news regarding the construction industry last week. According to the U.S. Census Bureau announced last week that construction spending for the month of February grew 1.2% from the previous month and 7.9 percent above February 2012. See the press release here. The improvement of construction spending month-over-month and year-over-year can be seen below (as provided by Bill McBride at www.calculatedriskblog.com):

A lot of the growth is due to the residential sector, but non-residential construction is up 6% year-over-year. This news is good for larger general contractors (like the ones I deal with and that my students go to work for). However, public construction spending (for things such as roads, schools, etc.) is down 1.5% year-over-year. So, it's a bit of a mixed bag, but overall, it's good news. And the housing sector tends to be a leading indicator for larger commercial and civil structure construction, so there may be better news on the horizon.

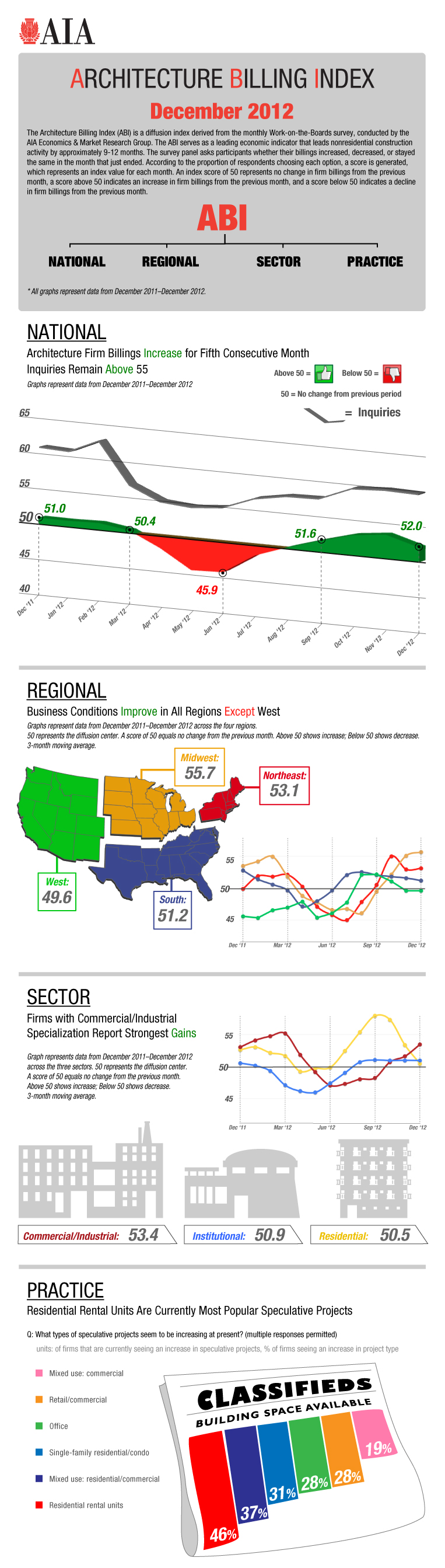

In other news... There was an article on the proposed new Apple campus in Cupertino, CA in Bloomberg Businessweek on April 4. According to the article, the 4-story, 2.8 million square-foot headquarters building's proposed cost has ballooned to ~$5 billion dollars (~$1,800/SF). There is an effort underway to value engineer $1 billion from the cost. Some people are piling on and questioning the wisdom of 1) constructing a building that is a giant donut (this type of space arrangement can actually isolate employees, which is is counter to the Silicon Valley ethos of creating spaces that increase the probability of chance meetings and collaboration, and 2) building an elaborate (ostentatious?) self-celebratory structure. I'm not going to weigh in on this because my attitude is that if you don't like how Apple spends it's money, you're free to sell your stock. Apple is sitting on a 12-figure cash stockpile, and they have to spend it somehow (with real estate having certain beneficial tax advantages). If you don't own stock in Apple (and presumably don't live in the shadow of the proposed structure), why do you care? But what I will mention is that there will almost certainly be a halo effect in that multiple additional peripheral structures will be constructed (hotels, banks, law firms, accounting firms, etc.). Also, as a net zero energy building pushing the edges of design and construction, the AEC industry will certainly learn something from this project (good, bad or otherwise). So net-net, I think this will be good for the construction industry. In the past two days, two leading economic indicators have showing continued improvement of the health of the construction industry (on top of the 48,000 new construction jobs reported earlier this month). First is the American Institute of Architects (AIA) Architectural Billings Index (ABI). The ABI has been steadily improving since the market bottomed out in early 2009. February's ABI came in at 54.9, increasing from 54.2 in January (50 is the baseline; greater than 50 means that architectural billings are increasing). The multi-family residential market was the healthiest and posted a strong gain over last month. The Northeast was the biggest winner in terms of geographical regions. All sectors and regions improved: Sectors:

Regions:

The New Project Inquiry Index (I'm not sure what that is, but it's name strongly suggests new projects) is at 64.8, it's highest level since January 2007. You can read the entire press release here and I'll post the cool graphic AIA typically produces when they post it. Second, it was reported today by the Wall Street Journal that plywood prices are skyrocketing (read article here). In the past year, prices have increased 45% and suppliers are having trouble keeping up with the increased demand. Increasing demand for plywood = more jobs using plywood = more construction activities. This is more good news for CM students. I have included the chart below that is maintained by Bill McBride at the Calculated Risk blog. Is shows the price of lumber per 1,000 board-feet, in case you're interested:

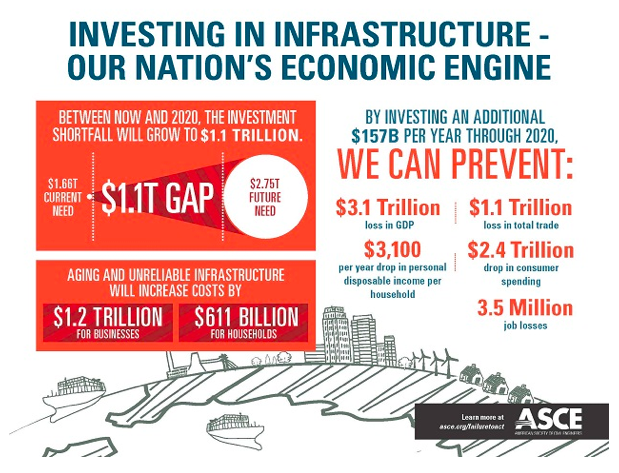

To answer the question posed in the title of this entry, we are apparently not investing in infrastructure, at least not in the ways we have in the past. Consider this graphic created by the American Society of Civil Engineers (ASCE):

Now, I typically take these graphics from ASCE with a grain of salt. I mean, ASCE, as an organization that supports civil engineers (a group that has a huge stake in infrastructure spending), is at least partially biased towards demanding more infrastructure spending. But the graphic below shows that they're not totally crying wolf:

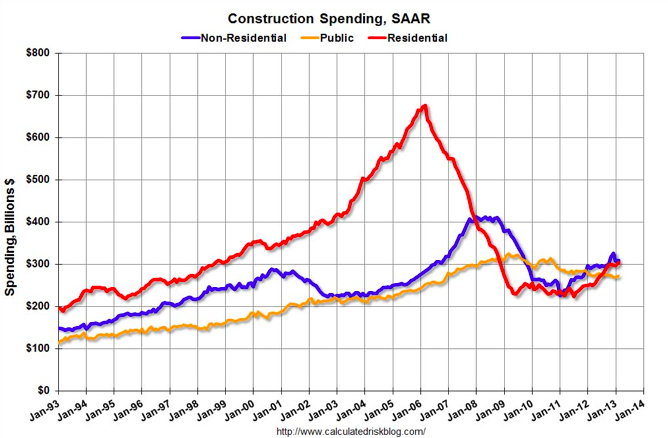

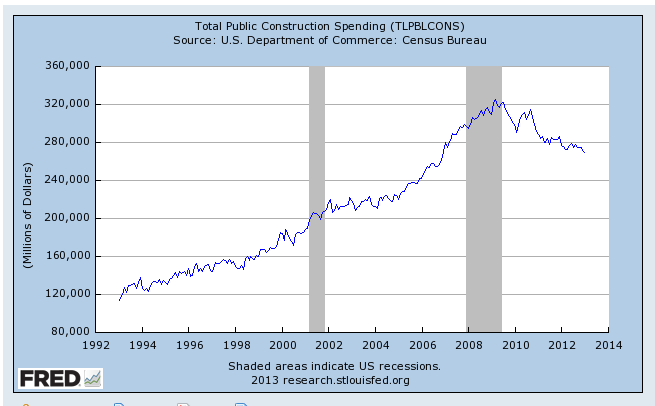

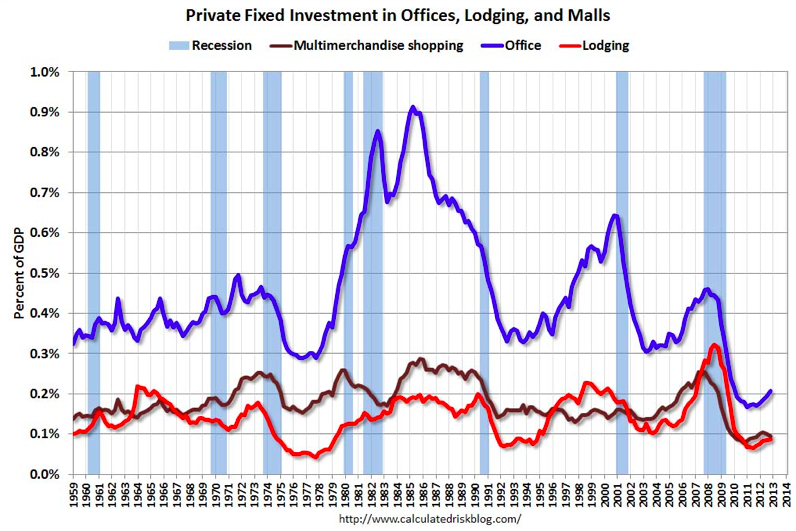

Since peaking in 2009, public spending in infrastructure has declined, save a short-lived uptick that started in late 2009 due to the American Recovery and Reinvestment Act. I'm interested in this phenomenon because at a recent technical job fair at Sac State, the large general contractors that are involved in infrastructure construction where among those with the most open positions. This form of hiring (soon-to-be recent college graduates) leads me to believe that perhaps construction spending in infrastructure is likely to start picking up (or contractors expect it to). I hope this is the case, because if ASCE is not calling for a falling sky, we could be in deepening trouble if we don't improve our crumbling infrastructure. If funding is dramatically cut, as is a likely scenario if the sequestration comes to fruition, it will only get worse. So public investments in infrastructure have decreased since the recession. There is very little private investment in infrastructure (in comparison to public investment). So where is private investment in buildings going? Let's go to some graphs created by Bill McBride of the Calculated Risk blog:

Capital investments in multimerchandise shopping centers (malls), office buildings, and lodging buildings have also declined since the recession. But there has been some positive growth in the past year or so in office and lodging building construction (malls have declined of recently after a slight recovery from 2011-2012; I have discussed the slowing growth in mall and big box retail construction elsewhere in this blog). The bigger story recently has been housing.

After also falling off a recessionary cliff, housing has increased markedly over the past year or so, particularly in single family housing (multi-family less so, but still moving positively in the last year). That's where the money seems to be going. With little inventory and large amounts of institutional money moving into single family housing, interest in that market should continue to be strong (emphasis on the *should*). A recent down tick in residential construction needs further data to see if it's an actual trend, but it seems on the macro scale that that's where construction investments are positive.

The bottom line: infrastructure spending is declining in the big picture (local areas may be bucking the trend, and hence the hiring of college graduates), but private building construction is increasing, particularly in housing. Wow, it's been a few weeks since I last posted, so there's a lot to get caught up on. Some of this news is a bit stale, so I'll keep it brief.

First, the sort of bad news: After going on a tear over 2012, the National Association of Homebuilders Housing Market Index (HMI) declined in February from 47 to 46. Any HMI less than 50 indicated that homebuilders see sales conditions for houses as poor (conversely, an HMI greater than 50 means the sales climate is good in the eyes of homebuilders). As I have said in the past, I'm not entirely interested in homebuilding as a sector of the construction industry, but it is a leading indicator for other types of construction (commercial, industrial, infrastructure, etc.). While a decrease is not good, it needs to be put in perspective: the HMI and number of housing starts increased crazily in 2012 (HMI in particular). It's not uncommon for markets to take a break. Let's wait to see if an actual downward trend emerges before hitting the panic button. More recently, it was reported that the price of lumber dipped slightly recently (it's around $400 per 1,000 board feet). Again, it has been going up over 2012 and this may just be a reaction to the small decline in HMI. A few months of data is still needed to see if this trend has staying power or if prices will start rising again. You can see how the price of lumber has changed over time here. The decline in prices may actually prompt corporations to start investing, and a recent headlines seem to indicate that's the case. Corporate capital spending plans have exceeded that predicted by Wall Street and have held up lately. The corporate spending on capital expenditures, or capex, includes offices, plants and machinery. This is the sector of the construction economy I am interested in because it's the one that hires the contractors most of the students that graduate with a Construction Management degree from Sac State will work for. Capex spending for 2013 is predicted to be the highest it's been in over the past four years. That's good news if it holds up, which leads me to... Any recovery, new or continued, is a function of sidestepping any issues tied to the sequestration. Hopefully our government will find some sort of palatable compromise so that we don't shoot our recovery in the foot. According to the Census Bureau, U.S. construction spending rose 0.9% (December, seasonally-adjusted rate), up from an increase of 0.1% last month (last month being November--there's a one-month lag on the data). The expected increase this month was 0.6%. Last month, -0.3% was the expected decrease. In other words, this month and last month handily beat expectations.

This increase in the growth rate means that the industry is on track for an annualized rate of $885 billion in construction spending. Most of the gains are in the single-family housing sector (residential housing construction grew 22.3% last year). But improvements in the residential market are usually correlated with improvements in the industry overall. I'm not sure how I missed the November ABI data, but since it's a new year, let's start fresh. And luckily, it's good news. The AIA's Architecture Billing Index (ABI), a leading indicator of construction, is up again, and 2012 finished at its highest since 2007. Booyah! The full press release can be found here.  The only real bad news, at least for us in the west, is that the measure is still slightly below 50 for that region (less than 50 corresponds to a decrease in billings, greater than 50 is an increase in billings). The west has shown some weakness over the past few months, but it's way lows of May 2012. Every sector is above 50, which is also good. All in all, a pretty good report, particularly since the economic recovery is still a bit fragile.

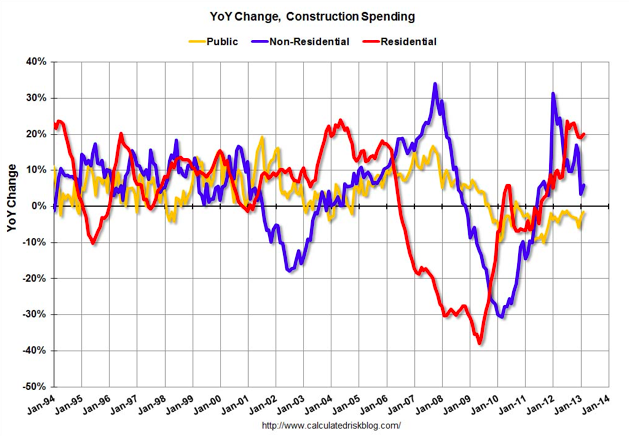

While the stock markets are going bananas over the avoidance of the fiscal cliff, some bad news has come out regarding the construction market. Per Ruth Mantell at the WSJ Market Watch: Outlays for U.S. construction projects declined in November, missing Wall Street's estimates, the U.S. Commerce Department reported Wednesday. Construction spending fell 0.3% in November, while analysts had expected a gain of 0.8%. Spending for October was downwardly revised to a gain of 0.7%, compared with a prior estimate of a 1.4% increase. In November, spending on private construction declined 0.2% while spending on public projects fell 0.4%. Spending on private homebuilding rose 0.4%. Home building is still going strong, but spending on projects municipal and commercial buildings is down. Even worse, analysts were expecting an uptick in building. Yikes! Let's hope this is an anomaly. [UPDTADED January 8, 2013] Here are two graphs from Bill McBride at the Calculated Risk blog that graphically represent how construction spending is trending:   So yes, this recent news is not great, particularly since the current recovery is still in a fragile state, but that can be expected from a weak recovery--there will be fits fits and starts. And this is one data point; a definitive trend cannot be determined yet. Next month's report will be very interesting. The good news is that we're in a much better place than we were in 2008-2010.

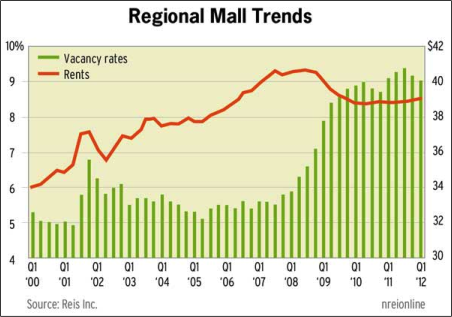

"I don't think we're overbuilt, I think we're under-demolished" -- Daniel Hurwitz, CEO of DDR, a commercial property owner and manager, talking about malls. I came across a blog post from Jeff Jordan, a Partner with venture capital firm Andreessen Horowitz. The gist of the post is in its title: "Why Malls Are Getting Mauled." Why would a venture capitalist be interested in malls? Because they fund online retailers (Jeff sits on the board of Fab.com and was previously a senior executive with eBay). Online retailers are the antithesis of malls. So even though Jeff is clearly rooting for online retailers in the online retailers vs. malls battle (if that can be billed as an actual battle), he presents some very compelling data. The data is interesting enough that Jeff expanded on his blog post in an article for The Atlantic Cites, which can be read here. There are three self-explanatory figures from the article that are worth showing here:    To summarize the above three figures, malls are hurting. Rents are flat and vacancies are increasing. And it's not like it's going to get better soon, seeing as many of the retailers that inhabit malls are hurting. The growth prospects don't look good. Hence the opening quote from Daniel Hurwitz. Unless the weak malls and retailers are culled from the herd, traditional brick-and-mortor retail properties will suffer. If you are a contractor that specializes in mall construction or sees a healthy percentage of your billings come from mall or brick-and-mortor retailers, this is troubling news. The pace of construction in that market is likely to decrease further, that is unless growing retail trends in the United State reverse course. If you are a contractor that has pursued work from retailers like Mervyn's, Circuit City or Borders, you already know this.

On the flip side, online retailers continue to grab market share from brick-and-mortor retailers. So while the market is closing the door on physical retail space construction, it's opening one for all things associated with online commerce. (*Note: I'm not predicting the death of malls and other physical retail stores. They will survive. There will just be fewer of them as time goes on if current trends hold. With more sales going online and lower rents from physical stores, the economics will call for fewer physical retail stores, and hence, less investment in them. But it won't go to zero anytime soon. Plus, with vacancies going up, and spaces changing hands, there may be increasing opportunities for tenant improvements. I just wanted to make that clear) So what does working in online commerce look like for commercial builders? Well, instead of clients like Sears, Macy's or Home Depot, your clients will be Google, Amazon, Facebook, Apple, etc. Instead of expansive retail spaces split up for individual stores and large tilt-up buildings for big box retailers, projects will be office buildings filled with cubicles, high-tech warehouses with miles of automated conveyor belts for fulfilling orders, and server farms that hold gobs of data. Google has an estimated 1 million servers split over 40 locations, and they're building more. There will be much fewer marble entrances, water fountains, glass curtain walls and other fancy architectural finishes and much more electrical and HVAC components (server farms, for example, suck electricity and require a lot of cooling). I will be coming back to this topic in the future because it's a deep vein of conversation. Some topics I hope to cover soon include:

But for now, let's just acknowledge that the competitive landscape of retailing is shifting, so general building contractors and their trade partners must be prepared to shift with it. |

Archives

January 2024

Categories |

RSS Feed

RSS Feed